MNI US OPEN - US, China Rare Earth Tensions Rise

EXECUTIVE SUMMARY

- RARE EARTHS TENSIONS RISE AS US AND CHINA TRADE BARBS

- BOJ'S TAMURA SAYS MOVE CLOSER TO 1% NEUTRAL RATE NEEDED

- VOTING UNDERWAY IN FIRST CENSURE MOTION AGAINST SECOND LECORNU GOVERNMENT

- UK MONTHLY GDP IN LINE WITH EXPECTATIONS

- AUD SLIDES AS SEPT JOBS DATA MISSES, AUGUST REVISED LOWER

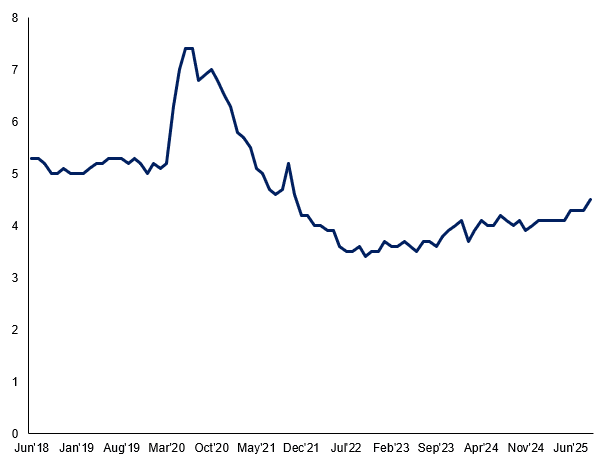

Figure 1: Australia Unemployment Rate Rises to New Post-COVID High

NEWS

US/CHINA (RTRS): Rare Earths Tensions Rise as US and China Trade Barbs

Chinese state media on Thursday issued a seven-point rebuttal to U.S. calls for Beijing to wind back its rare earth controls, as both sides struggle to move beyond a volley of barbs and accusations of blindsiding the other. U.S. Trade Representative Jamieson Greer on Wednesday called China's new rare earth export restrictions "a global supply-chain power grab," and suggested Beijing could stave off President Donald Trump's threat to reimpose triple-digit tariffs on Chinese goods by shelving the measures set to take effect on November 8.

US (WSJ): Trump Hosts Corporate Ballroom Donors at Glitzy White House Dinner

More than three dozen organizations and individuals, including companies with business before the federal government, attended a dinner with President Trump on Wednesday evening after opening their checkbooks to support the new $250 million ballroom under construction at the White House. Companies that sent representatives to the East Room event included Lockheed Martin, Microsoft, Meta Platforms, Alphabet’s Google, Amazon.com and Palantir Technologies, according to the White House.

US/INDIA (BBG): Trump Says Modi Has Committed to Stop Russian Oil Purchases

US President Donald Trump said Indian Prime Minister Narendra Modi vowed to halt purchases of Russian oil, signaling a possible resolution to an issue at the center of the diplomatic and trade rift between Washington and New Delhi. Trump said at the White House that Modi committed to halting Russian oil purchases during a conversation on Wednesday, which was previously undisclosed. In a statement Thursday, India’s government didn’t confirm it’s complying with Trump’s demands, although it said it’s working to deepen energy ties with the US.

US/S.KOREA (BBG): Korea Seeks Argentina-Style Currency Swap With US, Munhwa Says

South Korea is in talks with the US about an Argentina-style currency swap to help mitigate financial stability risks stemming from its planned $350 billion investment commitment under a trade agreement, the Munhwa Ilbo newspaper reported Thursday. Officials are holding detailed negotiations on the scale and method of a potential currency swap, the report said, citing unidentified government officials.

US/S.KOREA (BBG): Bessent Sees Outcome in 10 Days on S. Korea’s Investment: Yonhap

US Treasury Secretary Scott Bessent said South Korea and US can resolve their differences over how to implement Seoul’s $350b investment pledge, adding that he expects “something” to come “in the next 10 days,” according to Yonhap News. Bessent made the remarks during a press meeting, responding to a question from Yonhap. When asked whether the US can provide a currency swap agreement as requested by South Korea, Bessent said the issue isn’t under the purview of his department.

US/JAPAN (BBG): Bessent Says Yen to Settle If BOJ Sticks With Right Policies

US Treasury Secretary Scott Bessent said the yen will settle at an appropriate level if the Bank of Japan continues to conduct the right monetary policy, Japanese media reported, citing a group interview. Bessent declined to comment on the level of Japan’s currency, Kyodo News and Nikkei reported. The yen has declined against the dollar this month at a pace at least twice that of other major currencies, touching an 8-month low of 153.27 to the dollar on Oct. 10. Receding speculation over a near-term BOJ rate hike has been a key factor in that move.

BOJ (MNI): BOJ's Tamura Says Move Closer to 1% Neutral Rate Needed

Bank of Japan board member Naoki Tamura said Thursday that the central bank needs to raise its policy interest rate to around 1%, the lower end of what he sees as the neutral range, as the current 0.5% rate remains well below that level. “I believe that it is important from a risk management perspective for the Bank to move closer to a neutral monetary policy stance,” Tamura told business leaders in Naha City, though he did not specify when a rate increase might occur.

CORPORATE (BBG): TSMC Raises Sales Outlook to Convey Confidence in Global AI Boom

Taiwan Semiconductor Manufacturing Co. hiked its projection for 2025 revenue growth to the mid-30% range, sending a strong signal of confidence in demand for components like Nvidia Corp. chips that power AI. TSMC also raised the lower end of its capital spending target for the year, after reporting a better-than-anticipated 39% jump in profit to NT$452.3 billion ($14.8 billion) in the September quarter. Taiwan’s largest company is now earmarking at least $40 billion for capacity expansion and upgrades in 2025, up from a floor of $38 billion previously.

FRANCE (MNI): Voting Underway in First Censure Motion Against Second Lecornu Government

Voting is underway in the National Assembly in the first censure motion to be brought against the second gov't of PM Sebastien Lecornu. This motion has been put forward by the far-left La France Insoumise (LFI), with the ballot set to close at 11:30CET (05:30ET, 10:30BST) and results announced shortly afterwards. Following Lecornu's general policy speech on 14 Oct, in which he announced the suspension of the 2023 pension reforms and again renounced the use of Art. 49.3 of the Constitution to push through a budget without a parliamentary vote, the leadership of the centre-left Socialist Party (PS) said that it would not instruct its lawmakers to back a censure motion against Lecornu.

ECB (BBG): ECB’s Muller Warns Chinese Export Curbs Could Fuel Inflation

Chinese measures to curb the export of rare earths could reignite price pressures in the euro zone if they ripple through the global economy, according to European Central Bank Governing Council member Madis Muller. With interest rates at an appropriate level, officials should be “patient” and mindful of developments that could pull price pressures in both directions, the head of Estonia’s central bank said in an interview.

UK (MNI): Big UK Fiscal Consolidation Needed to Meet Rules - IFS

UK Chancellor of the Exchequer Rachel Reeves will need to adjust her 2029-30 borrowing outlook by GBP22 billion just to restore the GBP10 billion in headroom she left herself in the spring, the Institute for Fiscal Studies said on Thursday. "When choosing to operate her fiscal rules with such teeny tiny headroom, Ms Reeves would have known that run-of-the-mill forecast changes could easily blow her off course," IFS head Helen Miller said, commenting on a report which used Barclays’ central economic forecast.

UK/CHINA (BBG): China Spied on UK Through Servers Hack for Decade, Officials Say

Chinese hackers accessed classified UK computer systems for more than a decade, people familiar with the matter said, as the British government published documents acknowledging that it considered Beijing’s spying a threat to the economy and local democratic institutions. China routinely accessed low- and medium-level classification information on UK government servers over at least 10 years, according to two former senior security officials and other government officials familiar with the matter.

SWITZERLAND (MNI): Government Revises 2026 GDP Forecast 0.3ppt Lower, 2025 Unchanged

The Swiss government (SECO) forecasts GDP growth of 1.3% in 2025 and 0.9% in 2026. The 2025 is unchanged and 2026 downgraded 0.3ppt from 1.2% compared to those published on June 16. SECO inflation projections continue to be well within the SNB's defined range of price stability. The forecast downward revision is not unexpected following the incorporation of US tariffs, and these forecasts are consistent with an SNB policy rate of 0% for the foreseeable future.

JAPAN (MNI): LDP & Ishin to Continue Coalition Talks on 17th

The governing Liberal Democratic Party (LDP) and libertarian-federalist Japan Innovation Party (Ishin) will hold further talks on 17 Oct after leader-level discussions earlier today failed to reach an agreement on Ishin backing LDP President Sanae Takaichi to be the next PM, or on joining a governing coalition. Earlier today, a meeting of all Isihin lawmakers approved plans to enter coalition talks with the LDP. Ishin co-leader Fumitake Fujita says that at the discussions, Ishin submitted to the LDP 12 talking points that it wants addressed. With no comprehensive agreement reached, Fujita said that he "cannot say whether we are heading into a coalition."

RBA (MNI): RBA Sees Financial Conditions Easing - Kent

The Reserve Bank of Australia sees the cash rate as still slightly restrictive despite evidence of easing financial conditions, Assistant Governor Chris Kent said Thursday. Speaking at an industry forum, Kent said it makes sense to use several methods to assess financial conditions given the uncertainty surrounding each measure.

MIDEAST (BBG): Israel Won’t Compromise on Return of All Bodies of Hostages: PM

Hamas is required to uphold its commitments to the mediators and return all of the fallen hostages for proper burial in Israel, Prime Minister Benjamin Netanyahu’s office says. “We will not compromise on this and will spare no effort until we return all of the fallen hostages, every last one of them.”

DATA

UK DATA (MNI): Monthly GDP in Line With Expectations

- UK AUG GDP +0.1% M/M, +0.3% 3M/3M, +1.5% 3M Y/Y

- UK AUG IND PROD +0.4% M/M, -0.7% Y/Y

- UK AUG MANUF OUTPUT +0.7% M/M, -0.8% Y/Y

- UK AUG SERVICES INDEX +0.0% M/M, +0.4% 3M/3M

- UK AUG TRADE BALANCE GBP -3.39BN

UK GDP rose 0.1% M/M (which was the consensus expectation) but there was a downward revision of 0.1ppt to July to -0.1% M/M from flat. Overall, however, this left the 3m/3m measure in line with expectations at 0.3%. Looking at the component breakdown services was flat (tenth softer than expected) with a downward revision of a tenth to July to be flat M/M too. Manufacturing was stronger than expected rising 0.7% M/M (0.2% M/M expected) with July revised up 0.2ppt to -1.1% M/M.

SWEDEN DATA (MNI): Small Rise in 5-year CPIF Inflation Expectations Won't Concern Riksbank

Swedish long-term money market participant CPIF inflation expectations ticked up to 2.2% in October (vs 2.1% in September). This was the highest since April, but is unlikely to concern the Riksbank nor impact the policy path. At a two-year horizon, CPIF expectations ticked down to 1.9% (vs 2.0% in September).

NORWAY DATA (MNI): Industrial Confidence Indicator Negative Despite "Cautious Optimism"

The Norwegian industrial confidence indicator (which provides signal of output expectations in the forthcoming quarter) slipped to -0.3 in Q3, down from 0.4 in Q2. The indicator remains below the historical average of 2.8. The decline in the composite indicator was driven by capital and intermediate goods producers, offset a little by an increase in output expectations for consumer goods producers. The survey suggests that manufacturing industrial production momentum is unlikely to rebound materially in the fourth quarter, having declined in July and August.

