MNI ASIA MARKETS ANALYSIS: Volatile Day, Huge Range For Gold

HIGHLIGHTS

- Treasuries looked to finish near late morning highs Thursday, likely driven by risk-off tone in weaker stocks, middle-east tensions and the chances over another US Gov shutdown late Friday.

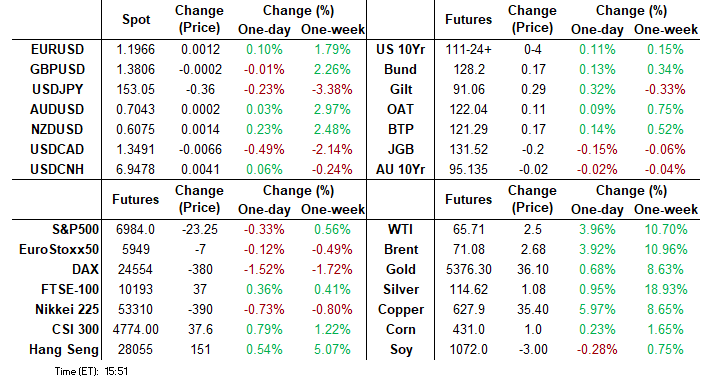

- The ICE dollar index sits very close to unchanged levels on the session Thursday, despite intra-day volatility and some extremely aggressive swings for major equity indices and precious metals.

- Stocks remain weaker late Thursday, off morning lows after carry-over selling in Microsoft (and a handful of software names) led a selloff in the IT sector in the first half.

- Gold has seen a near $500 intra-day range, falling to a low of $5,106, before rebounding later in the session, as the pressure on equity indices stabilised.

US TSYS

MNI US TSYS: Treasuries Bounce as Risk-Off Tone Gathers Momentum

- Treasuries look to finish near session highs Thursday after a relatively volatile first half as a risk-off tone gathered momentum - likely driven by risk-off tone in weaker stocks, middle-east tensions and the chances over another US Gov shutdown late Friday

- Currently, TYH6 trades +6 at 111-26.5 (111-16.5 low / 111-28.5 high), bear threat in Treasuries remains intact as short-term gains are considered corrective. Initial firm resistance to watch is at the 20-day EMA, currently at 112-00. The 50-day EMA is at 112-09+. The area between the 20- and 50-day averages represents a key resistance zone.

- Resumption of weakness would refocus attention on the bear trigger at 111-09, the Jan 10 low. A break of this level resumes the downtrend

- Stocks remain weaker late Thursday, off morning lows after carry-over selling in Microsoft (and a handful of software names) led a selloff in the IT sector. Despite reporting better than expected earnings late Wednesday, Microsoft fell appr 8% on large capital expenditures and weaker Azure & Copilot performance.

- Axios reported the Trump administration is hosting senior defense and intelligence officials from Israel and Saudi Arabia for talks on Iran this week as President Trump considers military strikes.

- A first procedural vote on the six-bill government funding package has been blocked by Democrats in the Senate. The failed vote doesn't necessarily indicate that a bipartisan deal to avert a government shutdown on Saturday has collapsed.

- Look ahead: German and Spanish inflation prints kick off the data calendar on Friday, before Canada GDP, US PPI and the MNI Chicago PMI are all scheduled. China CFLP Manufacturing PMI data late in the evening.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.64% (-0.02), volume: $3.146T

- Broad General Collateral Rate (BGCR): 3.62% (-0.02), volume: $1.313T

- Tri-Party General Collateral Rate (TCR): 3.62% (-0.02), volume: $1.279T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $88B

- Daily Overnight Bank Funding Rate: 3.63% (+0.00), volume: $181B

FED Reverse Repo Operation

RRP usage rises to $2.852B with 4 counterparties this afternoon vs. $1.103B Wednesday. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow reverted to better upside hedging and vol sales late Thursday as underlying futures revisited early session highs (likely driven by risk-off tone in weaker stocks, middle-east tensions and the chances over another US Gov shutdown late Friday). Projected rate cut pricing looks steady to slightly firmer vs. late Thursday levels (*): Mar'26 at -3.5bp, Apr'26 at -7.5bp (-7bp), Jun'26 at -19.7bp (-19.1bp), Jul'26 at -27.5bp (-26.5bp).

