AMERICAS OIL: US OIL: February 13 - Americas End of Day Oil Summary: Crude Up

US OIL: February 13 - Americas End of Day Oil Summary: Crude Slightly Higher

WTI Crude prices have reversed earlier declines after Baker Hughes reported a decline in the oil rig count, following losses led by reports that OPEC+ is considering further output hikes from April. The market continues to monitor US-Iran tensions as a second US aircraft carrier heads to the Middle East. US CPI came in slightly lower than expected.

- The US total oil and gas rig count was unchanged on the week at 551 rigs, according to Baker Hughes, with oil down 3 at 409 and down 72 rigs, or 15% on the year.

- OPEC+ is considering resuming oil output hikes from April, Reuters and Bloomberg reported citing OPEC+ sources/delegates. No decision has been made yet ahead of the next OPEC+8 meeting on March 1.

- Following meetings with Israel's President Netanyahu this week, US President Trump suggested that negotiations with Tehran could last as long as a month but cautioned that failure to reach an agreement could be 'very traumatic' for Iran.

- Saudi crude exports to China are set to rise to about 56-57mbbl for contracted oil supplies loading in March, Bloomberg sources said, up from 48mbbl for Feb. Yesterday Reuters reported the allocations for March of 53mbbl.

- Discounts for seaborne Russian crude cargoes offered to China’s independent refineries have continued to widen amid oversupply, as Indian refiners cut purchases, according to Platts.

- Druzhba pipeline supplies are expected to be restored in the coming days, Slovakia’s Economy Ministry said, according to Reuters.

- The U.S. Treasury will issue more allowances easing sanctions on Venezuelan energy this week, a White House energy official said. Venezuela's PDVSA is in talks with many of its joint-venture partners to offer expansions to oilfields and could help raise oil and gas output.

- Trump: oil coming out of Venezuela, only US able to refine it

- The US has issued a general license to India’s Reliance Industries that will allow the refiner to buy Venezuelan oil directly without violating sanctions, Reuters reports citing two sources.

- Cracks are slightly lower as the market considers future OPEC supply and US-Iran tensions.

- WTI Mar futures were up 0.1% at $62.89

- WTI Apr futures were up 0.2% at $62.76

- RBOB Mar futures were down 0.3% at $1.91

- ULSD Mar futures were down 0.3% at $2.39

- US gasoline crack down 0.3/bbl at 17.37$/bbl

- US ULSD crack down 0.3$/bbl at 37.38/bbl

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDJPY TECHS: Trend Needle Still Points North

- RES 4: 160.21 2.236 proj of the Dec 5 - 9 - 16 price swing

- RES 3: 160.00 3.000 projection of the Sep 17 - 26 - Oct 1 price swing

- RES 2: 159.60 2.000 proj of the Dec 5 - 9 - 16 price swing

- RES 1: 159.45 Cycle High

- PRICE: 158.15 @ 15:59 GMT Jan 14

- SUP 1: 156.90/155.61 20- and 50-day EMA values

- SUP 2: 154.35 Low Dec 5 and a reversal trigger

- SUP 3: 153.62 Low Nov 14

- SUP 4: 152.82 Low Nov 7

USDJPY bulls remain in the driver’s seat, despite the fade off highs. The pair has cleared resistance at 157.89, the Nov 20 high and a bull trigger. This maintains the bullish price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant medium-term uptrend. Sights are on the 160.00 handle next, a Fibonacci projection. Key support to watch lies at 155.61, the 50-day EMA.

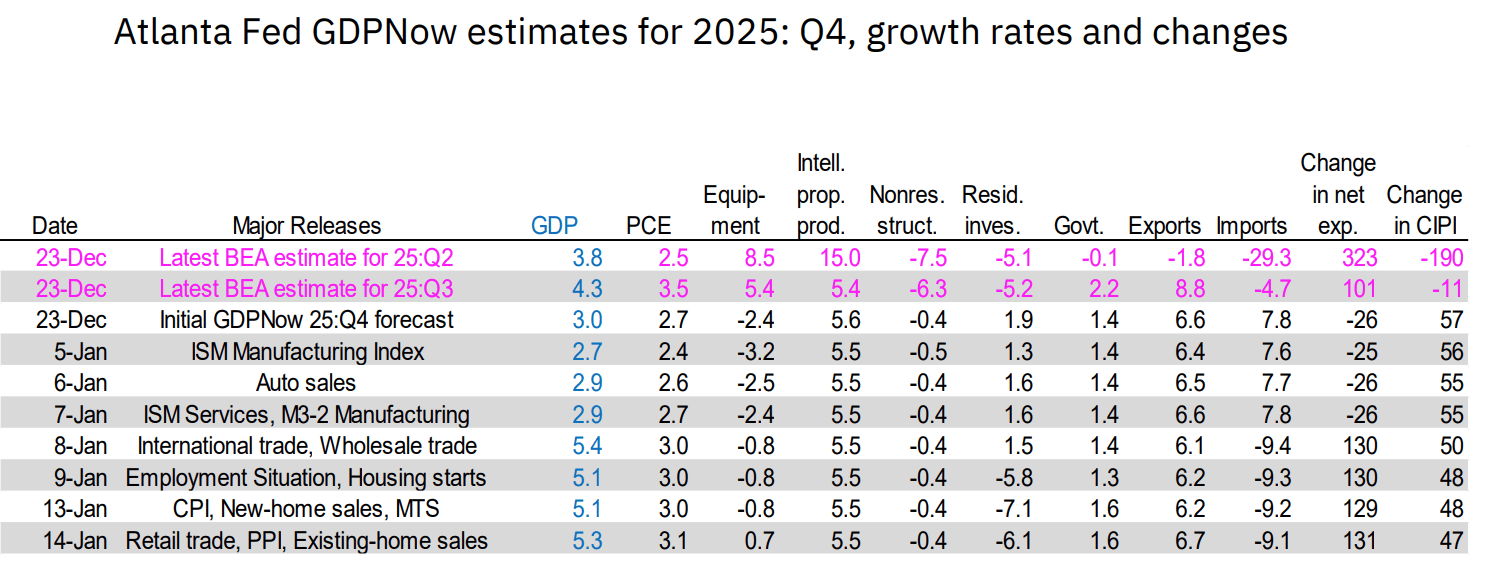

US DATA: Atlanta Fed Q4 GDPNow Edges Up, Underlying Demand Still Softer Than Q3

The Atlanta Fed's latest estimate of Q4 GDP has ticked up to 5.30% Q/Q SAAR vs 5.13% in the prior estimate on January 9.

- The biggest single driver to the upward revision was equipment investment, which following the Manufacturing and Trade Inventories and Sales report is now seen contributing 0.04pp to GDP in the quarter (vs -0.04% in the prior estimate), a +0.08pp contribution shift with the Atlanta Fed showing a positive growth rate in this column for the first time since it initiated the Q4 nowcast on December 23 (equipmant investment posted 5.4% Q/Q SAAR growth in Q3 and 8.5% in Q2 so this would be a slowdown either way).

- The PCE forecast has been upped to 3.1% from 3.0%, reflecting a solid November retail sales release earlier in the day; we had thought the Nowcast could actually edge lower given the downward revision to Control Group sales in October but the Atlanta Fed may have previously underestimated the strength in November; it still expects a slowdown in quarterly PCE growth at a still-high level (3.1% Q/Q SAAR vs 3.5% in Q3).

- Also contributing a little more are net exports (up 0.02pp to 1.99pp) and government spending (up 0.04pp to 0.27pp, following the federal monthly budget statement).

- But those latter two contributions - plus inventories' 0.82pp - mean that private final demand in the quarter is estimated to slow to the mid-2s from the 3.0% in Q3 and 2.9% in Q2, so in this respect underlying economic activity is moderating despite the gawdy headline estimate.

PIPELINE: Corporate Bond Update: $6B JPMorgan 3Pt Launched

$27.15B total corporate bonds to price Wednesday:

- Date $MM Issuer (Priced *, Launch #)

- 01/13 $6B #JPMorgan $2.6B 6NC5 +63, $400M $6NC5 SOFR, $3B 11NC10 +76

- 01/14 $5B *KFW 5Y SOFR+29

- 01/14 $2B #IFC 3Y SOFR+22

- 01/13 $2B *CABEI 3Y +49

- 01/14 $1.5B #OKB 5Y SOFR+34

- 01/14 $1.5B *CDP Fncl 5Y SOFR+42

- 01/14 $1.55B #Bank of NY Mellon $1.25B 4NC3 +47, $300M 4NC3 SOFR+63

- 01/14 $1.5B #ANZ NZ $500M 3Y +45, $500M 3Y SOFR+61, $500M 5Y SOFR+75

- 01/14 $1.5B #Azule Energy $850M 5NC2 8.25%, $650M 7NC3 8.625%

- 01/14 $1B #MassMutual Global $600M 3Y +50, $400M 3Y SOFR+66

- 01/13 $1B #Aviation Capital $400M +3Y+83, $600M 7Y +115

- 01/13 $1B #Jabil $500M 3Y +67, $500M 7Y +97

- 01/14 $1B *AfDB WNG 10Y SOFR+41

- 01/13 $600M #SQM 30.25NC5 5.625%