MNI ASIA MARKETS ANALYSIS: Stocks Shrug Off US-China Tensions

MNI (NEW YORK) -

HIGHLIGHTS:

- Equities recover from early drop, rallying into the monthly close despite US-China trade tensions

- Canadian dollar outperforms peers after firm GDP data points to no BOC cut next week

- Next week's key events include the ECB decision and US nonfarm payrolls

US TSYS: Twist Steepening Into Monthly Close

Treasuries twist steepened into the monthly close Friday.

- After a fairly flat overnight session, yields fell across the curve in early New York trade after President Trump posted on social media that China was in violation of its agreement set with the US, triggering a risk-off move.

- Yields would bounce back after PCE data came largely in line though April's trade deficit was much smaller than expected, later leading the Atlanta Fed to up its Q2 GDP growth nowcast to close to 4%.

- The Treasury bid was re-kindled in late morning, following weak MNI Chicago PMI data and a downward revision in UMichigan consumer inflation expectations, and as equities headed to session lows.

- But from there into the close, stocks and bonds decoupled (possibly the result of month-end dynamics), with the former rising to session highs while Treasuries merely consolidated earlier gains.

- Latest levels: the 2-Yr yield is down 3.5bps at 3.9037%, 5-Yr is down 2.8bps at 3.9686%, 10-Yr is down 1.2bps at 4.4063%, and 30-Yr is up 0.7bps at 4.9233%. The Sep 25 T-Note future is up 4/32 at 110-26, having traded in a range of 110-18 to 110-29.5.

- Monday's highlights include the ISM Manufacturing survey and an appearance by Fed Chair Powell, with the June employment report looming at the end of next week.

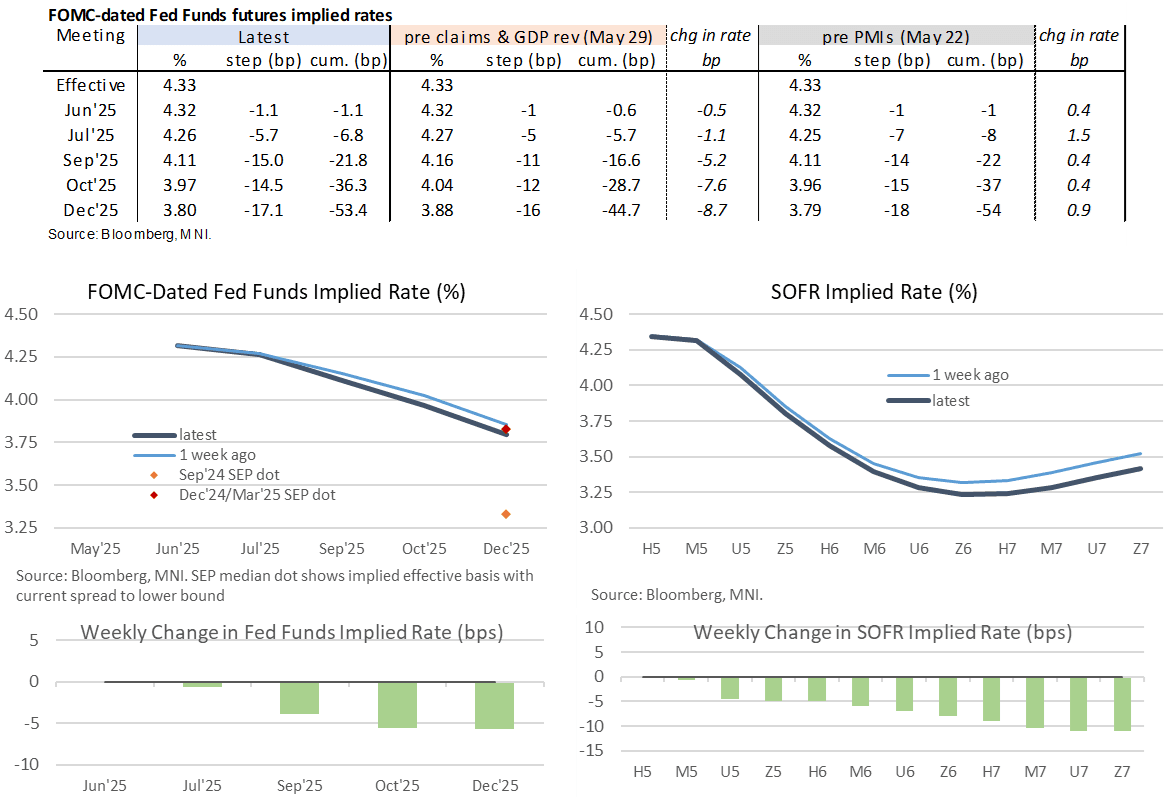

STIR: Dovish Weekly Shift On Renewed Souring In Risk Sentiment And Dovish Data

- After a shorter effective trading week with Memorial Day on Monday, Fed Funds implied rates for 2025 meetings have followed risk sentiment related to latest US tariff deliberations along with an added impetus from some dovish data.

