MNI ASIA MARKETS ANALYSIS: SF Fed Daly Recalibrate Policy Soon

HIGHLIGHTS

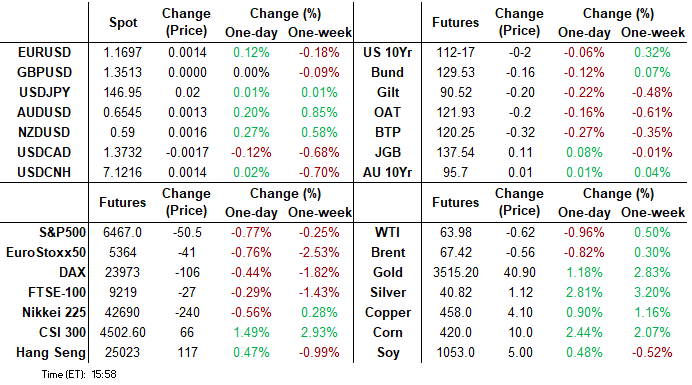

- Treasuries look to finish mostly weaker Friday, curves twisting back steeper (2s10s +3.564 at 60.589, 5s30s +4.097 at 122.418) with the short end outperforming much of the session.

- Late bounce in Tsys on SF Fed Daly comment on LinkedIn: that "it will soon be time to recalibrate policy".

- Steepening support may be a function of position squaring ahead the extended holiday weekend, month end, or even the Fed Gov Cook dismissal hearing that adjourned without a ruling.

- The USD index has edged lower on Friday, as the stagflationary picture painted by the U.S PCE & Chicago PMI data as well as ongoing uncertainty surrounding Fed independence weigh on the greenback.

- Next week’s calendar (Monday closed for Labor Day holiday) will undoubtedly be centered around the US employment report on Friday. Elsewhere, US ISM PMIs are also scheduled, as well as Australia GDP and Swiss CPI.

US TSYS

MNI US TSYS: Late Buying on Late SF Fed Daly Recalibration Comment

- Treasuries are still mostly weaker after the bell - but swinging off late lows following late comments on LinkedIn from SF Fed Daly, that tariff-tied inflation is likely a one-off, that inflation/labor market are in tension, and lastly that "it will soon be time to recalibrate policy"

- Tsy Dec'25 10Y futures currently trades -.5 at 112-18.5 vs. 112-20.5 morning high, initial technical resistance above at 112-28.5 (2.000 proj of the Jul 15 - 22 - 28 price swing).

- Curves mildly steeper: 2s10s +3.597 at 60.622, 5s30s +4.177 122.498.

- US$ remains stable near modest lows (BBDXY -.39 at 1200.81.)

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (-0.02), volume: $2.870T

- Broad General Collateral Rate (BGCR): 4.33% (-0.02), volume: $1.157T

- Tri-Party General Collateral Rate (TCR): 4.33% (-0.02), volume: $1.122T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $115B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $227B

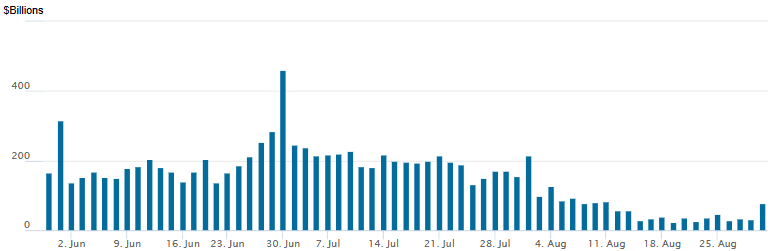

FED Reverse Repo Operation

RRP usage more than doubles to $77.898B going into month end with 26 counterparties this afternoon, from $31.966B yesterday. Compares to $22.344B on Tuesday, Aug 19 - lowest since April 5, 2021 vs. this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR Options continued to rotate around low delta call structures Friday, while Treasury options favored puts until a massive buyer of over 100,000 Oct 10Y calls arrived in the second half. Treasury futures drift near session lows, the short end of the SOFR strip saw modest support (SFRU5-SFRH7 trades +0.005 to +0.010). Projected rate cuts in turn continue to gain momentum vs. morning (*) levels: Sep'25 at -22.0bp (-21.2bp), Oct'25 at -35.6bp (-34.1bp), Dec'25 at -56.0bp (-54.9bp), Jan'26 at -68.1bp (-67.1bp).

