BONDS: EGBs-GILTS CASH CLOSE: US Pipeline Inflation Snuffs Out Early Gains

Aug-14 16:28

Unexpectedly strong US pipeline inflation data snuffed out a nascent European bond rally Thursday.

- After a small dip in yields in a relatively quiet European morning session, global yields spiked led by Treasuries in early afternoon after US producer price inflation came in much higher than expected in July, pointing to potential pipeline CPI pressures from tariffs.

- The brunt of the sell-off was felt by the long end, with curves bear steepening.

- Gilts underperformed Bunds on the day, with UK monthly economic activity data and headline Q2 GDP readings largely firmer-than-expected.

- 10Y Gilts reversed the prior session's rally, with yields closing at the highest level since Jul 28.

- Eurozone data was less impactful: Q2 GDP confirmed flash estimates at 0.1% Q/Q, with quarterly employment also growing at 0.1%; June industrial production was weaker-than-expected.

- Periphery / semi-core EGB spreads closed slightly wider, reversing early session tightening.

- Friday's calendar contains neither top-tier data nor ECB/BOE speakers, putting most of the global focus on the US-Russia talks over Ukraine due after the European cash close.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.2bps at 1.946%, 5-Yr is up 2.6bps at 2.283%, 10-Yr is up 3.2bps at 2.712%, and 30-Yr is up 3.9bps at 3.267%.

- UK: The 2-Yr yield is up 4.5bps at 3.908%, 5-Yr is up 4.3bps at 4.052%, 10-Yr is up 5.2bps at 4.641%, and 30-Yr is up 6.4bps at 5.492%.