AUSTRALIA DATA (MNI): Aussie Unemployment Climbs to 4.5% in September

- AUSTRALIA SEP UNEMPLOYMENT RATE +4.5%

- AUSTRALIA SEP LABOR PARTICIPATION RATE +67%

- AUSTRALIA SEP EMPLOYED PERSONS CHANGE 14.9K

- AUSTRALIA SEP F-T EMPLOYED PERSONS CHANGE 8.7K

Australia’s unemployment rate rose to 4.5% in September, 20 basis points higher than expected, as the economy added 14,900 jobs, data from the Australian Bureau of Statistics showed Thursday. “This is the highest seasonally adjusted unemployment rate recorded since November 2021,” said Sean Crick, head of labour statistics at the ABS. Full-time employment increased by 9,000, reflecting a 23,000 rise in full-time male employment offset by a 15,000 fall among females.

JAPAN DATA (MNI): Core Machine Orders Below Forecast, Hinting at Softer Capex Y/Y

- JAPAN AUG CORE MACHINE ORDERS -0.9% M/M; JULY -4.6%

Japan Aug core machine orders were below forecast and lost y/y momentum, implying some downside capex momentum risks (which has been a resilient source of Japan's GDP growth). We were -0.9%m/m versus +0.5% forecast, whole July fell 4.6%. This dragged the y/y outcome down to 1.6%, with the market consensus looking for an unchanged 4.9% outcome in Aug.

FOREX: AUDNZD Fades Hard, GBP Outperforms on Better Fiscal Picture

- AUDNZD faded hard today. AUD slipped overnight, pushing prices below the 0.6500 figure following a very poor employment report. Both the employment change headline and unemployment rate were weaker than expected, while the August release was marked lower in the first revision. This put the unemployment rate at a 4 year high, forcing markets to consider an accelerated pace of RBA rate cuts going forward.

- Cementing the theme, local desks note some potential position squaring and profit-taking in AUDNZD which could be putting the mullti-month uptrend at risk. NZDUSD is off highs, but remains higher by ~0.2% in early trade. As such, the price hasn't managed to break above Monday's high at 0.5759.

- As a November RBA cut is becoming more likely, AUDNZD lost 0.4% on the session at 1.1337. AU-NZ 2yr swap rates are not implying further sharp AUDNZD downside - despite the recent run higher in the cross. Monday's Q3 NZ CPI will be the next key input.

- GBP modestly outperforms. UK August activity data was broadly inline and is unlikely to have any real impact on the next BoE decision, however Gilt futures have steadied as markets see marginally less fiscal tightening required at the November Autumn Budget than many envisage, particularly as the Chancellor signalled that taxes on the wealthy will be “part of the story”. EURGBP is lower for a second session, again proving the resilience of the 0.8676 as a key anchor level.

- Tomorrow's negotiations between Japanese LDP and Ishin parties will be the next leg in LDP leader Takaichi's attempt to be elected as the next PM next Tuesday following the failure of leader-level discussions earlier today. Ishin leader Fujita said today they will decide by Monday whether or not to join a coalition, meaning the day could prove decisive for Takaichi's fate, her expansionary agenda, and subsequently, USDJPY trends in the short- to medium term.

- Today was originally set to see the concurrent release of retail sales, PPI and weekly jobless claims from the US, but the extended government shutdown (which the Treasury now estimate is costing the US economy ~$15bln per day) will delay these releases. Instead, alternative measures remain of primary focus - keeping the Philly Fed Business Outlook and New York Fed Services Business Activity data in the spotlight.

- In central bank speak, Fed's Waller, Barr, Miran, Bowman & Kashkari are all due to speak as FOMC members look to set the tone before the pre-meeting media blackout kicks in at tomorrow's close. BoE's Mann & Greene and ECB's Wunsch, Lane and Lagarde all appear at the IMF/World Bank Forum in Washington DC.

EGBS: Bund Rally Takes a Breather, but Tech Outlook Still Bullish

This week’s solid rally in Bund futures has taken a breather this morning, with Spanish/French supply helping contain intraday rallies. Bunds are -12 ticks at 130.02, off opening highs of 130.14. The technical outlook remains bullish though. Initial resistance is yesterday’s high at 130.18, which shields clustered resistance around 130.23 (2.55% 10-year yield level) and 120.27 (June 20 high).

- The German curve has lightly twist steepened, with Schatz yields down ~0.5bps and 30-year Bund yields up 1bp.