- It’s seen a sizeable pullback from what had been the most hawkish levels since February early on Thursday, with 2025 cuts currently at 54bp vs 42bp at one point after a trade court ruled against IEEPA-related tariffs before an appeals court questioned the decision.

- The dovish adjustment late this week still doesn’t quite fully price a next cut with the September FOMC, but it’s closer now at 23bp having been 16.5bp prior to Thursday’s jobless claims data.

- Terminal rate expectations have been hit more heavily, with SOFR implied yields seen at 3.235% in the Dec’26 contract, at what would be the lowest close since May 7 as it nears 110bp of cuts from the current effective Fed Funds rate.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

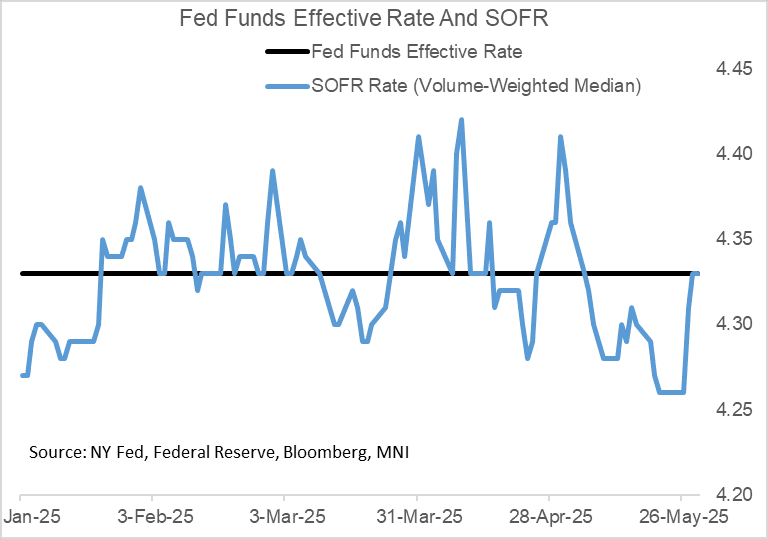

US TSYS/OVERNIGHT REPO: SOFR Holds Ahead Of Month-End/Settlement Pressures

Secured rates were unchanged Thursday after successive rises, with SOFR remaining at 4.33%.

- There were probably countervailing forces at play: to the upside by looming month-end pressures, and to the downside by $29B net Treasury paydowns (bills).

- Friday and Monday will see significantly more upside pressure on rates though: month-end dynamics and $46B in Treasury net new cash raised via FRN / TIPS auction settlements (Friday), and a further $94B in nominal coupon settlements Monday.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.33%, no change, $2652B

* Broad General Collateral Rate (BGCR): 4.32%, no change, $1059B

* Tri-Party General Collateral Rate (TGCR): 4.32%, no change, $1021B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $114B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $302B

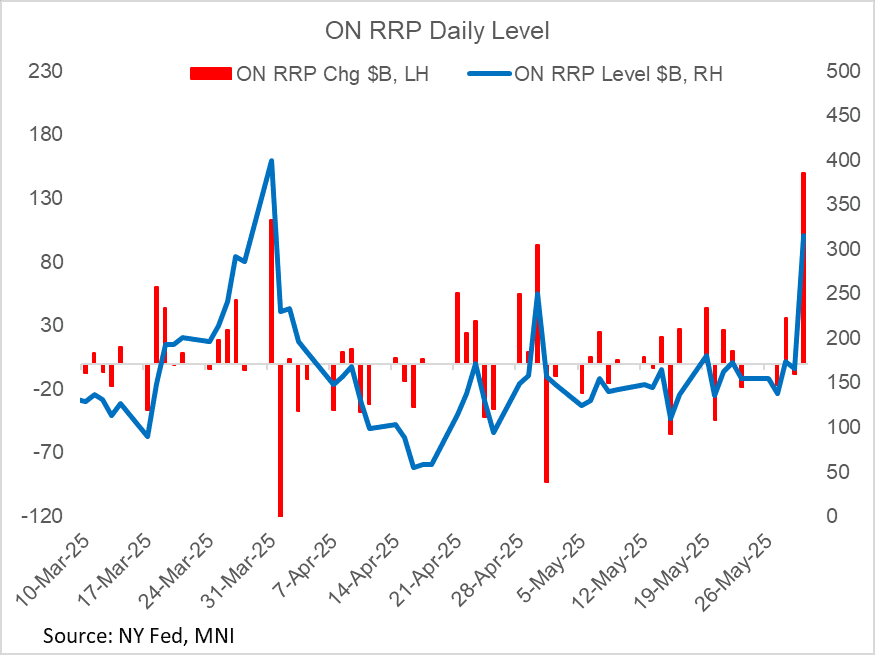

US TSYS/OVERNIGHT REPO: Overnight Reverse Repo Takeup Soars At Month-End

Takeup of the Fed's overnight reverse repo facility soared by $150B Friday, the biggest jump of the year (the last highest was Dec 31, 2024 amid year-/quarter-/month-end).

- The overall takeup ($315.7B) was the highest since quarter-end Q1 (March 31, $399.2B).

- This increase appears to be higher than anticipated (one estimate we saw was Wrightson ICAP's $260B), and indeed the takeup appears unusually large for a non-quarter end.

- Regardless, inflows are expected to reverse sharply lower Monday as usual following month-end.

US 10YR FUTURE TECHS: (U5) Bear Threat Remains Present

- RES 4: 112-04+ High May 2

- RES 3: 111-25 High May 7

- RES 2: 111-05+ High May 9

- RES 1: 110-23/27+ High May 16 and a key resistance / High May 30

- PRICE: 110-21 @ 16:01 BST May 30

- SUP 1: 109-26/12+ Low May 29 / 22 and the bear trigger

- SUP 2: 109-09+ Low Apr 11 and key support

- SUP 3: 109-00 Round number support

- SUP 4: 108-25+ 0.764 proj of the Apr 7 - 11 - May 1 price swing

A bear cycle in Treasury futures remains in play for now, and recent short-term gains are considered corrective. However, the contract is testing resistance 110-23, the May 16 high. A clear break of this level would undermine a bearish theme and highlight a stronger reversal, exposing 111-05+, the May 9 high. A reversal lower would refocus attention on the key support and bear trigger at 109-12+.

BONDS: EGBs-GILTS CASH CLOSE: Ending The Week With Twist Flattening

European curves lightly twist flattened Friday, with long-end instruments continuing to rally.

- Core instruments opened the session relatively flat following Thursday's rally, and drifted higher through the European morning.

- Eurozone inflation data was an early focus, with Germany surprising slightly to the upside, but Spain softer-than-expected (Italy's was in line).

- A risk-off move in equities triggered by US President Trump's accusation that China has "totally violated" their trade agreement helped trigger a safe haven bid, while weaker-than-expected MNI Chicago PMI maintained EGB/Gilt strength.

- After a small retracement as markets eyed month-end, yields closed nearer to their session lows than their highs.

- The German and UK curves both twist flattened. For the week as a whole, curves also twist flattened, with Bunds outperforming Gilts. German 2Y +1.2bp/10Y -6.7bp; UK 2Y +4.0bp/10Y -3.4bp.

- Periphery / semi-core spreads were mixed, with Portugal outperforming.

- Ratings reviews scheduled for after the market close Friday include S&P on France.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.7bps at 1.776%, 5-Yr is down 0.4bps at 2.064%, 10-Yr is down 0.8bps at 2.5%, and 30-Yr is down 0.7bps at 2.98%.

- UK: The 2-Yr yield is up 2.8bps at 4.023%, 5-Yr is up 1.6bps at 4.144%, 10-Yr is down 0.1bps at 4.647%, and 30-Yr is down 2.4bps at 5.372%.

- Italian BTP spread down 0.1bps at 98bps / Portuguese down 2.3bps at 47.5bps

EUROPE OPTIONS: Varied Sonia Call Flies Feature Friday

Friday's Europe rates/bond options flow included:

- RXQ5 127/125/124 broken put fly, sold at 7.5 in 2k.

- ERU5 98.0625/97.9375ps 1x2, bought for 2 in 6.25k.

- SFIU5 96.10/96.20/96.50 broken c fly, bought for half in 7k.

- SFIU5 96.10/96.30/96.50 1x1.5x0.5 call fly, paper pays 3 for 8.5k

- SFIH6 95.70/95.40ps 1x2, sold at flat in 3.5k.

