MNI ASIA MARKETS ANALYSIS: Added China Duties Not Sustainable

HIGHLIGHTS

- Treasuries gapped lower early Friday as Pres Trump commented about unsustainability of tariffs on China: Trump: "No, it's not sustainable, but that's what the number is. It's probably not, it could stand. They forced me to do that."

- Earnings releases really pickup next week, and particular focus may be paid to the earnings report from Zions Bancorp, who release just after the Monday close.

- St Louis Fed’s Musalem (’25 voter, hawk) broadly reiterated recent comments around there being little room to ease monetary policy before it becomes overly loose, with policy somewhere between modestly restrictive and neutral.

- Earnings releases really pickup next week, and particular focus may be paid to the earnings report from Zions Bancorp, who release just after the Monday close.

US TSYS

MNI US TSYS: Risk Sentiment Improved, Pres Trump Opens Door on China Trade

- Treasuries looked to finish lower, holding narrow range after reversing early gains. Tsys gapped lower after President Trump stated additional tariffs on China are "not sustainable, but that's what the number is. It's probably not, it could stand. They forced me to do that."

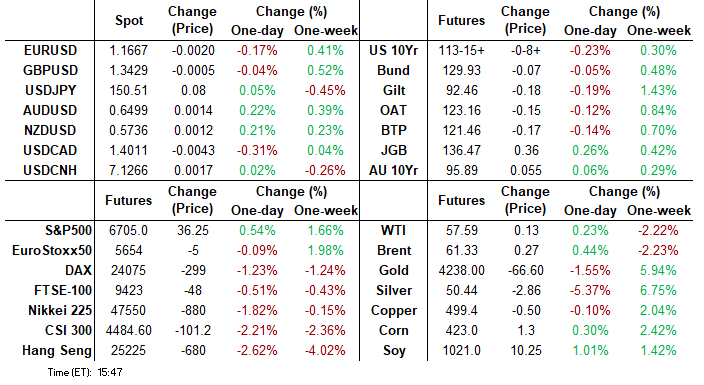

- Currently, the Dec'25 10Y contract trades 113-15 (-9) vs. 113-13 low, 10Y yield back over 4% at 4.005 (+.0304). Firm technical support lies below at 112-30, the 20-day EMA.

- St Louis Fed’s Musalem (’25 voter, hawk) broadly reiterated recent comments around there being little room to ease monetary policy before it becomes overly loose, with policy somewhere between modestly restrictive and neutral. “I could support a path with an additional reduction in the policy rate if there are further risks to the labor market that emerge.”

- Projected rate cut pricing has reversed course on the move, softer vs. late Thursday levels (*): Oct'25 at -25.3bp (-25.8bp), Dec'25 at -50.9bp (-52.4bp), Jan'26 at -64.8bp (-67.3bp), Mar'26 at -77.9bp (-81.6bp).

- Reminder - the Federal Reserve enters policy Blackout after midnight tonight. Slow start to next week: Monday's Leading Index suspended until Federal data is released.

- Corporate earning resume in earnest next week, some highlights: Zions Bancorp that took a hit yesterday reports late Monday, Halliburton, PulteGroup, Lockheed Martin, Northrop Grumman, GM, Netflix, Capital One, Texas Inst, AT&T, Alcoa, American Airlines, Valero, Ford, Intel, General Dynamics, Baker Hughes and Procter & Gamble.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.30% (+0.01), volume: $3.045T

- Broad General Collateral Rate (BGCR): 4.25% (+0.00), volume: $1.180T

- Tri-Party General Collateral Rate (TCR): 4.25% (+0.00), volume: $1.143T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.11% (+0.00), volume: $85B

- Daily Overnight Bank Funding Rate: 4.11% (+0.00), volume: $171B

FED Reverse Repo Operation

RRP usage retreats to $4.102B with 6 counterparties this afternoon from $6,960B Thursday. Compares to $3,516B on Tuesday, Oct 13 (lowest level since early April 2021) & this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Decent SOFR/Treasury option volumes as trade talk saw underlying futures reverse course - chunky call sales after Pres Trump said no when asked if China tariffs will stand - turned two way in the second half. Projected rate cut pricing has reversed course on the move, softer vs. late Thursday levels (*): Oct'25 at -25.3bp (-25.8bp), Dec'25 at -50.9bp (-52.4bp), Jan'26 at -64.8bp (-67.3bp), Mar'26 at -77.9bp (-81.6bp).