- 5/10-year supply from Spain saw solid results (potentially aided by a smaller-than-expected total size), driving some light outperformance for SPGBs versus peers. Meanwhile, MT OAT supply was digested smoothly.

- The 10-year OAT/Bund spread is off earlier highs of ~78.5bps, but French paper still underperforms peers a little (spread to Bunds +0.8bps at ~77.7bps). This should be viewed in the context of politics-inspired tightening earlier this week, with the spread falling by 6bps on Tuesday alone.

- Although PM Lecornu is expected to survive today’s no-confidence motions, fiscal/political risks remain present in France. Budget negotiations start from next week, and sell side desks generally remain cautious on the prospect of further OAT/Bund tightening.

- The Eurozone goods trade surplus was a little wider than expected in August.

- Comments from ECB’s Wunsch and Kocher haven’t added much new. ECB Lane and Lagarde are due this afternoon.

GILTS: Recent Gains Held, Curve Steeper

Gilts have consolidated the bulk of the recent rally, trading little changed vs. Wednesday closing levels.

- Futures -7 at 92.36.

- Initial support and resistance located at 91.60 & 92.51, with the bullish technical cycle intact.

- Yields -1.5bp to +0.5bp, light twist steepening seen on the curve.

- Key support levels in 10- & 30-Year yields (4.496% & 5.309%) remain untouched.

- 10-Year spread vs. Bunds set for the lowest close of the month, last 197bp, ~0.5bp tighter on the day.

- UK headlines point to the need for marginally less fiscal tightening than many envisage, while Chancellor Reeves has signalled that taxes on the wealthy will be “part of the story” when it comes to the Budget.

- Monthly UK GDP data met wider expectations, although the details were a little more mixed. The data had no tangible impact on gilts.

- SONIA futures flat to -1.0.

- BoE-dated OIS pricing ~9bp of easing through year-end.

- BoE’s Mann & Greene are set to speak today, neither expected to vote for a cut at the November meeting.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Nov-25 | 3.949 | -1.9 |

Dec-25 | 3.879 | -8.8 |

Feb-26 | 3.746 | -22.1 |

Mar-26 | 3.698 | -26.9 |

Apr-26 | 3.601 | -36.6 |

Jun-26 | 3.574 | -39.4 |

Jul-26 | 3.518 | -45.0 |

Sep-26 | 3.500 | -46.8 |

EQUITIES: Eurostoxx Trend Remains Up Despite Friday's Sharp Pullback

The trend direction in Eurostoxx 50 futures is up and the latest pullback appears to have been a correction. The contract remains above key support at 5487.08, the 50-day EMA. A clear break of the 50-day average is required to highlight a stronger reversal. On the upside, the bull trigger is 5689.00, the Oct 2 high. Clearance of this hurdle would confirm a resumption of the uptrend. A sharp sell-off in S&P E-Minis on Oct 10 appears corrective - for now. Price has found support below the 50-day EMA, currently at 6609.91, and the Oct 10 low of 6540.25 has been defined as a key short-term support. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend and positive market sentiment. The bull trigger is 6812.25, the Oct 9 high. A breach of this hurdle would confirm a resumption of the uptrend.

- Japan's NIKKEI closed higher by 605.07 pts or +1.27% at 48277.74 and the TOPIX ended 19.78 pts higher or +0.62% at 3203.42.

- Elsewhere, in China the SHANGHAI closed higher by 4.019 pts or +0.1% at 3916.228 and the HANG SENG ended 22.09 pts lower or -0.09% at 25888.51.

- Across Europe, Germany's DAX trades lower by 60.79 pts or -0.25% at 24120.76, FTSE 100 lower by 15.19 pts or -0.16% at 9409.12, CAC 40 up 1.57 pts or +0.02% at 8078.57 and Euro Stoxx 50 down 3.07 pts or -0.05% at 5601.96.

- Dow Jones mini up 78 pts or +0.17% at 46570, S&P 500 mini up 14.5 pts or +0.22% at 6729.5, NASDAQ mini up 97.75 pts or +0.39% at 25022.