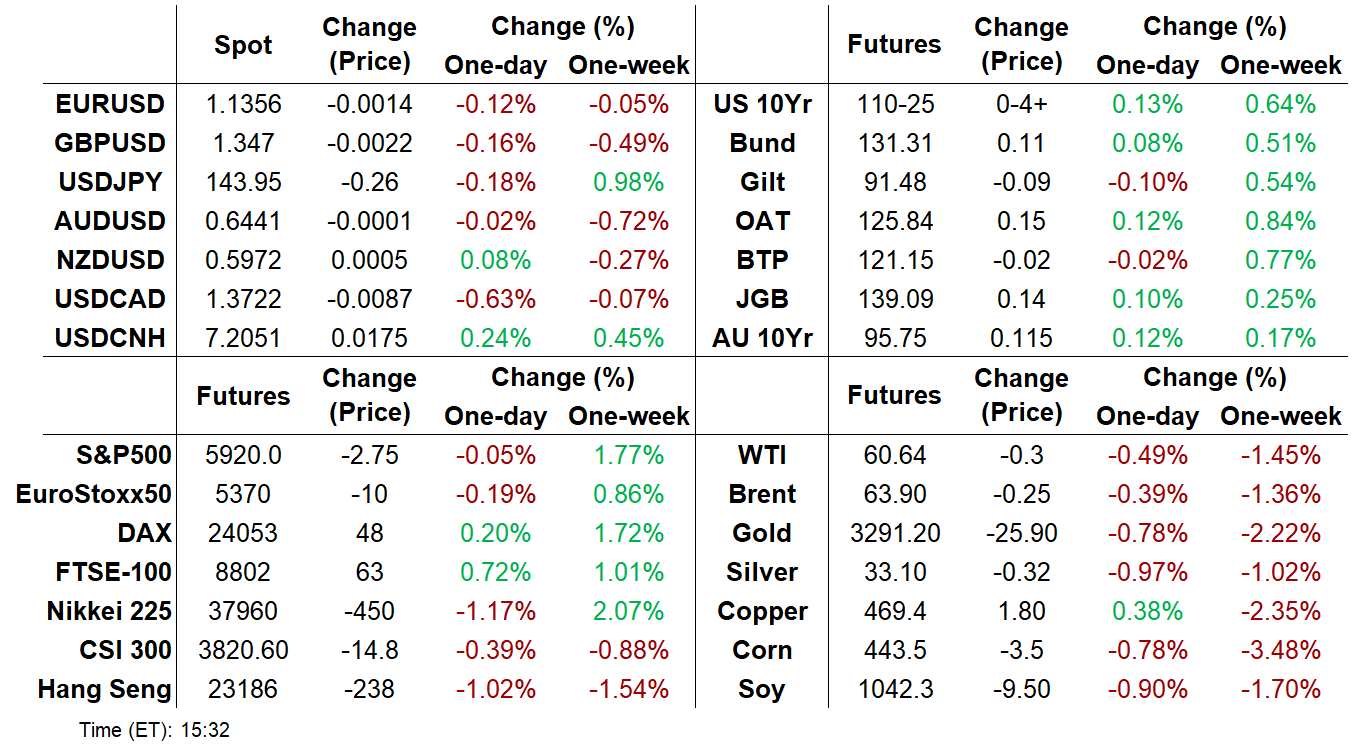

FOREX: Canadian Dollar Outperforms as BOC Easing Expectations Trimmed

- Some volatile two-way swings for equities had little effect on major currencies Friday, and the USD index looks set to close at unchanged levels on the session, modestly positive on the week. USDJPY remained its volatile self, posting a near 100 pip range across US trade, but broadly consolidates around the 144 handle as we approach the weekend.

- EURUSD has exhibited a stable tone, and the solid bounce from 1.12 on Thursday keeps bullish conditions firmly in play for the pair. On the upside, a break of 1.1419, the May 26 high, would be a bullish development and bolster the underlying trend.

- The most notable strength has been for the Canadian dollar, following a robust set of GDP data across the first quarter and an associated trimming of cut expectations for next week’s BOC. Market pricing now assigns just a ~20% chance of a cut, compared to ~28% prior to today's data.