SOFR Options:

+10,000 SFRG6 96.68/96.81/96.87/97.00 call condors, 1.75

+11,000 SFRX5 96.75/96.87 call spds, cab ref 96.39

+4,000 SFRX5 96.62/96.75/96.87 call flys, cab

Block, 5,000 SFRZ5 96.25/96.37 2x1 put spds, 1.5 net ref 96.385

-7,500 SFRZ5 96.25/96.37 put spds, 3.5 vs. 96.395/0.24%

-4,000 SFRU5 96.25/96.75 3x1 put spds4.25-4.5

+12,000 SFRH6 96.12/96.18 put spds, 0.5 trg 96.655

+5,000 0QZ5 97.00/97.12/97.25 call flys, 1.75 ref 97.085

Update, 10,000 SFRU5 96.00/96.75 put spds vs. 30,000 96.25/96.50 put spds, 2.5 net package

+12,000 0QZ5 96.75 puts, 3.0 vs. 97.075/0.16%

-22,000 SFRX5 96.87 calls, .75

3,000 SFRX5 96.50/96.56 call spds

Block, 3,000 SFRZ5 96.50/96.62/96.75 call flys, 1.0

3,000 SFRU6 96.00/96.25/97.00/97.25 put condors ref 97.105 to -.095

Block, 4,000 0QX5 96.75 puts, 0.5 vs. 97.11/0.10%

Block/screen, 10,000 SFRM6 96.18/96.31/96.37/96.50 put condors, 1.5

4,000 SFRH6 96.37 puts ref 96.71

9,500 0QZ5 97.00/97.12 call spds ref 97.15

2,000 3QZ5 97.25/97.50 call spds ref 96.83

2,000 SFRX5 96.25/96.31/96.43/96.50 call condors ref 96.425

+5,000 SFRX5 96.62/96.75/96.87 call flys, 0.5 ref 96.43

1,500 SFRH6 96.87/97.00 call spds vs. 96.56/96.62 put spds

+4,000 SFRX5 96.62/96.75 call spds, 1.0 ref 96.43

Block, 5,000 SFRX5 96.12/96.25/96.50 call trees, 7.25

Block/screen, -10,000 SFRH6 96.37/96.50 call spds, 8.25 vs. 96.715

+2,000 SFRZ5 96.43/96.62 call spds, 4.0 ref 96.425

+22,000 SFRU6 96.81/97.12 2x1 put spds, 1-2 ref 97.07

+2,800 SFRX5 96.25/96.37 put spds, 2.75 ref 96.425

Treasury Options:

+15,000 TYX5 114 calls, 10

-10,000 TYZ5 112.5/115 strangles, 36 ref 113-14.5

5,000 TUZ5 103.5/104/104.37broken put flys

1,765 USZ5 114/116 2x1 put spds, 6 ref 118-20

2,000 FVX5 109.5/109.75 put spds ref 110-03.5

2,000 TYX5 113.5/114/114.5/115 call condors ref 113-28.5

-1,500 TYZ5 114 straddles, 136 ref 113-30

+10,000 FVZ5 111.75 calls, 8.5-9 ref 110-04.25 to -04.5

+3,000 FVZ5 110.5 calls, 20.5 ref 110-04

+10,000 TYZ5 112/113 2x1 put spds 6 ref 113-31 ref 113-31

-2,000 wk3 TY 114/114.25 call spds, 4 ref 113-29.5

1,900 TYZ5 115/116 call spds ref 113-26.5

EGBS

The Dec 25 Bund future is down 4 ticks at 129.96, having traded in a range of 129.87-130.59 today.

The 2-Yr yield is unchanged at 1.909%, 5-Yr is up 0.9bps at 2.168%, 10-Yr is up 1bps at 2.58%, and 30-Yr is up 1.6bps at 3.175%.

ITALY

The Dec 25 BTP future is down 17 ticks at 121.46, having traded in a range of 121.41-121.94 today.

The 2-Yr yield is up 2bps at 2.125%, 5-Yr is up 1.8bps at 2.64%, 10-Yr is up 1.9bps at 3.378%, and 30-Yr is up 2bps at 4.31%.

PERIPHERY

Spread of 10-Yr Italian BTPs vs Bunds is up 0.9bps at 79.8bps

Spread of 10-Yr Spanish bonds vs Bunds is is up 0.7bps at 52.7bps

Spread of 10-Yr Portuguese PGBs vs Bunds is is up 0.7bps at 38bps

MNI FOREX: USD Recovers After Soft Start as Trump Sees China Tariffs Not Sustainable

- After a soft start to the session for risk appetite, calming words from the US President helped shore up global equities, put a floor under the USD and aide a recovery for the likes of the AUD and NZD. In an interview with Fox News, Trump stated that 100% tariffs on top of what is in place already is "not sustainable", while adding that "We have to have a fair deal" with China.

- The resulting recovery for equities helped tip futures markets in the US back into positive territory at the close, meaning the e-mini S&P should avoid a formal close below the 50-dma support at 6624.3.

- USDJPY's daily low at 149.38 is holding for now. The bounce off lows for the USD Index seemed to coincide with a bout of sales in EM currencies; most notably

the CNH, ZAR and MXN. In sympathy with JPY gains, CHF stands out: EURCHF's low print of 0.9219 is through the April low, with horizontal support expected layered between 0.9206-22. - Earnings releases really pickup next week, and particular focus may be paid to the earnings report from Zions Bancorp, who release just after the Monday close. The company's stock traded higher Friday after disclosures about loan portfolio losses Thursday - helping stem the downside in US equities ahead of the Friday close.

- Prospects of an end to the US government shutdown next week still appear slim - although it is clear pressure is beginning to build on the White House to reach a resolution: White House econ adviser Hassett noted that if the shutdown proceeds after the weekend, markets can expect Trump to begin ramping up actions toward a resolution.