SOFR Options:

+7,000 SFRH6 96.68/96.81 call spds, cab

+40,000 0QZ6 97.50 calls, 6.0-7.0 ref 96.67

-20,000 0QN6 96.50 puts, 9.5 vs. 96.71/0.30%

+7,000 SFRM6 96.31/96.37 put spds, 1.25 ref 96.555

1,800 0QH6 97.31 calls ref 96.765

+2,250 SFRJ6 96.37/96.43/96.50 put flys, 1.5 ref 96.54

+5,000 SFRM6 96.62/96.75 call spds, 2.0 ref 96.54

+2,000 SFRH7 95.75/96.00 put spds, 1.5 ref 96.72/0.04%

6,000 SFRM6 96.31/96.37 put spds, 1.25 ref 96.54

+4,000 SFRH6 96.25 puts, cab

2,000 SFRH6 96.37 puts ref 96.37

-1,850 0QH6 96.62/96.75 put spds, 5 ref 96.755

Treasury Options:

+6,000 USH6 117.5 calls, 19 ref 115-06/0.20%

-15,000 TYH6 112 straddles, 56

25,000 FVH6 110.75/111 call spds ref 108-28

10,285 TYH6 110.75/112.75 call over risk reversals, 0.0 ref111-25

5,000 FVK6 108/109.5 strangles

-7,500 TYH6 111 puts, 12-14 last ref 111-20 to -22

-1,000 TYK6 111.5 straddles, 56

+1,500 FVK6 109/109.25/109.5 call trees, .5

+9,500 TYK6 113 calls, 25 vs. 111-23.5/0.22%

2,000 USK6 111 puts, 100 ref 114-04

+8,000 Monday TY 112 calls, 5 vs. 111-27/0.15%

Block, 5,000 TUH6 103.62/104.12/104.25/104.5 put condors. 8 net vs. 104-04.62/0.18%

+1,500 wk1 TY 111/111.75 2x5 call spds, 22

+2,000 FVH6 107.25 puts, 1 ref 108-22.75

MNI BONDS: EGBs-GILTS CASH CLOSE: Bellies Outperform In Risk-Off Trade

EGBs and Gilts enjoyed a solid rally Thursday as part of a broader risk-off move.

- The tone was set by equities tumbling in early afternoon trade, as earnings reports (notably by SAP and Microsoft) elicited concern over the sustainability AI-related stock boom in recent months.

- This pulled Bund and Gilt yields to session lows before bouncing slightly into the cash close alongside a nascent stabilization in equities.

- In data, Eurozone economic sentiment rose to a 36-month high in January. Belgian flash January CPI fell nearly 1pp but there was little reaction (and no consensus), with larger economies reporting inflation in coming days.

- Gains in both the German and UK curves were led by the belly. Periphery/semi-core EGB yields fell but spreads were mixed.

- Friday we get flash January inflation prints for Spain and Germany - our preview is here.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.7bps at 2.083%, 5-Yr is down 2.3bps at 2.418%, 10-Yr is down 1.7bps at 2.84%, and 30-Yr is down 0.5bps at 3.489%.

- UK: The 2-Yr yield is down 2.8bps at 3.714%, 5-Yr is down 4.3bps at 3.946%, 10-Yr is down 3.3bps at 4.511%, and 30-Yr is down 2.6bps at 5.27%.

- Italian BTP spread unchanged at 60.9bps / French OAT up 0.9bps at 58.8bps

MNI EGB OPTIONS: Large Sonia Trades Notable Thursday

Thursday's Europe rates/bond options flow included:

- DUH6 106.90/107.00/107.20c ladder, bought for 2.5 in ~5.3k

- ERU6 97.625p, bought for 1.25 in 20k

- 0RG6 97.87 calls vs. 97.925 10.5K given at 6.25

- SFIG6 96.40/96.35/96.30p ladder, sold at 2.5 in 5k

- SFIH6 96.40/96.35ps 1x2, sold at half and 0.75 in 15k

- SFIK6 96.65/96.75/96.85c fly, bought for half in 2k

- SIFH7 96.65/96.80/96.90c fly 1x1x1, bought for 15.5 in 10k (ref 96.57)

- 0NM6 96.50/96.60/96.70c fly, bought for 1.25 in 5.5k

MNI FOREX: USD Index Roughly Unchanged Amid Broader Cross-Asset Volatility

- The ICE dollar index sits very close to unchanged levels on the session Thursday, despite intra-day volatility and some extremely aggressive swings for major equity indices and precious metals. De-risking on the back of softer Microsoft earnings, geopolitical concerns in the middle east and the high likelihood of another US government shutdown have prompted gold to have a near $500 intra-day range, while Nasdaq futures pulled back around 2.8% from session highs before stabilising.

