OIL: US OIL: October 17 - Americas End of Day Oil Summary: Crude Slightly Higher

Oct-17 18:33

US OIL: October 17 - Americas End of Day Oil Summary: Crude Slightly Higher

WTI crude prices steadied after a slight improvement in perceived US-China trade tensions following Trump’s comments that China tariffs would not be sustained at higher levels. Crude remains set for a third successive weekly fall due to market surplus risks amid rising global supply and with US-China trade tensions still high.

- Baker Hughes US rig count 548; oil rigs 418; gas rigs 121. Canada rig count 198; oil rigs 136; gas rigs 61.

- US China trade tensions challenge global growth assumptions, while focus remains on future Russian supply. Trump said China tariffs are unlikely to be sustained at higher levels if 100% tariffs are applied.

- Trump said in a Truth Social post that he had concluded a call with Russian president Putin, saying “great progress was made.” Trump said he would hold a second meeting with Putin “within two weeks or so.”

- India's refiners have suggested that they intend to reduce, but not halt, the purchase of Russian oil.

- Indian refiners IOC and HPCL have bought Guyanese crude oil from Exxon Mobil in rare purchases from the South American producer, Reuters said.

- China’s onshore crude inventories fell to 1.17 billion barrels this week from a record high of 1.2 billion barrels in mid-August, due to draws in commercial stockpiles, according to Kayrros.

- Softness in oil demand seen in early October persisted into the second week, with both US and Chinese port activity continuing to weaken, according to JPMorgan.

- Bank of America said that if US-China trade tensions escalate in the midst of an OPEC+ production ramp-up, Brent could drop below $50/bbl, according to a report cited by Rigzone.

- A bearish theme in WTI futures remains intact and the move down this week reinforces the current bearish theme. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. Sights are on $57.50 next, the May 30 low, where a break would open $54.89, the May 5 low. Initial firm resistance is seen at $62.11, the 50-day EMA. Key resistance has been defined at $66.42, the Sep 26 high.

- Patrick DeHaan notes on X that BP’s Whiting facility experienced a fire last night that was extinguished and was actively flaring while alarms were heard in the area.

- Cracks are higher amid signs of disruption at BP’s Whiting refinery. Diesel cracks are nevertheless set for a net weekly decline amid economic fears stemming from heightened US-China trade tensions. Gasoline cracks have been supported this week by signs of limited crude purchasing by the Dangote refinery.

- WTI Nov futures were up 0.1% at $57.524WTI Dec futures were up 0.2% at $57.11

- RBOB Nov futures were up 1.4% at $1.84

- ULSD Nov futures were up 1.2% at $2.18

- US gasoline crack up 1$/bbl at 19.64$/bbl

- US ULSD crack up 1$/bbl at 34.10/bbl

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Dollar Extends Decline Following Fed Cut & Statement Adjustments

Sep-17 18:26

- Statement surprises including downside risks to employment rising and the shift in the balance of risks suitably weigh on the US dollar, bolstering the underlying trend of greenback weakness this week. Price action sees the USD index break the aforementioned cycle lows, which places the DXY at the lowest point since February 2022.

- USDJPY sharply through those 146.21 lows and the bear trigger, to reach a low print of 145.49, significantly narrowing the gap to the next chart point of 145.40 (50% retracement of the Apr - Aug upleg). Should downside momentum continue, support is scant until 142.68, the July 01 low.

- EURUSD has risen to a high of 1.1919 and the immediate focus is on 1.1923, the 2.00 proj of the Feb 28 - Mar 18 - 247 price swing, while GBPUSD briefly surges above 1.37 and outperforms on the session.

- Cycle highs for cable reside at 1.3789, the July 1 and key resistance which could provide a significant level given the upcoming FOMC press conference and tomorrow’s Bank of England MPC meeting.

- AUD and NZD relatively underperform on the session following the sharp two-way swings for major equity benchmarks. AUDUSD did rise to a fresh 11-month high of 0.6707.