- Price action backs up the underlying bear trend for USDCAD (-0.64%) - through which a sell-on-rallies theme clearly persists. Barring the corrective bounce earlier in the week, the sequence of lower lows and lower highs. Sights are on 1.3643 next, the Oct 9 2024 low. A phase of USD sales into the Friday month-end fix may have assisted this dynamic. Below here, attention will be on 1.3579, the 1.5 projection of the Feb 3 - 14 - Mar 4 price swing

- Swiss GDP and final eurozone PMIs kick off the economic calendar on Monday, before the focus turns to the US ISM Manufacturing PMI. Fed Chair Powell is also delivering opening remarks at a conference in Washington.

OPTIONS: Expiries for Jun02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1250($1.4bln), $1.1300-05(E1.9bln), $1.1345-50(E1.9bln)

- EUR/JPY: Y159.50(E500mln)

- AUD/USD: $0.6400(A$856mln), $0.6425-45(A$789mln)

EQUITIES: Stocks Shrug Off US-China Tensions, Led By Defensives

Equities are shrugging off a sources piece from the WSJ into the monthly close: "A trade truce between the U.S. and China is at risk of falling apart, as China's slow-walking on rare-earth exports fuels U.S. recriminations that China is reneging on the deal. Getting the pact together in Geneva earlier this month hinged on Beijing's concession on the critical minerals, according to people familiar with the matter."

- This adds some more color to this morning's White House contentions that China had failed to meet its commitments under the Geneva deal.

- Equities however appear to be largely ignoring today's US-China tensions, with S&P emini futures now up 0.1% on the session after being down as much as 1.1%, helped in part by the largest buying program of the day at 3:25pm (1372 names) and perhaps some month-end dynamics.

- Though at 5,917 last, e-minis have failed to test the May 20 high (and bull trigger) of 5,993.50.

- In cash, it's been mainly defensives outperforming, suggesting that perhaps the recovery is not particularly risk-on: S&P500 consumer staples +1.4% (Costco up 4.1%), utilities +0.9% and healthcare +0.5%, with energy (-0.8%), info tech (-0.6%) and consumer discretionary (-0.3%) pulling up the rear.

EQUITY TECHS: E-MINI S&P: (M5) Bulls Remain In The Driver’s Seat

- RES 4: 6124.00 High Feb 24

- RES 3: 6080.75 High Feb 26

- RES 2: 6057.00 High Mar 3

- RES 1: 6008.00 High May 29

- PRICE: 5904.75 @ 14:17 BST May 30

- SUP 1: 5815.85/5742.22 20- and 50-day EMA values

- SUP 2: 5596.00 Low May 7

- SUP 3: 5455.50 Low Apr 30

- SUP 4: 5355.25 Low Apr 24

A bullish trend condition in S&P E-Minis remains intact. Thursday’s initial gains delivered a print above 5993.50, the May 20 high and a bull trigger. The break highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. 6000.00 has been pierced, an extension would open 6057.00 next, the Mar 3 high. Key support lies at 5742.22, the 50-day EMA. A clear break of this average is required to highlight a reversal.

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 30/05/2025 | 2045/1645 | San Francisco Fed's Mary Daly | ||

| 30/05/2025 | 2330/1930 | Chicago Fed's Austan Goolsbee | ||

| 31/05/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/05/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 02/06/2025 | 2300/0900 | ** | S&P Global Manufacturing PMI (f) | |

| 01/06/2025 | 0000/2000 | Fed Governor Christopher Waller | ||

| 02/06/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 02/06/2025 | 0630/0830 | ** | Retail Sales | |

| 02/06/2025 | 0700/0900 | *** | GDP | |

| 02/06/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 02/06/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 02/06/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 02/06/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 02/06/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 02/06/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 02/06/2025 | 0830/0930 | ** | BOE M4 | |

| 02/06/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 02/06/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 02/06/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 02/06/2025 | 1400/1000 | * | Construction Spending | |

| 02/06/2025 | 1400/1000 | * | Construction Spending | |

| 02/06/2025 | 1400/1000 | Dallas Fed's Lorie Logan | ||

| 02/06/2025 | 1400/1500 | BOE's Mann fireside chat at Fed's IF 75th anniversary conference | ||

| 02/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 02/06/2025 | 1630/1830 | ECB Lagarde Video Message at Women In Finance Event | ||

| 02/06/2025 | 1645/1245 | Chicago Fed's Austan Goolsbee | ||

| 02/06/2025 | 1700/1300 | Fed Chair Jerome Powell | ||

| 02/06/2025 | 1700/1800 | BOE Greene Fireside Chat | ||

| 03/06/2025 | 0130/1130 | Business Indicators | ||

| 03/06/2025 | 0130/1130 | Balance of Payments: Current Account | ||

| 03/06/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI |