MNI ASIA MARKETS ANALYSIS: CPI Inflation Softer Than Expected

HIGHLIGHTS

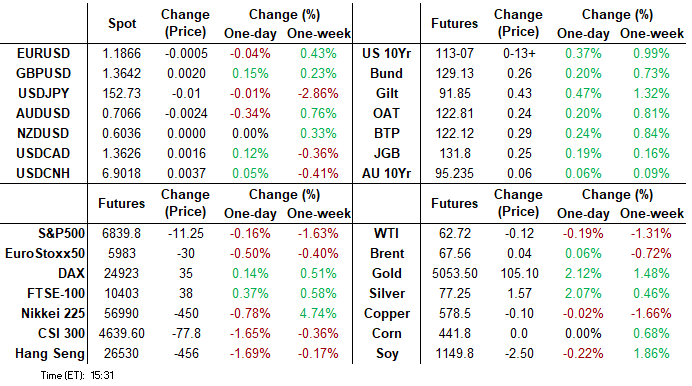

- Treasuries look to finish higher/off highs as markets continue to digest Friday's softer-than-expected CPI data across the board for the most part, though an upside beat in supercore.

- The dollar index marginally weaker, allowing the DXY to have a fourth consecutive session of consolidating price action following the impressive 0.8% move south on Monday. Greenback weakness has been most notable against the Japanese yen following Japan’s election last Sunday.

- Stocks have rebounded from early Friday selling, partially position squaring ahead of the weekend, while headlines of privately held AI company Anthropic planning on going public spurred additional selling in the first half.

- Chinese Lunar New Year Holiday - Markets will be shut Monday Feb 16th through Monday Feb 23rd as China celebrates the Lunar New Year, ushering in Year of the Horse.

US TSYS

MNI US TSYS: Softer CPI Metrics Buoys Tsys, Rate Cut Pricing Gains Slightly

- Treasuries look to finish stronger/near highs - climbing to best levels since early December after this morning's CPI inflation measure for January came out softer than expected, though an upside beat in supercore (more on which in a moment). The Y/Y changes for headline and core CPI came in line/a little softer than expected.

- Core CPI 3-month: 2.52% annualized over the latest three months to January, following 1.70% to December (1.61% first reported) and 3.42% to September (3.64%).

- TYH6 trades 113-06 (+12.5) vs. 113-07.5 high - breaching 113-04 (76.4% of the Nov 25 - Jan 20 bear leg) and opening up 113-11 as next resistance, the Dec 1 ‘25 high.

- Curves mildly steeper after this morning's softer than expected CPI data. In turn - projected rate cut pricing gain slightly vs. late Thursday lows (*): Mar'26 at -2.6bp (-1.6bp), Apr'26 at -7.6bp (-6.6bp), Jun'26 at -21.5bp (-19.2bp), Jul'26 at -32.1bp (-28.6bp).

- The dollar index tilts very marginally in the red Friday, allowing the DXY to have a fourth consecutive session of consolidating price action following the impressive 0.8% move south on Monday. Greenback weakness has been most notable against the Japanese yen following Japan’s election last Sunday.

- Look ahead: US markets closed Monday for Presidents' Day holiday (Globex early close at 1300ET), Tuesday sees weekly ADP NER Pulse and NAHB Housing Market Index. Supreme Court announces Feb 20, 24 and 25 as next opinion days (appr 1000ET).

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.65% (+0.00), volume: $3.205T

- Broad General Collateral Rate (BGCR): 3.63% (+0.01), volume: $1.342T

- Tri-Party General Collateral Rate (TCR): 3.63% (+0.01), volume: $1.318T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $97B

- Daily Overnight Bank Funding Rate: 3.63% (+0.00), volume: $196B

FED Reverse Repo Operation - New Low

RRP usage retreats to lowest level since early 2021 at $0.377B with 3 counterparties this afternoon vs. $2.844B Thursday. Compares to prior low on December 12 low of $0.838B; last year's highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option trade near paired Friday with some standout call spread buying emerging in both. Underlying futures firmer after the bell, curves mildly steeper after this morning's softer than expected CPI data. In turn - projected rate cut pricing gain slightly vs. late Thursday lows (*): Mar'26 at -2.6bp (-1.6bp), Apr'26 at -7.6bp (-6.6bp), Jun'26 at -21.5bp (-19.2bp), Jul'26 at -32.1bp (-28.6bp).

SOFR Options:

+20,000 0QH6 96.50/96.62/96.75/96.87 put condors, 3.0

Block, 5,715 SFRZ6 97.50 calls, 21.0

+40,000 SFRU6 98.00/99.00 call spds, 3 ref 96.82

+12,000 SFRM6 96.31/96.37/96.43 put flys, 1.75

6,000 0QG6 96.87 puts, 1.0 ref 96.93

2,500 0QH6 96.50/96.75 2x1 put spds ref 96.93

+7,500 SFRU6 96.31/96.43 put spds, 2.25 ref 96.795

+10,000 SFRJ6 96.68/96.93 call spds, 2.5

+11,000 0QJ6 96.50/96.68/96.87 put flys, 5 ref 96.89

+2,500 SFRK6 96.43/96.56 2x1 put spds, 4.5 vs. 96.57/0.10%

+2,000 SFRM6 96.37/96.43/96.56 2x3x1 put flys, 1.25

1,500 SFRN6 96.43/96.56 2x3 put spds

1,500 SFRM6 96.43/96.62/96.75 call trees ref 96.56

2,000 0QH6 97.00 calls, 6.0 ref 96.91

Treasury Options:

-1,500 TYH6/TYJ6 113 straddle strip, 1-56

5,000 TYH6 112.75 puts, 6 ref 113-03

5,000 TYJ6 111.5/112/112.5 put trees, 1 ref 113-02.5

5,000 TYJ6 113/114 1x2 call spds

+12,000 TYJ6 112 calls, 119 vs. 113-01/0.73%

+30,000 TYH6 112.5/113.5 call over risk reversals, 4 net vs. 113-00/0.45%

over 11,500 TUJ6 104.75 calls, 7.5

2,000 TUJ6 104/104.25 2x1 put spds ref 104-18

over 14,300 TYH6 111.5 puts, 1

2,300 TUJ6 104.12 puts ref 104-15.12

+2,000 FVJ6 110.5/111.5 1x2 call spds, 1.5 vs. 109-14.25/0.10%

+7,200 TYH6 111.5/115 call over risk reversals, 1 net vs. 112-21/0.05%

-2,600 FVH6 110 calls, 3.5-4 ref 109-12.5

+3,750 FVJ6 110.25 calls, 13 vs. 109-11.75/0.10%

over 31,100 TYH6 113 calls, 12-14

2,200 TYJ6 114 calls vs. 111/112 put spds ref 112-21

-10,000 TYJ6 113.5 calls, 24 ref 112-20, total volume over 12,100

2,000 FVJ6 111.5 calls ref 109-12.75

3,000 USH6 116.5 puts vs. USJ6 116 puts, 51 net

5,000 TYJ6 111/112 put spds vs. 114 calls, 2 net

+1,400 USH6 119 calls vs. 2,800 115/116 put spds, 9-11 net ref 117-02

MNI BONDS: EGBs-GILTS CASH CLOSE: Rally Continues, Cementing Weekly Bull Flattening

Long-end European yields fell for a 4th consecutive session Friday, cementing a solid bull flattening move for the week.

- The key focus for the session was US inflation, and a softer-than-expected set of data triggered a rally in Treasuries that spilled over into Europe.

- Bunds underperformed Gilts overall however. German Defence Minister Klingbeil triggered a late sell-off when he did not rule out an exemption made to the debt brake rule for the country's raw material fund.

- Core EGBs gained on the day nonetheless; periphery/semi-core EGB spreads widened modestly.

- On the week, both the UK (2Y yield -3bp, 10Y -10bp) and German (2Y -5bp, 10Y -9bp) curves bull flattened.

- Ratings reviews for Austria (Moody's) and the Netherlands (also Moody's) feature after the cash close.