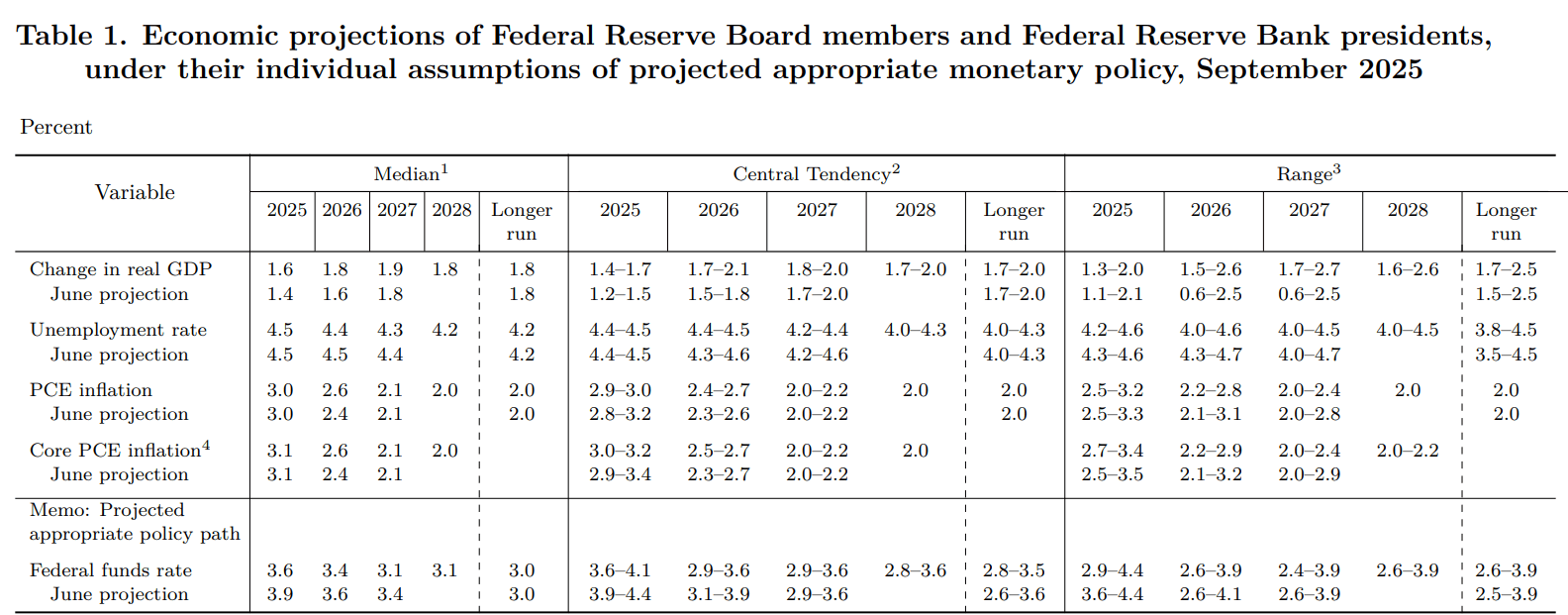

FED: New Econ Forecasts Show Stronger Growth And Inflation, Lower Unemployment

Sep-17 18:24

Looking at the updated macroeconomic forecasts:

- Inflation is seen as a little more stubborn than had been expected in the prior set of projections, with the 2026 medians upped 0.2pp each.

- That pairs with upgrades to growth across the forecast horizon, with the unemployment actually seen as lower than had been previously expected.

- The central tendency of forecasts also shows higher projected growth with lower joblessness and a higher low-end to inflation.

- These are not major changes but we would expect Chair Powell to have to address the seeming incongruence of this with the decision to cut rates at this meeting, as - while they are not central Committee forecasts, per se - the projections appear to suggest that loosening policy restriction leads to stronger growth and higher inflation.

- The longer-run projections were unchanged.