MNI OPTIONS: Expiries for Oct20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1515(E1.0bln), $1.1540-50(E1.2bln), $1.1640-55(E1.3bln), $1.1710-30(E1.4bln),$1.1790-00(E1.0bln)

- USD/JPY: Y150.00-05($2.0bln), Y150.25($600mln), Y154.80($2.0bln)

- EUR/JPY: Y178.00(E530mln)

- AUD/USD: $0.6670(A$589mln)

- USD/CAD: C$1.4000($718mln)

MNI US STOCKS: Late Equities Roundup: Risk Sentiment Back on Track, Earnings Next Wk

- Stocks are trading near late session highs after losing midday momentum, focus back on trade after President Trump mentioned the unsustainability of increased tariffs on China helped stock indexes bounce off morning lows. Currently, the DJIA trades up 316.73 points (0.69%) at 46,265.01, S&P E-Minis up 38.25 points (0.57%) at 6,706.75, Nasdaq up 128.9 points (0.6%) at 22,690.37.

- Financials, Consumer Staples and Energy continued to lead gainers in lat etrade, the former rebounding after some heavy selling in regional banks yesterday weighed on the Financials sector: American Express +7.17%, Capital One Financial +3.97%, Truist Financial +3.97% and Synchrony Financial +2.51%.

- Consumer Staples buoyed by: Kenvue +8.75%, Estee Lauder +3.71%, Dollar Tree +2.10% and Bunge Global +2.00%; while the Energy sector supported by Expand Energy +2.02%, Halliburton +2.02%, Exxon Mobil +1.63% and Marathon Petroleum +1.53%.

- A mix Information Technology, Utility and Materials/Industrials sector shares underperformed in the first half: Oracle -6.96%, Super Micro Computer -2.64%, Newmont -6.73% (Gold -90 at 4235.0), Vistra Corp -3.50%, Albemarle -2.48%, Cummins -3.35% and United Rentals -2.49%.

- Reminder, corporate earning resume in earnest next week, some highlights: Zions Bancorp that took a hit yesterday reports late Monday, Halliburton, PulteGroup, Lockheed Martin, Northrop Grumman, GM, Netflix, Capital One, Texas Inst, AT&T, Alcoa, American Airlines, Valero, Ford, Intel, General Dynamics, Baker Hughes and Procter & Gamble.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Pullback Appears Corrective For Now

- RES 4: 6850.87 1.618 proj of the Aug 1 - 15 - 20 price swing

- RES 3: 6831.38 2.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6819.25 1.500 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6766.75/6812.25 High Oct 15 / High Sep 9 and bull trigger

- PRICE: 6703.00 @ 1456 ET Oct 17

- SUP 1: 6612.26 50-day EMA

- SUP 2: 6540.25 Low Oct 10 and a key short-term support

- SUP 3: 6506.50 Low Sep 5

- SUP 4: 6427.00 Low Sep 2

Short-term weakness in S&P E-Minis appears corrective - for now. Price has again pierced support at the 50-day EMA, currently at 6612.26. The Oct 10 low of 6540.25 marks the key short-term support. Clearance of this level would undermine a bull theme. Note that moving average studies continue to remain in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Oct 9 high.

COMMODITIES

MNI OIL: US OIL: October 17 - Americas End of Day Oil Summary: Crude Slightly Higher

WTI crude prices steadied after a slight improvement in perceived US-China trade tensions following Trump’s comments that China tariffs would not be sustained at higher levels. Crude remains set for a third successive weekly fall due to market surplus risks amid rising global supply and with US-China trade tensions still high.

- Baker Hughes US rig count 548; oil rigs 418; gas rigs 121. Canada rig count 198; oil rigs 136; gas rigs 61.

- US China trade tensions challenge global growth assumptions, while focus remains on future Russian supply. Trump said China tariffs are unlikely to be sustained at higher levels if 100% tariffs are applied.

- Trump said in a Truth Social post that he had concluded a call with Russian president Putin, saying “great progress was made.” Trump said he would hold a second meeting with Putin “within two weeks or so.”

- India's refiners have suggested that they intend to reduce, but not halt, the purchase of Russian oil. Indian refiners IOC and HPCL have bought Guyanese crude oil from Exxon Mobil in rare purchases from the South American producer, Reuters said.

- WTI Nov futures were up 0.1% at $57.524WTI Dec futures were up 0.2% at $57.11

- RBOB Nov futures were up 1.4% at $1.84

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 20/10/2025 | 0600/0800 | ** | PPI | |

| 20/10/2025 | 0800/1000 | ** | EZ Current Account | |

| 20/10/2025 | 0800/1000 | ECB Schnabel at Macroeconomics and Finance Conference | ||

| 20/10/2025 | 0900/1100 | ** | EZ Construction Output | |

| 20/10/2025 | 0900/1100 | *** | EZ GDP 4th (Final) | |

| 20/10/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 20/10/2025 | 1400/1600 | ECB Schnabel Panel at Macroeconomics and Finance Conference | ||

| 20/10/2025 | 1430/1030 | ** | BOC Business Outlook Survey | |

| 20/10/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 20/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill |