MNI US OPEN - UK GDP Growth Above Expectations in Q2

EXECUTIVE SUMMARY

- PUTIN-TRUMP SUMMIT STARTS 11:30 LOCAL ON FRIDAY, JOINT PRESSER AFTER

- NORGES BANK HOLDS, GUIDES TO FURTHER EASING IN 2025

- CHINA SENDS TOP ENVOY TO INDIA AS TIES WARM AMID US TRADE STRAIN

- UK Q2 GDP STRONGER-THAN-EXPECTED, BUT PRIVATE DETAILS WEAK

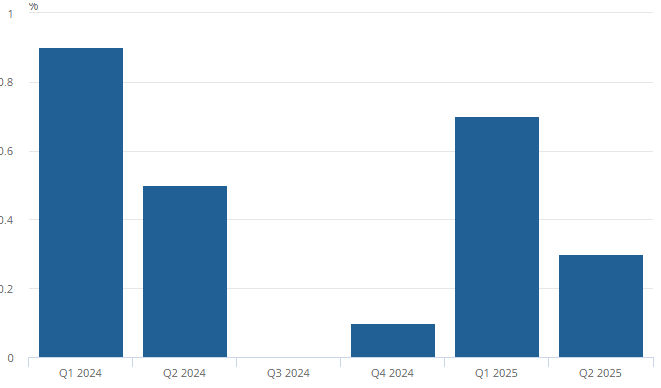

Figure 1: UK economy grew a faster-than-forecast 0.3% in Q2

Source: ONS

NEWS

US/RUSSIA (MNI): Putin-Trump Summit Starts 11:30 Local, Joint Presser After - Kremlin

Senior aide to Russian President Vladimir Putin, Yuri Ushakov, has given details of the upcoming summit between Putin and US President Donald Trump set to take place in Anchorage, Alaska, tomorrow (15 August). Ushakov says that the summit will begin at 11:30 local time (15:30ET, 20:30BST, 21:30CET, 04:30JST). Ushakov says that the two leaders will have a one-on-one meeting with only translators present, as well as a wider meeting with delegations present and a working breakfast. Putin and Trump will hold a joint news conference after the summit. There is no set timeline for how long the talks could last, so presser could take place well into the evening on the east coast/early hours of the morning in Europe.

FED (WSJ): Fed's Daly Says Jumbo Rate Cut Next Month Doesn’t Seem Warranted

San Francisco Fed President Mary Daly pushed back against the need for an interest-rate cut of a half percentage point, or 50 basis points, at the Federal Reserve's September meeting. "Fifty sounds, to me, like we see an urgent-I'm worried it would send off an urgency signal that I don't feel about the strength of the labor market," Daly said in an interview Wednesday. "I just don't see that. I don't see the need to catch up."

NORGES BANK (MNI): Norges Bank Holds, Guides to Further Easing in 2025

Norges Bank left its key policy rate unchanged at.4.25% at its August meeting and stuck to guidance that if the economy evolves broadly as expected it would ease further this year. The decision to leave the policy rate on hold at what was an interim meeting, without fresh forecasts, was widely anticipated, with analysts divided over whether the Norwegian central bank would be more precise about when the next cut was coming. Norges Bank offered no fresh steer on timing, with the June forecast compatible with one or two more 25-basis-point cuts in 2025 and markets pricing in a cut in September.

UK (FT): Initial Tax Data Allays Fears of Non-dom Exodus From UK

Fears of a massive non-dom exodus from the UK have been allayed by initial tax data, which suggests that total numbers leaving the country are in line with — or even below — official forecasts. HM Revenue & Customs payroll data has found no evidence to suggest more non-doms left Britain in response to Rachel Reeves’ 2024 Budget than official predictions, according to people briefed on the findings. The findings will be a relief to the chancellor after a series of surveys — based mainly on anecdotal evidence — suggested her tax policies had prompted huge numbers of wealthy individuals to flee the country.

UKRAINE (MNI): Zelenskyy to Meet w/UK's Starmer After High-Profile Trump Call

President Volodymyr Zelenskyy meets with UK PM Sir Keir Starmer in the aftermath of a series of high-level videocalls on 13 August related to the situation of the war, and more specifically, the upcoming meeting between US President Donald Trump and Russian President Vladimir Putin in Alaska on 15 August. Three main calls took place on 13 Aug: the first between Zelesnkyy and European Union leaders, the second involving Zelensky, European leaders (incl. Starmer), the NATO Secretary General Mark Rutte, and Trump and his VP JD Vance, and the third involving the 'coalition of the willing', those countries that have committed to providing peacekeeping troops to Ukraine if a peace deal is reached.

CHINA/INDIA (BBG): China Sends Top Envoy to India as Ties Warm Amid US Trade Strain

China will send a top official to New Delhi next week, as Beijing steps up efforts to ease long-standing tensions with India amid US President Donald Trump’s global trade overhaul. Chinese Foreign Minister Wang Yi will likely travel to New Delhi on Aug. 18 — his first trip to the country in over three years — and is expected to meet India’s National Security Adviser Ajit Doval and External Affairs Minister Subrahmanyam Jaishankar, according to people familiar with the matter.