- The most notable price action in G10 FX has been for the Australian dollar, where AUDUSD had an aggressive turnaround after it reached a fresh cycle high of 0.7094 overnight. The swift reversal for risk during the US session then saw the pair print a low of 0.6969 before recovering to 0.7030 as we approach the APAC crossover. Importantly, a daily close below 0.7041 would bring an end to the impressive streak of winning sessions that saw AUDUSD extend its 2026 advance to around 6.3%.

- Broader de-risking has modestly boosted the Japanese Yen, with USDJPY pulling back below 153.00, although downside momentum has failed to materialise and the most recent lows just above the 152 handle remain unscathed.

- In similar vein, the Swiss Franc remains on the front foot with USDCHF sliding back below 0.77 and EURCHF matching the most recent lows of 0.9158, and the lowest levels since the removal of the peg in 2015. SNB President Schlegel spoke today on the current economic situation and monetary policy, notably there was no mention of the recent CHF strength, with some analysts citing 0.9100 and 0.9000 as levels that will start to ring the alarm bells.

- German and Spanish inflation prints kick off the data calendar on Friday, before Canada GDP, US PPI and the MNI Chicago PMI are all scheduled.

MNI OPTIONS: Expiries for Jan30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1800(E1.7bln), $1.1850(E2.0bln), $1.1900(E5.0bln), $1.1925(E2.1bln), $1.1950(E1.3bln)

- USD/JPY: Y153.00($1.2bln), Y156.00($1.3bln)

- EUR/JPY: Y181.00(E500mln), Y183.00(E520mln)

- GBP/USD: $1.3500(Gbp557mln)

- USD/CAD: C$1.3500($1.7bln)

MNI US STOCKS: Late Equities Roundup: Off Early Lows, Tech Stocks Still Lagging

- Stocks remain weaker late Thursday, off morning lows after carry-over selling in Microsoft (and a handful of software names) led a selloff in the IT sector in the first half. Currently, the DJIA trades down 83.68 points (-0.17%) at 48930.74, S&P E-Mini Futures down 42.25 points (-0.6%) at 6964.75, Nasdaq down 323.8 points (-1.4%) at 23534.6 vs. 23232.78 low.

- Despite reporting better than expected earnings late Wednesday, Microsoft fell appr 8% on large capital expenditures and weaker Azure & Copilot performance. Softening the blow, IBM surged 10% after reporting earnings yesterday - and currently +3.36%. Reminder, Seagate had surged nearly 20% yesterday, helping the third consecutive day of IT sector gains.

- Microsoft is currently -12.10%, followed by ServiceNow -12.3%, Datadog -9.36%, Tyler Technologies -9.30%, Workday-8.62%, Intuit -8.02% and Salesforce -7.35%. Of note, Oracle headlines grabbed some attention earlier: *ORACLE SHARES EXTEND DECLINE FROM SEPTEMBER RECORD TO 50%” Bbg, with the infrastructure software company down 4.12% at the moment.

- On the positive side, a mix of Consumer Discretionary and Communication Services sector shares led advances in the second half: Southwest Airlines +17.79%, Royal Caribbean Cruises +17.04%, Meta Platforms +9.93%, Norwegian Cruise Line +9.91% and Carnival +8.60%.

- Energy sector shares continued to outperform, led by oil & gas stocks with crude climbing higher on middle east tensions (WTI +2.20 at 65.41): Coterra Energy +4.44%, Marathon Petroleum +3.79%, APA Corp +3.58%, Diamondback Energy +3.45%, ConocoPhillips +3.42% and Valero Energy +3.24%.

- Reminder: stocks announcing earnings after the close include: Stryker Corp, Olin Corp, Apple Inc, Sandisk Corp, KLA Corp, Arthur J Gallagher, Weyerhaeuser, Western Digital, Visa Inc, Deckers Outdoor, Colgate-Palmolive, Regeneron Pharmaceuticals, LyondellBasell Ind, Chevron, Church & Dwight, Verizon, Exxon Mobil, American Express and Charter Communication.

MNI EQUITY TECHS: E-MINI S&P: (H6) Bullish Trend Theme

- RES 4: 7141.7 1.236 proj of the Dec 18 - Jan 13 - 21 price swing

- RES 3: 7100.00 Round number resistance

- RES 2: 7080.92 0.764 proj of the Nov 21 - Dec 11 - 18 price swing

- RES 1: 7043.00 High Jan 28

- PRICE: 6970.75 @ 1508 ET Jan 29

- SUP 1: 6955.94 20-day EMA

- SUP 2: 6879.00 Low Jan 26

- SUP 3: 6814.50 Low Jan 21 and the bear trigger

- SUP 4: 6771.50 Low Dec 18 and a key support

The trend structure in S&P E-Minis remains bullish and the pullback between Jan 13 - 21 has been a correction. Yesterday’s gains delivered a print above key short-term resistance at 7036.25, the Jan 13 high and bull trigger. This confirms a resumption of the primary uptrend and paves the way for an extension towards 7080.92, a Fibonacci projection. Key support and the bear trigger has been defined at 6814.50, the Jan 21 low.