SOFR Options:

+1,500 SFRM6/SFRU6 97.50/98.50/99.50 call fly strip, 14.0

+2,000 SFRM6 96.87/97.18 call spd vs. 0QM6 97.25/97.50 call spd

+8,000 0QU5 96.75 puts, 2.0

+10,000 SFRU5 96.12/96.25 call spds, 0.5 vs. 95.935/0.05%

Update, +10,000 SFRZ5 95.68/95.81/96.00/96.12 call condors, 3.5

1,275 SFRX5 96.00/96.12 call spds vs. 96.00/96.12 call spds

+3,000 0QH6 97.50/98.00 call spd w/ 0QM6 97.50/98.00 call spds, 17.0

+20,000 SFRZ5 96.18/96.43 1x2 call spds, 1.25

Block, 4,000 0QZ5 96.50/96.87 put spds vs. 3QZ5 96.25/96.62 put spds, 0.5 net

-3,000 SFRU5 96.06/96.18 call spds, 0.5 ref 95.895

+2,000 SFRU5 95.93/96.00/96.06 call flys, 0.5

+18,800 SFRU5 96.00/96.12 call spds, 1.0 ref 95.91/0.10%

+10,500 SFRU5 96.00/96.06 call spds, 0.5 ref 95.897

2,000 SFRZ5 96.37 calls ref 96.215

Treasury Options:

Update, +100,000 TYV5 114 calls, 12-13 ref 112-16.5/0.18%, total volume over 117k

+10,000 TYV5 108/109 put spds, 1.0

+1,000 wk1 FV 109.5 straddles, 17.5

1,120 TYX5 110.5/112.5 put spds ref 112-16

4,000 FVV5 109 puts, 14.5 last

+2,000 FVV5 108.25/109 put spds, 11.5

+20,000 FVV5 108.25/108.75 put spds, 6.5 ref 109-13.75

MNI BONDS: EGBs-GILTS CASH CLOSE: Curves Bear Steepen To End The Week

European curves bear steepened to close the week.

- The overall price action for the session was set from the start, with light bear steepening seen on both the UK and German curves from early trade.

- There was little reaction to national-level August flash inflation data, which was generally seen as being on the soft side for headline but core measures were mixed.

- Likewise, US data in the European afternoon was largely in line with consensus, not bringing much reaction on either side of the Atlantic.

- The German and UK curves both bear steepened, with Bunds slightly underperforming Gilts. For the week, both the UK (2Y yield -0.1bp, 10Y +2.9bp) and German (2Y yield -0.8bp, 10Y +0.2bp) curves twist steepened.

- Periphery/semi-core EGB spreads widened, with OATs outperforming and closing the week below the 80bp mark, rising around 9bp for the week on political concerns but below the 81.8bp post-Jan closing high set Wednesday.

- Next week's scheduled highlights include the Eurozone-wide inflation reading, BOE Treasury committee testimony, final PMIs, UK retail sales, and German factory orders.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.6bps at 1.94%, 5-Yr is up 1.4bps at 2.257%, 10-Yr is up 2.9bps at 2.724%, and 30-Yr is up 3.8bps at 3.336%.

- UK: The 2-Yr yield is up 0.7bps at 3.943%, 5-Yr is up 0.6bps at 4.103%, 10-Yr is up 2.3bps at 4.722%, and 30-Yr is up 3bps at 5.6%.

- Italian BTP spread up 2.1bps at 86.3bps / French OAT up 0.7bps at 79.3bps

MNI OPTIONS: Euribor, Sonia Put Structures Largely Bought To End Week

Friday's Europe rates/bond options flow included:

- ERZ5 98.00/97.87 put spread vs ERZ5 98.62/98.75 call spread, bought ps for 3.0 in 5k

- ERH6 97.87/97.75ps, bought for half in 6k

- ERU6 98.0625/97.9375/97.8125p fly, bought for 3 in 2.5k

- SFIV5 96.25/96.35cs vs 96.05p, bought the cs for 0.75 in 4k

MNI FOREX: USD Index Set to Close at Unchanged Levels This Week

- The USD index has edged lower on Friday, as the stagflationary picture painted by the U.S PCE & Chicago PMI data as well as ongoing uncertainty surrounding Fed independence weigh on the greenback. This has culminated in the dollar index returning to very similar levels to last week’s close.

- Overall, markets are adhering to the most recent dovish tilt from the Fed, however, the significance of the upcoming US data (NFP and CPI) before the September meeting, is keeping bearish dollar momentum in check for now.

- NZDUSD strength stands out today, as the pair extends its bounce from firm pivot support at 0.5800 to around 1.8%. However, as bearish trend conditions remain overall, this might suggest that good supply is seen into 50-day EMA resistance around 0.5930. There have been some primary signs on Friday of momentum stalling above 1.1100 for AUDNZD, however, look for dips back towards 1.1000/1.1030 to be well supported.

- For the majors, USDJPY has been happy to oscillate either side of 147.00, while the late dollar weakness has helped propel EURUSD back to the 1.17 handle. For the latter, French political concerns leave us moderately lower on the week, however, a false break of key 50-day EMA support on Wednesday keeps bullish trend conditions firmly intact for now.

- GBP remains a relative underperformer to end the week, remaining down 0.07% at 1.3500 despite a bounce from 1.3446 session lows. This dynamic has allowed EURGBP to extend its most recent recovery, to test resistance at 0.8674. A break above this level would signal a stronger reversal, placing the cross at its highest levels in three weeks.

