MNI ASIA MARKETS ANALYSIS: September Fed Cut Doubts Resurface

MNI (NEW YORK) -

HIGHLIGHTS:

- Hotter-than-expected US producer price data boosts dollar, bear flattens Treasury curve

- Equities recover post-PPI losses to close flat

- US data schedule remains active Friday including Retail Sales, with Trump-Putin summit to follow

US TSYS: Curve Bear Flattens As PPI Casts Slight Doubt On September Fed Cut

The Treasury cash curve bear flattened modestly Thursday, after strong producer price data cast doubt on Fed easing prospects.

- Early trade was very constructive, with 2 and 5-year yields hitting the lowest levels since early May.

- But the early pullback in yields soon gave way to bear flattening, with July's producer price report coming in much hotter than expected (headline 0.9% M/M vs 0.2% expected), pushing back against the post-CPI narrative that tariffs were not materializing as acutely as feared.

- Released alongside PPI, initial jobless claims were in-line (224k vs 225k expected), continuing to show a steady "low hiring, low firing" labor market dynamic.

- Fed speakers included hawkish 2025 FOMC voter and St Louis Fed President Musalem, who said it's too early for him to decide on whether to support a rate cut in September, while a 50bp cut would be "unsupported" by the fundamentals and the outlook.

- Overall, the day's developments meant a September Fed cut is no longer fully priced (23bp at writing, vs 26bp+ Weds), helping apply pressure on the short-end of the Treasury curve.

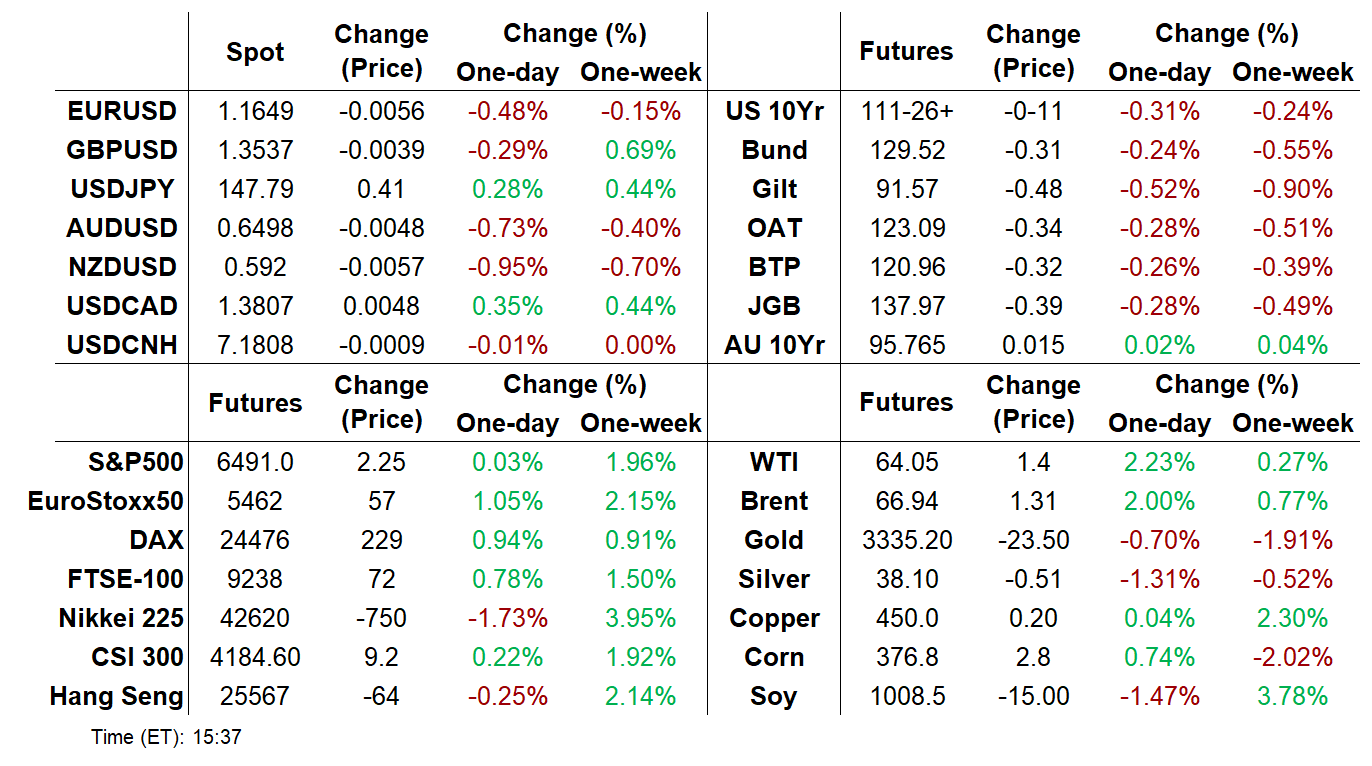

- Latest levels: The 2-Yr yield is up 6bps at 3.7345%, 5-Yr is up 5.4bps at 3.8154%, 10-Yr is up 5.4bps at 4.2868%, and 30-Yr is up 5.2bps at 4.8776%. Sep 10-Yr futures (TY) down 11.5/32 at 111-26 (L: 111-24.5 / H: 112-14)

- Friday's calendar includes several key data points including retail sales, import prices, industrial production, the Empire State manufacturing survey, and preliminary University of Michigan August consumer sentiment - not to mention the Trump-Putin summit in Alaska in late afternoon ET.

STIR: Implied Fed Easing Fades Slightly On Strong PPI

A September Fed rate cut is no longer quite fully priced, after seeing 26+bp in easing priced by Wednesday's close.

- Above-expected producer price data saw Fed funds futures sell off across the board Thursday, with cumulative cuts through the next six meetings reduced by 7-8bp. For September, it's now 23-24bp, so still almost a sure thing.

- However at least one current FOMC voter, St Louis's Musalem, sounded less than enthusiastic about the prospect of a cut ("too early to say exactly what policy I will be able to support" at the meeting).

- On the week, Fed easing expectations are roughly unchanged however, with today's move merely reversing the dovish post-CPI shift on Tuesday and Wednesday.

- Plenty of data Friday that could move the needle, including July retail sales and UMichigan consumer inflation expectations.

- Current implied easing (cumulative) by meeting: 23bp Sept, 38bp Oct, 58bp Dec, 69bp Jan.

| Meeting | Current FF Implieds (%), LH | Cumulative Change From Current Rate (bp) | Incremental Chg (bp) | Yesterday (Aug 13) | Chg Since Then (bp) | Start of Week | Chg Since Then (bp) |