- UK macro takes centre stage next week, with the latest round of labour market, inflation, and retail sales data.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.4bps at 2.036%, 5-Yr is down 2.8bps at 2.337%, 10-Yr is down 2.4bps at 2.755%, and 30-Yr is down 1.7bps at 3.432%.

- UK: The 2-Yr yield is down 1bps at 3.593%, 5-Yr is down 3bps at 3.825%, 10-Yr is down 3.6bps at 4.416%, and 30-Yr is down 3.5bps at 5.223%.

- Italian BTP spread up 0.4bps at 60.9bps / French OAT up 1.2bps at 59.2bps

MNI OPTIONS: Call Spread Buying Prevalent In Sonia To Close The Week

Friday's Europe rates/bond options flow included:

- RXJ6 126/125ps, bought for 7 in 2k

- 0RM6 97.62/98.25RR, bought the call for -0.5 (receive) in 5k (ref 97.915, 30del)

- SFIJ6 96.70/96.75cs, bought for 0.75 in 9.5k

- SFIK6 96.70/96.75cs, bought for 0.75 in 5.5k

- SFIZ6 96.90/97.00cs vs 96.30/96.20ps, bought the cs for 2 in 3k

MNI FOREX: USDJPY Set to Post Near 3% Weekly Decline

- Friday’s session was an uneventful one for currencies, with the more stable risk backdrop having little impact across the G10 and the eagerly awaited US inflation data failing to spark any momentum for the major pairs. January brought softer-than-expected US CPI data across the board for the most part, though an upside beat in supercore. The Y/Y changes for headline and core CPI came in line/a little softer than expected.

- The dollar index tilts very marginally in the red Friday, allowing the DXY to have a fourth consecutive session of consolidating price action following the impressive 0.8% move south on Monday.

- Greenback weakness has been most notable against the Japanese yen following Japan’s election last Sunday. PM Takaichi’s convincing win has buoyed market hopes of both a more stable political backdrop and a more measured fiscal approach to policy. The stabilisation for JGB’s has fostered a substantial yen recovery, which has been exacerbated by positioning dynamics and thoughts that the BOJ’s March meeting could be live.

- After rallying at Monday’s open to 157.76, the aggressive selloff took us to within 17pips of the key 152.10 support and bear trigger. Despite an initial recovery Friday, spot has edged back to 152.80 ahead of the close, with the pair remaining to look vulnerable. The pre-October election close is at 147.47 and remains a significant downside target.

- AUDUSD has underperformed Friday to trade back below 0.7100, with this week’s rally falling just shy of the 2023 highs at 0.7158. Fresh cycle highs this week keep bullish conditions firmly intact, with dips remaining technically corrective at this juncture.

- Another notable mover this week has been the resilient Swiss Franc, with EURCHF printing below 0.9100 for the first time since the removal of the floor in 2015. Analyst notes have been surprisingly bullish CHF given the recent extremes and historical precedent for the SNB to comment on the strong levels of the franc, with one bank forecasting a move to 0.8700.

- Japan GDP and Eurozone industrial production data highlight a light calendar Monday, where volumes may be dampened due to China, the US and Canada out for national holidays.

MNI FX OPTIONS: Expiries for Feb16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1850(E1.2bln), $1.1875(E715mln)

- USD/JPY: Y154.40($599mln), Y155.00($518mln)

MNI US STOCKS: Late Equities Roundup - Off Early Lows

- Stocks have rebounded from early Friday selling, partially position squaring ahead of the weekend, while headlines of privately held AI company Anthropic planning on going public spurred additional selling in the first half.

- While Financials, Communication Services and Information Technology sector shares continue to lead late session declines, Materials and Crypto currency shares led the rebound in the second half.

- Gold rallied back over $5,000.0/oz to $5,035/oz Friday helping mining stocks buoy the Materials sector while a strong bounce in Bitcoin by over 4.15% supported the Financial Services sector.