- Italian BTP spread up 0.8bps at 77.9bps / French OAT up 0.3bps at 65.9bps

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

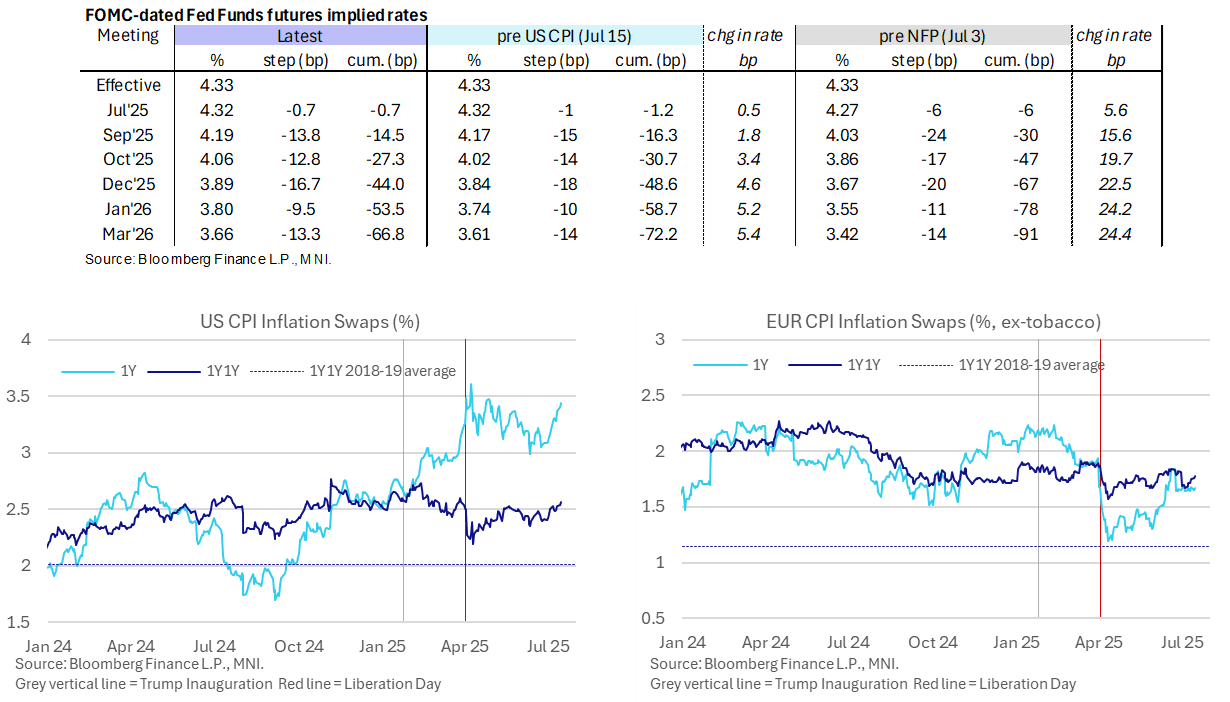

STIR: Fed Rates Hold Hawkish Shift On CPI Along With Short-Term Inflation Swaps

Jul-15 16:17

- Fed Funds futures are holding their belated push higher after a US CPI report for June which showed signs of increasing passthrough to consumer prices from tariffs.

- Cumulative cuts from 4.33% effective: 0.5bp Jul, 14.5bp Sep (vs 16.5bp pre CPI), 27.5bp Oct, 44bp Dec (vs 48.5bp), 53.5bp Jan and 67bp Mar (vs 72bp).

- The Dec 2025 implied rate is now 22.5bp higher than prior to the June non-farm payrolls report one and a half weeks ago.

- The CPI report extends a marked increase in short-term US inflation expectations. The 1Y inflation swap is 3.5bp higher today at 3.44%, following the 3.29% averaged through much of last week and 3.12% in the holiday-shortened week before that into Independence Day. This peaked at 3.61% (looking at closes) in the week after US reciprocal tariff announcements in April.

- Recent increases have been mostly confined to just 1Y, on the assumption that tariff increases have short-lived inflationary impacts, although 1Y1Y rates are drifting higher as well so it’s not entirely in isolation. See the below charts including a comparison with EU inflation swaps over the same period.

FOREX: USDJPY Leads Impressive Greenback Rally Following US Inflation Data

Jul-15 16:11

- Despite the initial dip lower for the greenback following the softer-than-expected core and supercore readings for US inflation, a deeper dive into the data prompted a swift and significant recovery for the greenback. A broader increase in core goods across 56 items for a second month, with a median increase of 0.44% M/M in June is another marked acceleration, threatening to delay the Fed hitting their inflation target.

- With US yields rising in reflection of this dynamic, the broad dollar reversal higher was swift and then persistent throughout the session. The most recent USD index recovery has now extended to around 2.3% from cycle lows printed on July 01. The rally marks the cleanest evidence yet of a material break of the downtrend posted off the February high, bolstered by a breach of the 20-day EMA.

- The rally has been led by a powerful 0.75% advance for USDJPY, where topside momentum was exacerbated on a break of the June and July highs at 148.03 and 148.65 respectively. The peak so far today stands at 149.02 as the market continues to extend its short squeeze, and the next focus will be on 149.38, the 50.0% retracement of the Jan 10 - Apr 22 bear leg, and 150.49, the Apr 2 high.

- While JPY weakness stands out today, the Swedish krona sits at the bottom of the G10 leaderboard. A continued reversal following last week’s inflation data provides an interesting positioning dynamic here, as the market may prefer to be positioned for a dovish Riskbank ahead.

- The likes of EUR, AUD and NZD have all declined around 0.4% against the dollar. EURUSD has hit fresh pullback lows towards the 1.16 mark as downside momentum has picked up following a breach of the 20-day EMA.

- Although sterling moderately outperforms, GBPUSD has breached important trendline support below 1.3430, drawn from the Jan 13 low. A clear break of the trendline would strengthen a bearish threat and expose 1.3335, the May 20 low. Sentiment will be affected by both CPI and labour market reports, due on Wed and Thu respectively. US PPI is also due.

FED: US TSY TO SELL $80.000 BLN 8W BILL JUL 17, SETTLE JUL 22

Jul-15 16:05

- US TSY TO SELL $80.000 BLN 8W BILL JUL 17, SETTLE JUL 22