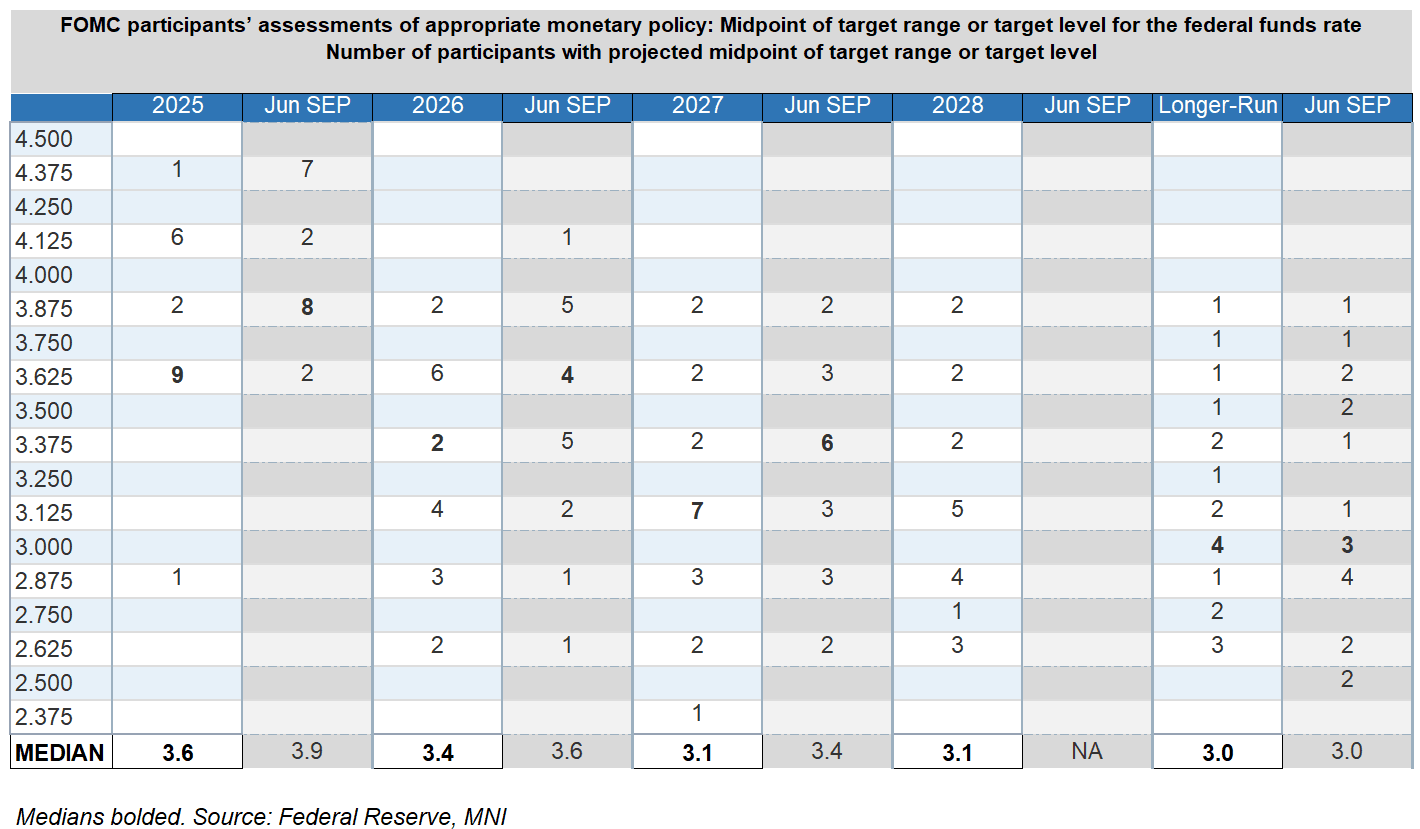

FED: Rate "Dot Plot" Comparison - September vs June

Sep-17 18:18

Below is a comparison of the September FOMC "dot plot" of participants' projections of end-year Fed funds rates, vs the last edition in June:

- The median shifts lower are not really a surprise (3.6% from 3.9% in 2025, 3.4% from 3.6% in 2026, then 3.1% further out and 3.0% longer-run).

- The lowest dot almost certainly belongs to the new Governor Miran who pencilled in a 2.9% dot for end-2025 and presumably sees the lowest in 2027 (2.4%) before coming back up toward neutral in 2028.

- To be sure the 2025 and to a lesser extent 2026 Dot medians were reasonably close calls though with definite shifts lower. There were 9 dots at 3.9% or above for this year and 10 at 3.6% or below, making the latter the 2025 median. We presume that includes the leadership of the Committee including Chair Powell. But interesting that one saw no cuts this year (and it wasn't a voting dissenter) and 6 see this as the last reduction. That's not much changed from the total 9 who saw zero or 1 cuts in the June Dot Plot.

- For 2026 the highest dot has shifted lower by 25bp to 3.9%, but again it's a fairly split median.8 members are at 3.6% or higher (was 10 previously), with 11 at 3.4% or below (vs 9 prior). The mean of the distribution drops lower though with 5 seeing rates at 2.9% or below, vs 2 last time. That's indicative of envisaging more back-loaded cutting.

- As for further out, the 2027-2028 medians are at roughly neutral as expected, 3.1% (2028 was newly introduced in this round of projections).

- There was an interesting shift in the longer-run dots: while the median remains 3.00%, the number above 3.4% has fallen from 6 to 4, while those at 2.50% have shifted up. There are 10 members at 3.00% or below, vs 11 last time - getting a little closer to raising the median. Some of this may be related to the changes in personnel since the June meeting (Philly's Paulson for Harker, Miran for Kugler).