| Sep 17 2025 | 4.10 | -23.4 | -23.4 | 4.06 | 3.4 | 4.10 | -0.7 |

| Oct 29 2025 | 3.95 | -38.3 | -14.9 | 3.90 | 4.9 | 3.95 | -0.6 |

| Dec 10 2025 | 3.75 | -57.6 | -19.3 | 3.69 | 6.3 | 3.75 | 0.1 |

| Jan 28 2026 | 3.64 | -68.8 | -11.2 | 3.57 | 7.2 | 3.65 | -0.6 |

| Mar 18 2026 | 3.51 | -81.9 | -13.1 | 3.44 | 7.4 | 3.53 | -2.0 |

| Apr 29 2026 | 3.44 | -88.7 | -6.8 | 3.37 | 7.5 | 3.46 | -1.7 |

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

US TSYS/OVERNIGHT REPO: Secured Rates Dip Between Treasury Settlement Days

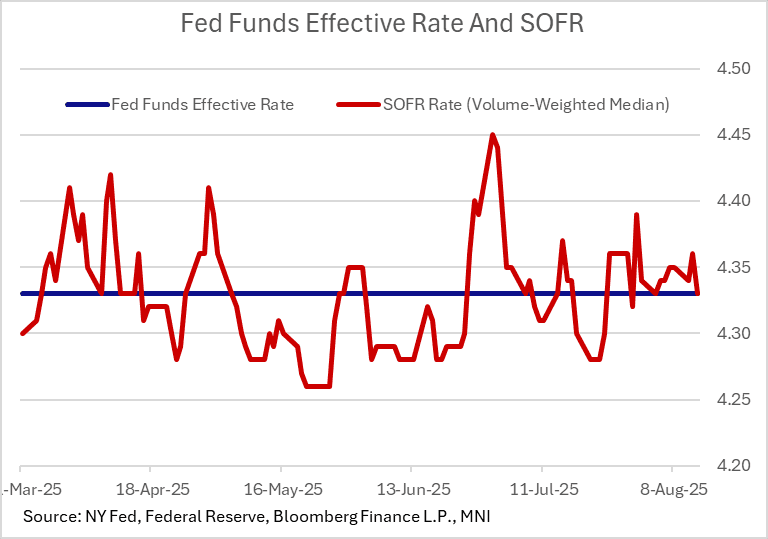

Secured rates pulled back sharply Wednesday, reversing Tuesday's Treasury supply-led rise. SOFR fell 3bp to 4.33%, with BGCR and TGCR down 2bp each. That's the lowest SOFR rate since Aug 4.

- While Wednesday's softening was expected, pressures are expected to start rebuilding today amid $42B in net bill settlements, followed by $35B in coupon settlements Friday.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.33%, -0.03%, $2796B

* Broad General Collateral Rate (BGCR): 4.32%, -0.02%, $1177B

* Tri-Party General Collateral Rate (TGCR): 4.32%, -0.02%, $1146B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $116B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $267B

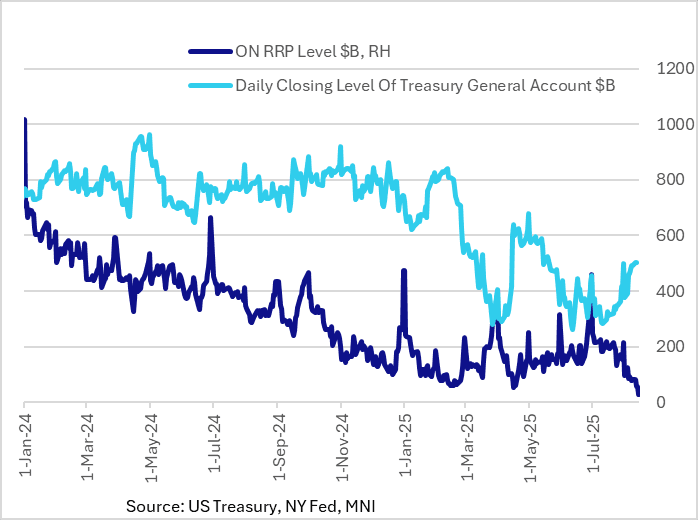

US TSYS/OVERNIGHT REPO: ON RRP Takeup At 4+ Year Lows As Treasury Cash Rebuilds

Takeup of the New York Fed's overnight reverse repo facility fell by $28.4B Thursday to $28.8B, the lowest since April 2021. Similarly, the number of counterparties fell to a post-2021 low of just 14.

- Aside from the usual month-end pickup, takeup has been falling in pronounced fashion as Treasury has begun ramping up bill sales to rebuild the Treasury General Account after the lifting of the debt limit in the first week of July.

- At current levels, ON RRP is basically negligible compared with a peak of over $2.5T at the end of 2022.

- We will be interested to see the Fed's weekly balance sheet release later today for the current level of system reserves versus ON RRP and TGA. So far reserves have remained relatively unchanged despite a sharp rise in the TGA, with ON RRP instead falling.

US Options Roundup - Aug 14 2025

Thursday's US bond/rate options flow included:

- SFRM6 98.50c with SFRU6 98.62c strip, bought for 6.5 in 10k

- SFRQ5/U5 96.00c spread, traded 4 in 4k

- SFRU5 96.12/96.25cs, bought for 1.25 in 15k total (note this is a 50bp September Fed cut play - has been bought for 1.25 to 1.625 in over 230k

in the past week or so) - SFRU5 96.06/96.12cs, traded 1.25 and 1.5 in 6k

- SFRU5 95.81/0QU5 96.62p spread, traded 0.5 for the front in 2.5k (on Block).

- SFRU5 96.25c, traded 0.75 in 2k.

