OPTIONS: Expiries for Aug15 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1590-10(E1.3bln), $1.1750(E1.2bln)

- USD/JPY: Y147.00($572mln)

- GBP/USD: $1.3500-20(Gbp630mln)

- AUD/USD: $0.6485-00(A$681mln), $0.6523(A$562mln)

- USD/CAD: C$1.3910($995mln)

- USD/CNY: Cny7.5000($1.7bln)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Back From Highs As Details Of U.S. CPI Weigh

Gilt futures fade from highs after initially registering fresh session bests in the wake of the U.S. CPI data, generally taking cues from Tsys.

- Tariff passthrough signals in the U.S. CPI M/M readings made for an eventual hawkish move in the wake of the data.

- Elsewhere, the White House has played down reports suggesting that U.S. President Trump encouraged Ukraine to strike Moscow in a recent conversation, which may have removed a little geopolitical risk premium from bonds.

- Futures back to 91.85 after trading as high as 92.24. 20-day EMA (92.29) untouched, bearish technical theme intact.

- Yields last flat to 3bp higher, curve flattens.

- BoE-dated OIS pricing sits at the dovish end of the recent range but is a handful of bp back from the extremes witnessed earlier this week, showing ~55bp of cuts through year-end (vs. ~58bp yesterday morning).

- Early July highs intact and untested in SFIZ6.

- This week’s labour market and inflation data has taken on added significance after Governor Bailey’s interview with The Times at the weekend in which he noted that more easing could be needed if the labour market weakens more than expected.

- Our full preview of this week’s key UK data releases is here.

- We don’t expect much new from BoE Governor Bailey in his Tuesday evening address, while much of Chancellor Reeves’ planned fiscal commentary has been leaked to the press ahead of the Mansion House event.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 3.998 | -21.9 |

Sep-25 | 3.928 | -28.9 |

Nov-25 | 3.760 | -45.7 |

Dec-25 | 3.670 | -54.8 |

Feb-26 | 3.539 | -67.9 |

Mar-26 | 3.505 | -71.3 |

FED: Further Critique From Trump

U.S. President Trump continues to post to Truth Social: "Fed should cut Rates by 3 Points. Very Low Inflation. One Trillion Dollars a year would be saved!!!"

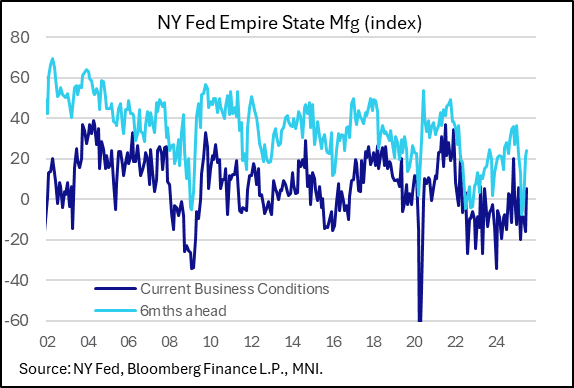

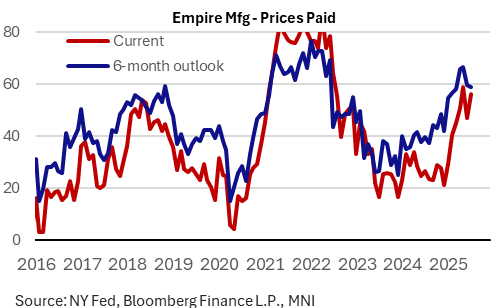

US DATA: Empire Manufacturing Shows Signs Of Stability, But Inflation Elevated

The New York Fed's Empire State Manufacturing Survey for July was stronger than expected, with the headline general business conditions index jumping 21.5 points to 5.5 (-9.5 expected). This marked the first positive reading since February and a slightly above-average reading vs the last 5 years.

- To be sure, this is more indicative of a recovery than a nascent boom. There seems to have been significant relief over the alleviation of some tariff policy uncertainty, which of course was responsible for sentiment deteriorating between March and June - though this may not repeat in August's report if the US fails to reach "deals" with major key trading partners for the NY region including Canada.

- July's was a roundly constructive Empire report across subcategories. Per the report, "New orders edged higher and shipments increased. Delivery times lengthened, and supply availability continued to worsen. Inventories grew significantly. Employment expanded for a second consecutive month, and the average workweek also increased. ... Capital spending plans grew. Firms remained fairly optimistic about the outlook."

- Indeed, one of the survey highlights was that employment was the highest since 2022, rising 4.2 points to 9.2.

- Less positive: inflationary pressures remained relatively acute, and in a potential warning sign, supply availability deteriorated (-11.0 from -8.3).

- Current prices paid resumed their uptrend, at 56.0 after falling to 46.8 in June from the recent peak of 59.0 in May, though current prices received dipped to 25.7 from 26.6. Future prices paid (6-months ahead) moderated for a 2nd month, down 0.9 points to 58.7; future prices received ticked up 0.9 points to 42.2 but both remain well below their April-May peaks.