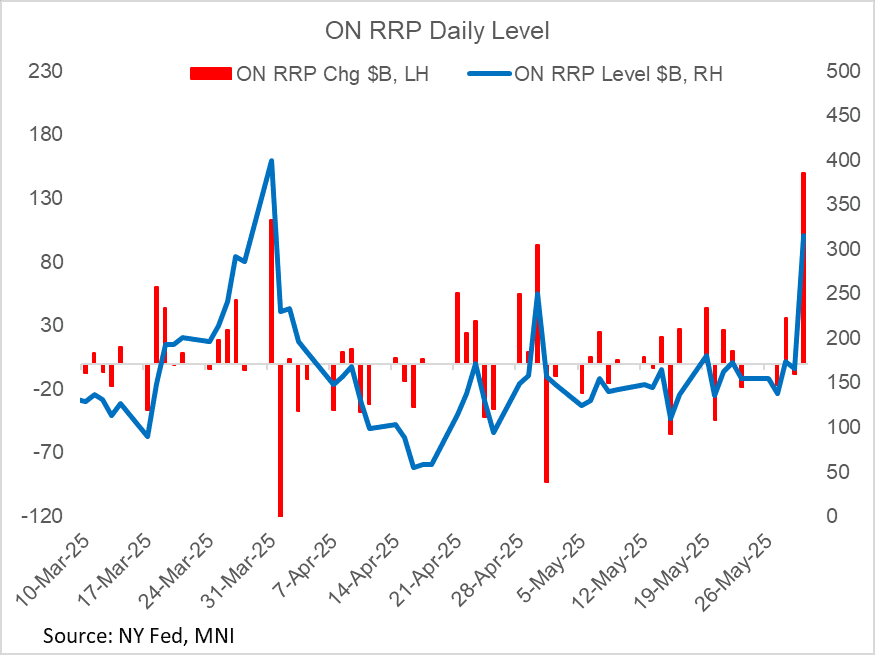

US TSYS/OVERNIGHT REPO: Overnight Reverse Repo Takeup Soars At Month-End

May-30 17:35

Takeup of the Fed's overnight reverse repo facility soared by $150B Friday, the biggest jump of the year (the last highest was Dec 31, 2024 amid year-/quarter-/month-end).

- The overall takeup ($315.7B) was the highest since quarter-end Q1 (March 31, $399.2B).

- This increase appears to be higher than anticipated (one estimate we saw was Wrightson ICAP's $260B), and indeed the takeup appears unusually large for a non-quarter end.

- Regardless, inflows are expected to reverse sharply lower Monday as usual following month-end.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: Corporate Bond Update: $3.25B BNP Paribas 3Pt Launched

Apr-30 17:32

- Date $MM Issuer (Priced *, Launch #)

- 04/30 $3.25B #BNP Paribas $1.6B 4NC3 +120, $400M 4NC3 SOFR+143, $1.25B 6NC5 +135

- 04/30 $2.5B Bahrain $750M 12Y 7.5%, $1.75B 8Y Sukuk 6.25%

- 04/30 $2B *IADB 5Y SOFR+44

- 04/30 $1.25B *Nordic Investment Bank 5Y SOFR+43

- 04/30 $1B *CoE Dev Bank 3Y SOFR+36

- 04/30 $850M *Uzbekneftgaz 5Y 8.75%

GBPUSD TECHS: Bullish Trend Structure

Apr-30 17:30

- RES 4: 1.3605 1.236 proj of the Feb 28 - Apr 3 - 7 price swing

- RES 3: 1.3550 High Feb 24 ‘22

- RES 2: 1.3510 1.236 proj of the Feb 28 - Apr 3 - 7 price swing

- RES 1: 1.3444 High Apr 28 / 29

- PRICE: 1.3337 @ 16:27 BST Apr 30

- SUP 1: 1.3280 Low Apr 28

- SUP 2: 1.3202 20-day EMA

- SUP 3: 1.3041/3002 Low Apr 14 / 50-day EMA

- SUP 4: 1.2807 Low Apr 10

The trend condition in GBPUSD remains bullish and Monday’s fresh cycle high reinforces current conditions. The move higher highlights a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Moving average studies are in a bull-mode position too, signalling a dominant uptrend. Sights are on 1.3510, a Fibonacci projection. Support to watch lies at 1.3202, the 20-day EMA.

BONDS: EGBs-GILTS CASH CLOSE: Bellies Outperform

Apr-30 17:19

European yields fell on a data-heavy Wednesday.

- After some initial overnight weakness, Bunds and Gilts largely looked through higher-than-expected Q1 Eurozone GDP and French and German state-level flash inflation.

- Core instruments would strengthen through the European morning session on weaker equities and oil prices which helped support global FI generally.

- Stronger-than-expected (or at least, less-weak-than-expected) US GDP and PCE inflation data saw core FI pull back sharply, but Bunds and Gilts would rally anew as equities tumbled on US growth fears.

- The German and UK curves leaned bull steeper on the day, with outperformance in the bellies. Periphery EGB spreads widened modestly, with GGBs underperforming.

- Following today's inflation releases, April Eurozone core HICP (Friday) is seen as having upside risks vs the 2.5% Y/Y estimate coming into the week.

- Thursday is a holiday (Labor Day) throughout much of Europe, though in the UK we get consumer credit / money supply / mortgage data, as well as final April Manufacturing PMI.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 5bps at 1.686%, 5-Yr is down 5.9bps at 1.985%, 10-Yr is down 5.3bps at 2.444%, and 30-Yr is down 4.5bps at 2.882%.

- UK: The 2-Yr yield is down 4bps at 3.803%, 5-Yr is down 4.1bps at 3.917%, 10-Yr is down 3.9bps at 4.441%, and 30-Yr is down 3.7bps at 5.207%.

- Italian BTP spread up 1bps at 112bps / Greek up 1.3bps at 85.5bps