- SFRV5 97.00c, traded 1 in 2.5k.

- SFRX5 96.06p vs 96.43/96.68cs, traded 0.5 for cs in 2.5k (on Block).

- SFRZ5 97.00c, traded 2.5 in 8k.

- SFRZ5 96.37/96.43/96.50/96.56c condor, traded 1 in 1.5k.

- 0QQ5 96.87/96.93cs 1x2, traded half in 2k.

- 0QZ5 96.68/96.93/97.18c fly, traded 4 in 2.5k.

Futures blocks of note:

- FVU5 4k blocked at 109-02.25 vs WNU5 940 blocked at 118-17, steepener

- TUU5 10K blocked at 103-31.375 vs WNU5 2K blocked at 118-28, flattener

EGBs-GILTS CASH CLOSE: US Pipeline Inflation Snuffs Out Early Gains

Unexpectedly strong US pipeline inflation data snuffed out a nascent European bond rally Thursday.

- After a small dip in yields in a relatively quiet European morning session, global yields spiked led by Treasuries in early afternoon after US producer price inflation came in much higher than expected in July, pointing to potential pipeline CPI pressures from tariffs.

- The brunt of the sell-off was felt by the long end, with curves bear steepening.

- Gilts underperformed Bunds on the day, with UK monthly economic activity data and headline Q2 GDP readings largely firmer-than-expected.

- 10Y Gilts reversed the prior session's rally, with yields closing at the highest level since Jul 28.

- Eurozone data was less impactful: Q2 GDP confirmed flash estimates at 0.1% Q/Q, with quarterly employment also growing at 0.1%; June industrial production was weaker-than-expected.

- Periphery / semi-core EGB spreads closed slightly wider, reversing early session tightening.

- Friday's calendar contains neither top-tier data nor ECB/BOE speakers, putting most of the global focus on the US-Russia talks over Ukraine due after the European cash close.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.2bps at 1.946%, 5-Yr is up 2.6bps at 2.283%, 10-Yr is up 3.2bps at 2.712%, and 30-Yr is up 3.9bps at 3.267%.

- UK: The 2-Yr yield is up 4.5bps at 3.908%, 5-Yr is up 4.3bps at 4.052%, 10-Yr is up 5.2bps at 4.641%, and 30-Yr is up 6.4bps at 5.492%.

- Italian BTP spread up 0.8bps at 77.9bps / French OAT up 0.3bps at 65.9bps

EUROPE OPTIONS: Europe Flow On The Thin Side Thursday

Thursday's Europe bond/rate options flow included:

- ERZ5 98.25/98.50cs, bought for 2 in 3.5k

FOREX: Hotter PPI Stalls USD Downtrend

- A hotter PPI print helped stall the USD's recent slippage - snapping the losing streak in the USD Index that had resulted in a break of support. PPI came in higher than forecast on both a final demand and ex-food and energy basis, helping undo a large part of the market reaction to CPI earlier in the week. This should feed through positively into the latest PCE view at the Fed, and could limit the space for easing later this year - although OIS markets still showed a September rate cut as the likely outcome.

- AUD held losses into the Thursday close, erasing any marginal gains on the labour market data. Thursday price action countered the gradual uptrend in AUDUSD throughout this month, and counters any support for the currency stemming from risk sentiment - as US equities remain at alltime highs. This raises the question of whether AUD would be able to capitalize on any further risk-on, for example driven through a potential Russia-Ukraine ceasefire.

- Stronger-than-expected Q2 UK GDP of 0.3% Q/Q led EURGBP on track for its sixth consecutive daily decline, with breach of key support through the 0.8611-13 level further pressuring the pair which now sits at its lowest reading since early July. This leaves markets contemplating a deeply divided MPC, and Bailey's appearance at Jackson Hole next week, as well as UK CPI is scheduled for next Wednesday, will be carefully watched.

- JPY outperformed throughout the trading day, with recent weakness putting the price through support drawn off the early August lows as well as 146.71, a key retracement. Price action this week marks a full reversal of the previously overbought condition, keeping the downside argument in focus.