MNI COMMODITIES: Precious Metals Pull Back Sharply, Crude Rallies

- Precious metals have come under significant pressure today, amid extremely aggressive swings for major equity indices following softer Microsoft earnings. Gold has seen a near $500 intra-day range, falling to a low of $5,106, before rebounding later in the session, as the pressure on equity indices stabilised.

- Currently, spot gold is down by 1.8% at $5,318/oz, while silver is down by 3.2% at $113.0/oz.

- As noted, positioning dynamics likely exacerbated the pullbacks, with gold and silver entering the session up 25% and over 60%, respectively, YTD.

- From a technical perspective, the primary uptrend in gold remains intact, and today’s pullback has allowed an overbought condition to unwind. Sights are still on $5,654.3, a Fibonacci projection. Firm support is at $4,827.7, the 20-day EMA.

- For silver, trend signals also remain bullish, with sights on $124.585, a Fibonacci projection. Initial firm support to watch at $92.51, the 20-day EMA.

- Elsewhere, copper has also seen significant intra-day volatility, with price surging by over 10% to a fresh record high earlier ($658.3/lb), before pulling back sharply. Currently, copper is up by 4.6% at $620/lb.

- Meanwhile, crude has rallied as the market assesses Iran-related risks amid the potential for US strikes.

- WTI Mar 26 is up 3.5% at $65.4/bbl.

- Today’s rally in WTI futures has resulted in a breach of $64.75, the Sep 26 2025 high and a key resistance. This opens $66.49 next, the Jul 30 2025 high.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 30/01/2026 | 0630/0730 | ** | Consumer Spending | |

| 30/01/2026 | 0630/0730 | *** | GDP (p) | |

| 30/01/2026 | 0700/0800 | ** | Import/Export Prices | |

| 30/01/2026 | 0700/0800 | ** | Retail Sales | |

| 30/01/2026 | 0700/0800 | *** | GDP (p) | |

| 30/01/2026 | 0745/0845 | ** | PPI | |

| 30/01/2026 | 0745/0845 | Flash Payrolls | ||

| 30/01/2026 | 0800/0900 | *** | HICP (p) | |

| 30/01/2026 | 0800/0900 | *** | GDP (p) | |

| 30/01/2026 | 0800/0900 | ** | KOF Economic Barometer | |

| 30/01/2026 | 0855/0955 | ** | Unemployment | |

| 30/01/2026 | 0900/1000 | *** | GDP (p) | |

| 30/01/2026 | 0900/1000 | *** | Baden Wuerttemberg CPI | |

| 30/01/2026 | 0900/1000 | *** | Bavaria CPI | |

| 30/01/2026 | 0900/1000 | *** | North Rhine Westphalia CPI | |

| 30/01/2026 | 0900/1000 | ** | ECB Consumer Expectations Survey | |

| 30/01/2026 | 0930/0930 | ** | BOE Lending to Individuals | |

| 30/01/2026 | 0930/0930 | ** | BOE M4 | |

| 30/01/2026 | 1000/1100 | *** | EZ GDP 1st (Prelim Flash) | |

| 30/01/2026 | 1000/1100 | ** | EZ Unemployment | |

| 30/01/2026 | 1000/1100 | Unemployment | ||

| 30/01/2026 | 1100/1200 | ** | PPI | |

| 30/01/2026 | 1300/1400 | *** | Germany CPI (p) | |

| 30/01/2026 | 1300/1400 | *** | Germany CPI (p) | |

| 30/01/2026 | 1330/0830 | *** | Gross Domestic Product by Industry | |

| 30/01/2026 | 1330/0830 | *** | PPI | |

| 30/01/2026 | 1330/0830 | *** | PPI | |

| 30/01/2026 | 1442/0942 | *** | MNI Chicago PMI | |

| 30/01/2026 | 1600/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 30/01/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 30/01/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 30/01/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 30/01/2026 | 1830/1330 | St. Louis Fed's Alberto Musalem | ||

| 30/01/2026 | 2200/1700 | Fed's Michelle Bowman | ||

| 31/01/2026 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/01/2026 | 0130/0930 | ** | CFLP Non-Manufacturing PMI |