FOREX: Hotter PPI Stalls USD Downtrend

- A hotter PPI print helped stall the USD's recent slippage - snapping the losing streak in the USD Index that had resulted in a break of support. PPI came in higher than forecast on both a final demand and ex-food and energy basis, helping undo a large part of the market reaction to CPI earlier in the week. This should feed through positively into the latest PCE view at the Fed, and could limit the space for easing later this year - although OIS markets still showed a September rate cut as the likely outcome.

- AUD held losses into the Thursday close, erasing any marginal gains on the labour market data. Thursday price action countered the gradual uptrend in AUDUSD throughout this month, and counters any support for the currency stemming from risk sentiment - as US equities remain at alltime highs. This raises the question of whether AUD would be able to capitalize on any further risk-on, for example driven through a potential Russia-Ukraine ceasefire.

- Stronger-than-expected Q2 UK GDP of 0.3% Q/Q led EURGBP on track for its sixth consecutive daily decline, with breach of key support through the 0.8611-13 level further pressuring the pair which now sits at its lowest reading since early July. This leaves markets contemplating a deeply divided MPC, and Bailey's appearance at Jackson Hole next week, as well as UK CPI is scheduled for next Wednesday, will be carefully watched.

- JPY outperformed throughout the trading day, with recent weakness putting the price through support drawn off the early August lows as well as 146.71, a key retracement. Price action this week marks a full reversal of the previously overbought condition, keeping the downside argument in focus.

- Just ahead of the Friday close, Presidents Trump and Putin are set to meet in Alaska. The meeting is set to continue for an indeterminate period of time before, reportedly, the Presidents will hold a joint press conference (however Trump stated that a joint appearance would be contingent on results of the meeting itself). Any appearance is likely to be well after the market close, leaving any reaction to Monday trade.

- On data, Friday focus shifts to the Japanese GDP print for Q2, Chinese retail sales and industrial production stats for July, rounded off with US retail sales, industrial production and prelim UMich sentiment data. There are no central bank speakers of note.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Continues To Appreciate

- RES 4: 175.43 High Jul 11 ‘24 and a key medium-term resistance

- RES 3: 174.86 1.764 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 2: 173.43 High Jul 12 ‘24

- RES 1: 173.08 High Jul 15

- PRICE: 172.89 @ 16:42 BST Jul 15

- SUP 1: 170.81 Low Jul 11

- SUP 2: 169.75 20-day EMA

- SUP 3: 168.46 Low Jul 1

- SUP 4: 167.09 50-day EMA

The trend condition in EURJPY is unchanged, a bull cycle is in play and today’s climb reinforces current conditions. Fresh cycle highs confirm a resumption of the uptrend and maintain the price sequence of higher highs and higher lows. Note that MA studies are in a bull-mode position, highlighting a dominant medium-term uptrend. Sights are on 173.43, the Jul 12 ‘24 high. Support to watch lies at 169.75, the 20-day EMA.

FED: Boston's Collins: Tariffs To Move Economy Away From Favorable Conditions

Boston Fed President Collins (2025 voter) reiterated in a speech Tuesday that she advocates an "actively patient" approach to policymaking. Speech text here. Note that she'd already implied in a previous appearance that she was one of two FOMC participants to only pencil in 1 cut in 2025, putting her slightly on the hawkish side of the median (recall 10 of 19 participants in June saw 2 or more cuts).

- Collins writes: "In my view, the economy continues to be in a good place overall, close to the Congressionally mandated objectives of price stability and full employment. However, going forward, I expect to see some upward pressures on inflation, as well as some downward pressures on employment and economic growth."

- She acknowledges that "services inflation has continued to moderate, especially on a 12-month basis, despite continued unevenness. This moderation reflects a more balanced labor market". But core goods inflation "has picked up some, recently, and is currently running above the rates that prevailed before the pandemic. Some of these recent movements in goods inflation are likely tariff-related".