Time: 10:00 BST

COMMODITIES: Tuesday's Cycle Low Reinforces Bearish WTI Futures Trend

A bearish theme in WTI futures remains intact and Tuesday’s fresh cycle low reinforces current conditions. The move down last week resulted in a break of support at $60.40, the Oct 2 low. This highlights an extension of the bearish price sequence of lower lows and lower highs and the move down opens $57.50 next, the May 30 low. On the upside, key resistance is at $66.42, the Sep 29 high. First resistance is at $62.30, the 50-day EMA. A bull cycle in Gold remains intact and this week’s extension reinforces current conditions. The move higher maintains the price sequence of higher highs and higher lows. Sights are on the $4300.00 handle next, and $4317.7, a Fibonacci projection point. Note that the trend is in overbought territory. A move down would be considered corrective and would allow the overbought set-up to unwind. Support to watch lies at $3919.6, 20-day EMA.

- WTI Crude up $0.5 or +0.86% at $58.8

- Natural Gas up $0.03 or +1.03% at $3.046

- Gold spot up $24.27 or +0.58% at $4232.18

- Copper down $4 or -0.8% at $497.6

- Silver down $0.14 or -0.26% at $52.8922

- Platinum down $0.46 or -0.03% at $1665.03

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 16/10/2025 | 1200/0800 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 16/10/2025 | 1230/0830 | *** | Retail Sales | |

| 16/10/2025 | 1230/0830 | *** | PPI | |

| 16/10/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 16/10/2025 | 1230/0830 | *** | Retail Sales | |

| 16/10/2025 | 1300/1400 | BOE Mann in Panel on MonPol and Trade Shocks | ||

| 16/10/2025 | 1300/0900 | Fed Governor Christopher Waller | ||

| 16/10/2025 | 1300/0900 | Fed Governor Michael Barr | ||

| 16/10/2025 | 1300/0900 | Fed Governor Stephen Miran | ||

| 16/10/2025 | 1400/1000 | * | Business Inventories | |

| 16/10/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 16/10/2025 | 1400/1000 | * | Business Inventories | |

| 16/10/2025 | 1400/1000 | Fed Governor Michelle Bowman | ||

| 16/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 16/10/2025 | 1445/1545 | BOE Mann in MonPol Panel at IMF/World Bank Meetings | ||

| 16/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 16/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 16/10/2025 | 1545/1745 | ECB Lane in Policy Panel at IIF Annual Meeting | ||

| 16/10/2025 | 1600/1200 | ** | DOE Weekly Crude Oil Stocks | |

| 16/10/2025 | 1600/1200 | ** | US DOE Petroleum Supply | |

| 16/10/2025 | 1600/1800 | ECB Lagarde in IMF Policy Debate | ||

| 16/10/2025 | 1645/1245 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 1730/1330 | BOC Governor Macklem speaks at Peterson Institute event in Washington. | ||

| 16/10/2025 | 1830/1930 | BOE Greene in Panel on UK/EU Relations | ||

| 16/10/2025 | 2015/1615 | Fed Governor Stephen Miran | ||

| 16/10/2025 | 2030/1630 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 2200/1800 | Minneapolis Fed's Neel Kashkari | ||

| 17/10/2025 | 0600/0800 | ** | Unemployment | |

| 17/10/2025 | 0900/1100 | *** | EZ HICP Final | |

| 17/10/2025 | 0935/1035 | BOE Pill Speech at Institute of Chartered Accountants Conference | ||

| 17/10/2025 | 1100/1200 | BOE Greene Roundtable at Atlantic Council | ||

| 17/10/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 17/10/2025 | 1230/0830 | *** | Housing Starts | |

| 17/10/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/10/2025 | 1230/0830 | *** | Housing Starts | |

| 17/10/2025 | 1315/0915 | *** | Industrial Production | |

| 17/10/2025 | 1615/1215 | St. Louis Fed's Alberto Musalem | ||

| 17/10/2025 | 1630/1730 | BOE Breeden in Panel at IMF/World Bank Meetings | ||

| 17/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 17/10/2025 | 2000/1600 | ** | TICS |