- Next week’s calendar will undoubtedly be centered around the US employment report on Friday. Elsewhere, US ISM PMIs are also scheduled, as well as Australia GDP and Swiss CPI.

MNI US STOCKS: Late Equities Roundup: Tech, Industrials, Discretionary Shares Weigh

- Stocks remain moderately weaker late Friday, inside ranges as indexes scale off this week's record or near record highs ahead of the weekend - not to mention month end position squaring. Currently, the DJIA trades down 121.93 points (-0.27%) at 45515.24, S&P E-Minis down 49.75 points (-0.76%) at 6467.75, Nasdaq down 267.5 points (-1.2%) at 21438.28.

- A mix of Information Technology, Industrials and Consumer Discretionary sector shares continued to lead the decline in late trade, chip makers weighing on the tech sector (partially tied to concerns over longer term AI support/need for high end chips): Dell Technologies -9.27%, Oracle -6.45%, Super Micro Computer -5.53% and Broadcom -4.38%.

- Lagging Industrials shares included: Caterpillar -4.22%, Axon Enterprise -3.70%, Uber Technologies -3.49% and Hubbell -3.23%. Weighing on the Discretionary sector: Ulta Beauty -6.78%, Tesla -3.73%, Norwegian Cruise Line -2.36% and eBay -2.09%.

- Meanwhile, Consumer Staples and Health Care sector shares continued to outperform: J M Smucker +3.18%, Brown-Forman +2.17%, Hershey Co +1.59% and General Mills +1.40%.

- Pharmaceuticals buoyed the Health Care sector: Molina Healthcare +2.67%, Elevance Health +2.49%, Centene Corp +1.87% and Quest Diagnostics +1.60%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Fresh Cycle High

- RES 4: 6600.00 Round number resistance

- RES 3: 6590.17 2.0% 10-dma envelope

- RES 2: 6543.75 2.00 proj of the Apr 7 - 10 - 21 price swing

- RES 1: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- PRICE: 6470.00 @ 1505 ET Aug 29

- SUP 1: 6436.50/6362.75 20-day EMA / Low Aug 20

- SUP 2: 6326.74 50-day EMA

- SUP 3: 6313.25 Low Aug 6

- SUP 4: 6239.50 Low Aug 1 and a key support

S&P E-Minis bulls remain in the driver’s seat and the contract traded to a fresh cycle high yesterday. This maintains the bullish price sequence of higher highs and higher lows. Moving average studies are in a bull-mode position too, highlighting a clear uptrend and positive market sentiment. Attention is on 6543.75, a Fibonacci projection. Support to watch lies at 6326.74, the 50-day EMA.

COMMODITIES

MNI OIL: Americas End of Day Oil Summary: Crude Declines

Oil markets pulled back Friday, after trading mostly rangebound for much of the day, selling off some of the Russia sanctions fear premium from yesterday. US total rig count 536, Baker Hughes says; US oil rig count up 1 to 412

- Kazakh oil flows from CPC terminal is in normal mode and oil is still flowing through still-operational CPC mooring. The system is receiving producers’ crude without limit.

- Russia expects that the US will continue its efforts within the Alaska agreements according to TASS and Russia assumes that contact with the US to discuss “mutual irritants may take place in coming weeks.

- Expectations of a Trump announcement on Russian-Ukraine yesterday saw oil prices move higher over sanctions fears. An announcement is yet to be made. Hopes of a Russia/Ukraine peace deal fade by the day, putting pressure on Trump to make good on his Russia secondary sanction oil threats.

- WTI Oct futures were down 0.9% at $64.00

- WTI Nov futures were down 1.0% at $63.45

MONDAY/TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 01/09/2025 | 0530/0730 | ** | Retail Sales | |

| 01/09/2025 | 0700/0900 | Employment and Unemployment (p) | ||

| 01/09/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/09/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/09/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/09/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/09/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/09/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 01/09/2025 | 0830/0930 | ** | BOE M4 | |

| 01/09/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/09/2025 | 0900/1100 | ** | EZ Unemployment | |

| 01/09/2025 | 1200/1400 | ECB Schnabel Chairs Panel at ECB Legal Conference | ||

| 01/09/2025 | 1400/1600 | ECB Cipollone Chairs Panel at ECB Legal Conference | ||

| 01/09/2025 | 1800/2000 | ECB Lagarde Speech at ECB Legal Conference | ||

| 02/09/2025 | 0130/1130 | Balance of Payments: Current Account | ||

| 02/09/2025 | 0900/1100 | ** | PPI | |

| 02/09/2025 | 0900/1100 | *** | EZ HICP Flash | |

| 02/09/2025 | 1130/1330 | ECB Elderson and Machado in Panel at ECB Legal Conference | ||

| 02/09/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 02/09/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 02/09/2025 | 1400/1000 | * | Construction Spending | |

| 02/09/2025 | 1400/1000 | * | Construction Spending | |

| 02/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 02/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/09/2025 | 1700/1300 | ** | US Treasury Auction Result for 52 Week Bill |