MNI EQUITY TECHS: E-MINI S&P: (H6) Reversal Lower Exposes Key Support

- RES 4: 7080.92 0.764 proj of the Nov 21 - Dec 11 - 18 price swing

- RES 3: 7055.73 2.0% Upper Bollinger Band

- RES 2: 7043.00 High Jan 28 and bull trigger

- RES 1: 6922.20/7011.50 50-day EMA / High Feb 11

- PRICE: 6868.00 @ 1455 ET Feb 13

- SUP 1: 6751.50 Low Feb 6 and key short-term support

- SUP 2: 6733.00 Low Nov 25 ‘25

- SUP 3: 6691.56 76.4% retracement of the Nov 21 - Jan 28 bull leg

- SUP 4: 6583.00 Low Nov 21 ‘25 and a key medium-term support

A sharp sell-off yesterday in S&P E-Minis reinstates a potential bearish threat with key resistance at 7043.00 intact, the Jan 28 high and bull trigger. Attention turns to the key support at 6751.50, the Feb 6 low, where a break would highlight a top and a stronger short-term reversal. This would open 6691.56, a Fibonacci retracement point. Initial resistance to watch is at 6922.20, the 50-day EMA.

COMMODITIES: Americas End of Day Oil Summary: Crude Up

WTI Crude prices have reversed earlier declines after Baker Hughes reported a decline in the oil rig count, following losses led by reports that OPEC+ is considering further output hikes from April. The market continues to monitor US-Iran tensions as a second US aircraft carrier heads to the Middle East. US CPI came in slightly lower than expected.

- The US total oil and gas rig count was unchanged on the week at 551 rigs, according to Baker Hughes, with oil down 3 at 409 and down 72 rigs, or 15% on the year.

- OPEC+ is considering resuming oil output hikes from April, Reuters and Bloomberg reported citing OPEC+ sources/delegates. No decision has been made yet ahead of the next OPEC+8 meeting on March 1.

- Following meetings with Israel's President Netanyahu this week, US President Trump suggested that negotiations with Tehran could last as long as a month but cautioned that failure to reach an agreement could be 'very traumatic' for Iran.

- Saudi crude exports to China are set to rise to about 56-57mbbl for contracted oil supplies loading in March, Bloomberg sources said, up from 48mbbl for Feb. Yesterday Reuters reported the allocations for March of 53mbbl.

- WTI Mar futures were up 0.1% at $62.89

- WTI Apr futures were up 0.2% at $62.76

MONDAY-TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 16/02/2026 | 0700/0800 | ** | Unemployment | |

| 16/02/2026 | 1000/1100 | ** | EZ Industrial Production | |

| 16/02/2026 | - | ECB Lagarde and Cipollone at Eurogroup meeting | ||

| 16/02/2026 | 1315/0815 | ** | CMHC Housing Starts | |

| 16/02/2026 | 1325/0825 | Fed's Michelle Bowman | ||

| 16/02/2026 | 1330/0830 | ** | Monthly Survey of Manufacturing | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 17/02/2026 | 0700/0800 | *** | Germany CPI (f) | |

| 17/02/2026 | 0700/0800 | *** | Germany CPI (f) | |

| 17/02/2026 | 0900/1000 | Foreign Trade | ||

| 17/02/2026 | 1000/1100 | *** | ZEW Current Expectations Index | |

| 17/02/2026 | - | ECB de Guindos at ECOFIN Meeting | ||

| 17/02/2026 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/02/2026 | 1330/0830 | ** | Wholesale Trade | |

| 17/02/2026 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 17/02/2026 | 1330/0830 | *** | CPI | |

| 17/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 17/02/2026 | 1500/1000 | ** | NAHB Home Builder Index | |

| 17/02/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 17/02/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 17/02/2026 | 1745/1245 | Fed Governor Michael Barr | ||

| 17/02/2026 | 1800/1300 | ** | US Treasury Auction Result for 52 Week Bill | |

| 17/02/2026 | 1930/1430 | San Francisco Fed's Mary Daly | ||

| 18/02/2026 | - | Reserve Bank of New Zealand Meeting | ||

| 18/02/2026 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 18/02/2026 | 0030/1130 | *** | Quarterly wage price index | |

| 18/02/2026 | 0100/1400 | *** | RBNZ official cash rate decision |