OPTIONS: All Call Spread Buying In Rates

Sep-03 16:52

Wednesday's Europe rates/bond options flow included:

- ERU5 97.9375/98.00cs, bought for 2 in 20k

- SFIZ5 96.20/96.25cs, bought for 1.75 in 2k

- SFIM6 96.70/96.85cs, bought for 2.75 in 6k

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: Corporate Bond Update: $2B FISERV 2Pt, $1.5B Quanta 3Pt Launched

Aug-04 16:48

- Date $MM Issuer (Priced *, Launch #)

- 08/04 $2B #FISERV $1B +5Y +87, $1B 10Y +107

- 08/04 $1.5B #Quanta Services $500M Each: 3Y +65, +5Y +80, 10Y +93

- 08/04 $1.25B Level 3 Financing 8.5NC3

- 08/04 $1B #Altria $500M 5Y +85, $500M 10Y +112

- 08/04 $600M #CenterPoint Houston 10Y +80

- 08/04 $Benchmark KKR & Co. 10Y +115a

- 08/04 $Benchmark Chub Holdings 10Y +70

- 08/04 $Benchmark Public Service of Colorado 10Y +120a, 2055 Tap

- 08/04 $Benchmark Dominion Energy 30.5NC5.25 6%, 30.5NC10.25 6.2%

- 08/04 $Benchmark Barclays 4.25NC3.25 +83, 4.25NC3.25 SOFR, 21NC10 +110

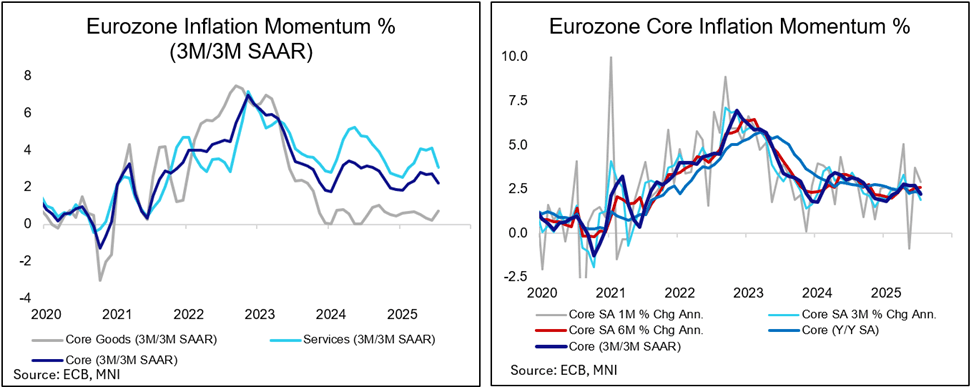

EUROPEAN INFLATION: MNI Eurozone Inflation Insight – July 2025

Aug-04 16:25

We've just published our review of the July Eurozone flash inflation round - DOWNLOAD FULL REPORT HERE

Services Inflation Moderates Further

- Eurozone July flash headline HICP printed slightly above expectations on Friday, at an unchanged 2.0% Y/Y (2.02% after 1.99%), while the median analyst was looking for a marginally lower 1.9% print.

- Underlying the headline ‘beat’ was a set of moving parts: Services inflation, at 3.13%, decelerated to a greater extent than expected, to its lowest Y/Y reading since March 2022 on a rounded basis, but non-energy industrial goods (‘core goods’) came in notably above consensus, at 0.75%, with changing or less significant seasonal summer clothing sales likely being at work. This made for a little changed and in line ‘core’ reading of 2.29% Y/Y in July.

- Services 3M/3M momentum meanwhile eased to 3.1% annualised after three months at circa 4.0% according to separate ECB seasonally adjusted data.

- Near-term ECB market-implied expectations currently stand at a mere 15% implied odds for another cut by the September meeting. A repricing thereof would likely have to be motivated through a material deterioration in sentiment amid the 15% US-EU trade deal or a significant undershoot in the August inflation round – especially in categories considered as indicative for persistent inflation pressures.

- Further out, markets continue to expect almost one more cut for the ECB current cycle which would mean a 1.75% terminal for the deposit rate, with 22bps of easing priced through March 2026.

LOOK AHEAD: Tuesday Data Calendar: Import/Export, PMIs, ISM Services, 3Y Sale

Aug-04 16:24

- US Data/Speaker Calendar (prior, estimate)

- 08/05 0830 Trade Balance (-$71.5B, -$61.1B)

- 08/05 0830 Exports MoM (-4.0%, --), Imports MoM (-0.10%, --)

- 08/05 0945 S&P Global US Services PMI (55.2, 55.2)

- 08/05 0945 S&P Global US Composite PMI (54.6, 54.6)

- 08/05 1000 ISM Services Index (50.8, 51.5)

- 08/05 1000 ISM Services Prices Paid (67.5, 67.0)

- 08/05 1000 ISM Services New Orders (51.3, --)

- 08/05 1000 ISM Services Employment (47.2, --)

- 08/05 1130 US Tsy $85B 6W & $50B 52W bill auctions

- 08/05 1300 US Tsy $58B 3Y Note auction (91282CNU1)

- Source: Bloomberg Finance L.P. / MNI

Trending Top

Jan-30 21:43

Jan-30 21:11