- Just ahead of the Friday close, Presidents Trump and Putin are set to meet in Alaska. The meeting is set to continue for an indeterminate period of time before, reportedly, the Presidents will hold a joint press conference (however Trump stated that a joint appearance would be contingent on results of the meeting itself). Any appearance is likely to be well after the market close, leaving any reaction to Monday trade.

- On data, Friday focus shifts to the Japanese GDP print for Q2, Chinese retail sales and industrial production stats for July, rounded off with US retail sales, industrial production and prelim UMich sentiment data. There are no central bank speakers of note.

FX OPTIONS: Expiries for Aug15 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1590-10(E1.3bln), $1.1750(E1.2bln)

- USD/JPY: Y147.00($572mln)

- GBP/USD: $1.3500-20(Gbp630mln)

- AUD/USD: $0.6485-00(A$681mln), $0.6523(A$562mln)

- USD/CAD: C$1.3910($995mln)

- USD/CNY: Cny7.5000($1.7bln)

EQUITIES: Major Indices Set To Close Flat After Recovering Post-PPI Drop

Major equity indices were set to record a flat session Thursday, following fresh closing records in the Nasdaq and S&P 500 Wednesday. Early gains were fully reversed after above-expected US PPI data, but stocks clawed back over the course of the rest of the session.

- In contrast with strong sectoral breadth Wednesday, today's session saw most S&P 500 sectors in the red.

- That was led by materials which had outperformed Wednesday but were lagging Thursday (-0.9%), with industrials neck-and-neck (-0.9%); consumer discretionary and communication services stocks led gains (up 0.5% apiece).

- Top performers had no particular theme: top was Texas Pacific Land (+4.1%), followed by drugmaker Eli Lilly (+3.5%) and Amazon (3.3%). Down double-digits were Tapestry (-14%, with tariff impact cited) and Amcor (-11%, missed Q4 earning estimates), though among larger market cap companies, Deere and Co's 6.5% drop stood out (cited cautious farmer consumers in paring its full-year earnings outlook).

- Latest futures levels: Dow Jones mini down 27 pts or -0.06% at 44994, S&P 500 mini up 0.75 pts or +0.01% at 6489, NASDAQ mini down 19 pts or -0.08% at 23926.

COMMODITIES: Crude Rebounds, Gold/Silver Pull Back Following US PPI Data

- WTI has rebounded today as the market focuses on the outcome of a Putin-Trump meeting tomorrow.

- WTI Sep 25 is up by 2.1% at $63.9/bbl.

- Prices have trended lower so far in August on excess supply concerns while the market is watching Ukraine developments closely. Trump said today that he placed the odds of failure at tomorrow’s meeting at 25%, saying that he doesn’t think he will get an immediate ceasefire.

- WTI futures remain below the 50-day EMA and bear trigger at $65.02, exposing $58.17, the May 30 low. On the upside, $69.41 marks the 50.0% retracement of the Jun 23-24 downleg - an important level on any further recovery from here.

- Meanwhile, spot gold has fallen by 0.5% to $3,338/oz, bringing the yellow metal to its lowest level since Aug 1.

- The move followed stronger-than-expected US PPI inflation data, which saw the market pare September rate cut expectations.

- For gold, short-term pullbacks are considered corrective - for now - and the bull cycle that started Jun 30 remains intact. However, a clear break of the 50-day EMA at $3,334.9 would signal scope for a deeper retracement to the next key support at $3,248.7, the Jun 30 low.

- Silver has also fallen by 1.2% to $38.1/oz amid the increase in US yields and firmer dollar. Initial support is seen at $36.216, the Jul 31 low, while first resistance is at $39.655 a Fibonacci projection.

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 15/08/2025 | 0430/1330 | ** | Industrial Production | |

| 15/08/2025 | 0700/0900 | * | CH Flash GDP | |

| 15/08/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/08/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 15/08/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/08/2025 | 1315/0915 | *** | Industrial Production | |

| 15/08/2025 | 1400/1000 | * | Business Inventories | |

| 15/08/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 15/08/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 15/08/2025 | 1400/1000 | * | Business Inventories | |

| 15/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 15/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 15/08/2025 | 2000/1600 | ** | TICS |