BONDS: EGBs-GILTS CASH CLOSE: Pressure On Long End Abates

Sep-03 16:41

Yields reversed an early rise to finish lower Wednesday, with strong bull flattening evident across EGBs and Gilts.

- Gilt futures pierced Tuesday's lows in early trade, with ongoing fiscal concerns continuing to weigh on the space, but eventualy bounced; meanwhile 10Y Bund yields weakened but held the 2.80% level.

- Having found an early footing, bonds rallied through much of the remainder of the session.

- Weak US job openings data added a final up-leg to global core FI in mid-afternoon, with yields closing near their session lows. Long-end Gilts also benefited from DMO cancelling a 30Y auction in the FQ3 quarter.

- In BOE Treasury Select Committee testimony, some highlights included Lombardelli sounding more hawkish that MNI's Markets Team had assumed, while BoE's Bailey noted that the bank's decision on QT in the next few weeks "is an open decision".

- European data wasn't a market-mover, with composite PMIs in the Eurozone and UK respectively revised slightly lower/higher in the final readings.

- The German and UK curves bull flattened, with Gilts outperforming; periphery/semi-core EGB spreads tightened, with BTPs outperforming.

- Thursday's schedule includes Eurozone retail sales and an appearance by ECB's Cipollone, while Swiss and Swedish inflation will garner some attention.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.8bps at 1.966%, 5-Yr is down 3.3bps at 2.28%, 10-Yr is down 4.6bps at 2.74%, and 30-Yr is down 5bps at 3.356%.

- UK: The 2-Yr yield is down 2.2bps at 3.96%, 5-Yr is down 4.1bps at 4.13%, 10-Yr is down 5.2bps at 4.748%, and 30-Yr is down 9bps at 5.603%.

- Italian BTP spread down 1.7bps at 87.3bps / French OAT down 0.2bps at 79.9bps

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

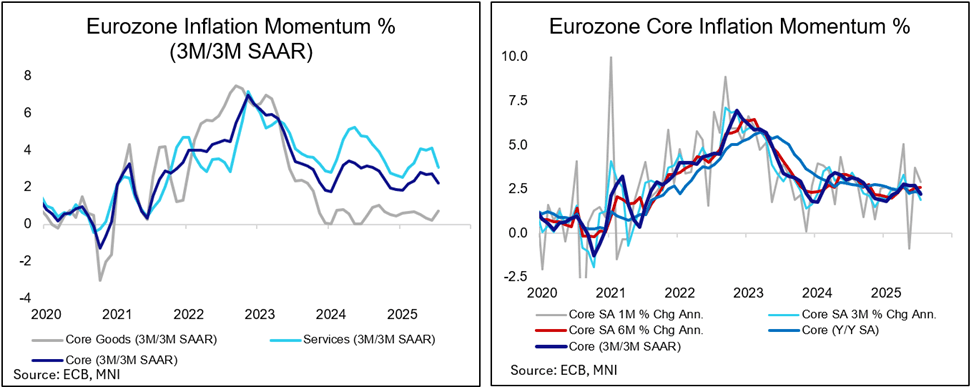

EUROPEAN INFLATION: MNI Eurozone Inflation Insight – July 2025

Aug-04 16:25

We've just published our review of the July Eurozone flash inflation round - DOWNLOAD FULL REPORT HERE

Services Inflation Moderates Further

- Eurozone July flash headline HICP printed slightly above expectations on Friday, at an unchanged 2.0% Y/Y (2.02% after 1.99%), while the median analyst was looking for a marginally lower 1.9% print.

- Underlying the headline ‘beat’ was a set of moving parts: Services inflation, at 3.13%, decelerated to a greater extent than expected, to its lowest Y/Y reading since March 2022 on a rounded basis, but non-energy industrial goods (‘core goods’) came in notably above consensus, at 0.75%, with changing or less significant seasonal summer clothing sales likely being at work. This made for a little changed and in line ‘core’ reading of 2.29% Y/Y in July.

- Services 3M/3M momentum meanwhile eased to 3.1% annualised after three months at circa 4.0% according to separate ECB seasonally adjusted data.

- Near-term ECB market-implied expectations currently stand at a mere 15% implied odds for another cut by the September meeting. A repricing thereof would likely have to be motivated through a material deterioration in sentiment amid the 15% US-EU trade deal or a significant undershoot in the August inflation round – especially in categories considered as indicative for persistent inflation pressures.

- Further out, markets continue to expect almost one more cut for the ECB current cycle which would mean a 1.75% terminal for the deposit rate, with 22bps of easing priced through March 2026.

LOOK AHEAD: Tuesday Data Calendar: Import/Export, PMIs, ISM Services, 3Y Sale

Aug-04 16:24

- US Data/Speaker Calendar (prior, estimate)

- 08/05 0830 Trade Balance (-$71.5B, -$61.1B)

- 08/05 0830 Exports MoM (-4.0%, --), Imports MoM (-0.10%, --)

- 08/05 0945 S&P Global US Services PMI (55.2, 55.2)

- 08/05 0945 S&P Global US Composite PMI (54.6, 54.6)

- 08/05 1000 ISM Services Index (50.8, 51.5)

- 08/05 1000 ISM Services Prices Paid (67.5, 67.0)

- 08/05 1000 ISM Services New Orders (51.3, --)

- 08/05 1000 ISM Services Employment (47.2, --)

- 08/05 1130 US Tsy $85B 6W & $50B 52W bill auctions

- 08/05 1300 US Tsy $58B 3Y Note auction (91282CNU1)

- Source: Bloomberg Finance L.P. / MNI

SECURITY: Netherlands To Be First Contributor To New Ukraine Financing Mechanism

Aug-04 16:23

The Netherlands will be the first country to contribute (500 million euros) to NATO’s new "Priority Ukraine Requirements List" (PURL) financing mechanism for Ukraine, per Reuters.

- Comes after President Donald Trump said last month that the US and NATO would develop a mechanism for the United States to maintain military support for Ukraine via NATO partners in Europe. The financing initiative is part of a two-pronged approach to push Russia to the negotiating table with Ukraine.

- Reuters reported last week, “Ukraine would prioritize the weapons it needs in tranches of roughly $500 million, and NATO allies... would then negotiate among themselves who would donate or pay for items on the list. Through this approach, NATO allies hope to provide $10 billion in arms for Ukraine... It was unclear over what timeframe they hope to supply the arms.”

- Trump negotiator Steve Witkoff is expected to meet Russian officials in Moscow on August 6, just days before the Friday deadline for Russia to agree a ceasefire with Ukraine.

- If Russia does not commit to a ceasefire, Trump has promised sanctions and secondary tariffs, but it is unclear if a final decision has been taken on the scope of the measures. Trump also downplayed the effectiveness of sanctions, telling reporters Russia seems to be “pretty good at avoiding sanctions."

- Senator Jim Rische (R-ID), the chair of the Senate Foreign Relations Committee, said: “When and if secondary sanctions hit, it’s going to be shock and awe,” adding that “things are going to change dramatically” as a result.

Trending Top

Jan-30 21:43

Jan-30 21:11