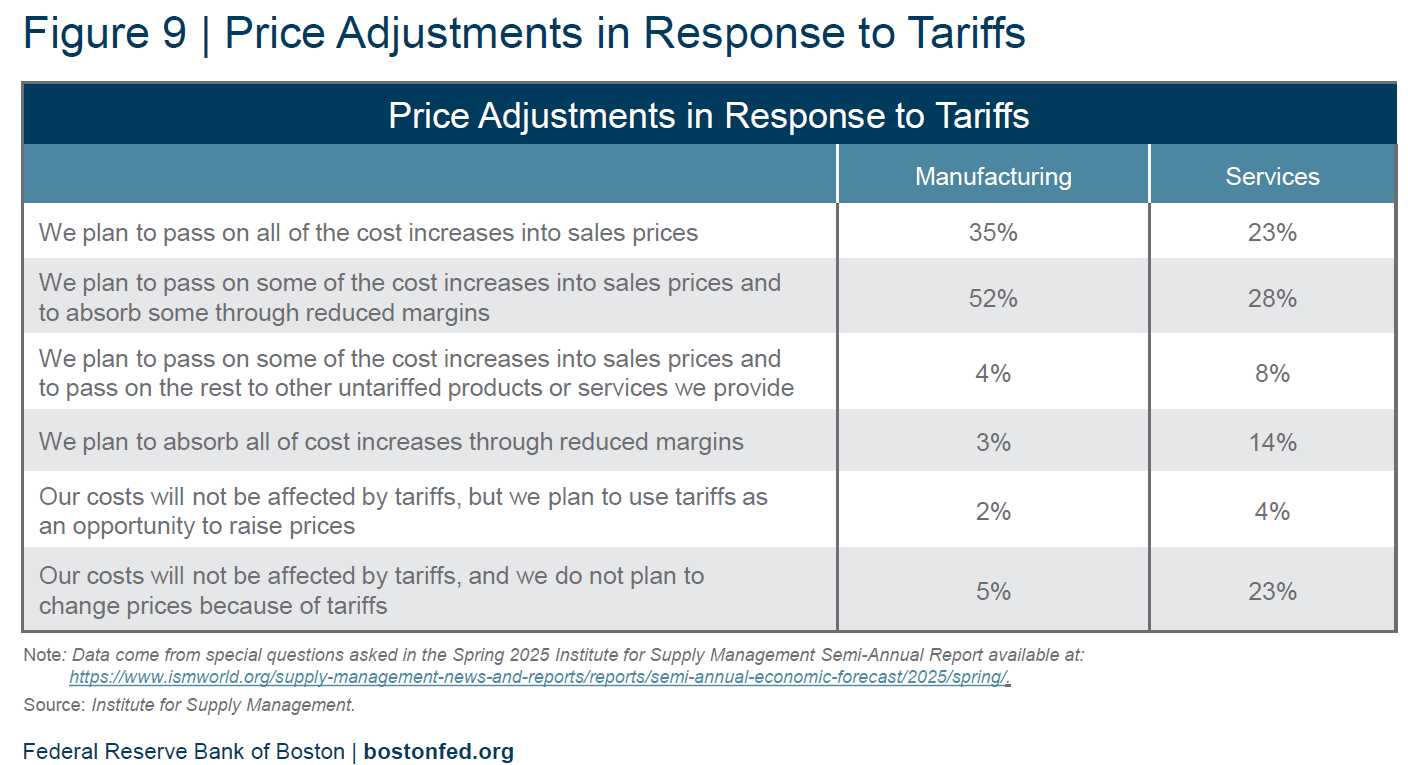

- She notes that "most" firms "plan to pass along some – even if not necessarily all – of the tariff costs" (pointing to ISM data - see table below) while the "typical household has the resources to at least partly offset a tariff-induced loss in purchasing power".

- She concludes that "it seems likely that core PCE inflation will be in the vicinity of 3 percent by year’s end, before resuming its decline. Concerning the labor market side of our mandate, tariffs should slow demand and hiring, though not necessarily by a large amount." Overall, "it seems likely that the economy will move away, at least temporarily, from the favorable conditions I have just described. Tariff policy is the main driver, with higher broad-based tariffs than last year likely leading to a rise in inflation, higher unemployment, and slower GDP growth."

- On the labor market not being a significant source of inflationary pressures, "when adjusted for productivity, the pace of [Employment Cost Index] growth has been running around 2 percent recently, which is consistent with the Fed’s 2 percent inflation target. Therefore, even though some indicators show wages still rising somewhat faster than before the pandemic, given recent productivity developments, I do not see wage growth as placing additional pressure on inflation."

US STOCKS: Late Equities Roundup: Chip Makers Buoyed as Export Curbs Lifted

- Stocks continue to trade near steady (SPX eminis) to mixed late Tuesday, the tech-heavy Nasdaq outperforming after the White House rescinded a ban on high speed chips to China. At the moment, the DJIA trades down 327.71 points (-0.74%) at 44134.32, S&P E-Minis down 6 points (-0.1%) at 6305.25, Nasdaq up 119.8 points (0.6%) at 20760.16.

- Semiconductor makers supported the the tech heavy Nasdaq after several were greenlighted for exports to China. Leading gainers included: Advanced Micro Devices +6.52%, NVIDIA +4.07%, Broadcom +2.38%, KLA Corp +2.15% and Lam Research +2.02%.

- On the flipside, the DJIA continued to underperform in late trade with the Materials sector, specifically mining stocks w/ Gold lower, and Health Care sectors weighed by pharmaceuticals.

- Weighing on the Materials sector: Newmont Corp -6.15%, Freeport-McMoRan -3.62%, Vulcan Materials -2.59% and Albemarle -2.21%. Pharmaceuticals weighed on the Health Care sector: Agilent Technologies -5.08%, Regeneron Pharmaceuticals -4.10%, Moderna -3.80%, Eli Lilly -3.51% and Biogen Inc -3.34%.

- Individually, some banks and services underperforming after reporting earnings this morning, namely: State Street Corp -6.38%, Wells Fargo -6.26%, Blackrock -5.15%, Invesco -2.77% and American Express -2.70%.

- Earnings announcements expected early Wednesday: Prologis, Progressive, First Horizon, PNC Financial Services, Bank of America Corp, Johnson & Johnson, Goldman Sachs and Morgan Stanley. After the close: United Airlines Holdings, Rexford Industrial Realty, Alcoa Corp and Kinder Morgan.