CHINA (BBG): China Mulls Asking Firms Run by Central Government to Buy Homes

China is preparing to mobilize companies owned by the central government in Beijing to purchase unsold homes from distressed property developers, following the limited success of a previous initiative that relied on local governments, according to people familiar with the matter. Regulators are planning to ask some of its biggest state-owned enterprises and bad debt managers including China Cinda Asset Management Co. to help clear the housing glut, said the people, asking not to be identified discussing a private matter.

INDIA (BBG): India Wins S&P Rating Upgrade on Economic Growth Momentum

India clinched a higher investment grade rating from S&P Global Ratings, reflecting stronger economic fundamentals and enhancing the country’s appeal to foreign investors. S&P upgraded the country’s rating to BBB, from BBB- with a stable outlook, according to a statement.

TURKEY (BBG): Turkey Keeps Year-End Inflation Forecast Unchanged at 24%

Turkey’s central bank kept its year-end inflation forecast unchanged, maintaining a more optimistic stance than markets and businesses. The monetary authority still expects inflation to slow to 24% by year-end, the same as in its previous quarterly presentation in May, Governor Fatih Karahan said on Thursday. The projections serve as short-term targets for policymakers, whose official longer-term goal is to bring price gains down to 5%. For 2026, the bank’s forecast was raised to 16% from 12%.

DATA

EUROZONE DATA (MNI): Rounded Q2 GDP Unrevised From Flash Release

- EUROZONE FLASH Q2 GDP +0.1% Q/Q, +1.4% Y/Y

Eurozone Q2 GDP was unrevised from the preliminary flash release, rising by 0.1% Q/Q and 1.4% Y/Y (vs 0.6% and 1.5% Q1, respectively). Drivers of the GDP data will only be released with the final print, scheduled for September 5. Employment meanwhile also rose 0.1% Q/Q in Q2 (vs 0.2% Q1), implying flat productivity at least on a per-employee basis. On a yearly comparison, employment rose 0.7% (vs 0.7% Q2).

EUROZONE DATA (MNI): IP Underperforms Already Weak Expectations in June

- EUROZONE JUN IP -1.3% M/M, +0.2% Y/Y

Eurozone industrial production was weaker-than-expected in June, at -1.3% M/M (swda, -1.0% cons), with the downward surprise becoming more significant through a -0.6pp revision in May to 1.1% M/M. Volatile Irish data was, again, a major driver (-11.3% vs +11.9% prior). After the tariff front-loading bolstered Q1, Q2 data overall suggests EZ industry is so far not able to exhibit a more

durable recovery. On an annual basis, production rose just 0.2% Y/Y (cons 1.5%) after a downward revised 3.1% (initially 3.7%) in May, leaving the weakest Y/Y print since January.

UK DATA (MNI): Q2 GDP Stronger-Than-Expected, but Private Details Weak

- UK Q2 PRELIM GDP 0.3% Q/Q, 1.2% Y/Y

- UK JUN GDP +0.4% M/M, +0.3% 3MM, +1.1% 3M Y/Y

- UK JUN IND PROD +0.7% M/M, +0.2% Y/Y

- UK JUN MANUF OUTPUT +0.5% M/M, +0% Y/Y

- UK JUN SERVICES INDEX +0.3% M/M, +0.4% 3MM

Q2 flash GDP at 0.3% Q/Q, above the 0.1% expected by analysts and the BOE. It's a moderation from the 0.7% Q/Q seen in Q1, which was in part skewed higher by "international tariff or domestic tax-related front-loading", according to the BOE. The print was worth just 0.1% of upside in cable, with the BOE more focused on labour market and inflation outturns for its policy outlook. The details of the Q2 reading appear soft though. In particular, private consumption rose just 0.1% Q/Q (vs 0.2% cons and 0.4% prior), while total business investment fell a notable 4.0% Q/Q (vs 0.3% cons, 3.9% prior).

FRANCE JUL HICP +0.3% M/M, +0.9% Y/Y (MNI)

FRANCE JUL CPI +0.2% M/M, +1% Y/Y (MNI)

SWEDEN DATA (MNI): July CPIF Ex-energy Essentially Confirms Flash Estimates, Momentum Falls

- SWEDEN FINAL JUL CPIF +3% Y/Y

- SWEDEN FINAL JUL CPIF EX-ENERGY +3.2% Y/Y

Swedish July CPIF ex-energy essentially confirmed flash estimates, even as the rounded figure printed at 3.2% Y/Y (vs 3.1% flash, 3.3% prior). The unrounded reading was unchanged from the flash at 3.15% Y/Y (vs 3.28% prior). On a seasonally adjusted basis (MNI calculations using the X-13 methodology), CPIF ex-energy prices rose 0.18% M/M, allowing 3m/3m annualised momentum to ease to 2.81% (vs 2.85% prior). Spot inflation rates are probably too high for the Riksbank to cut rates next week (markets and analysts overwhelmingly favour a hold), but declining momentum alongside weak activity trends could prompt the board to guide for a September cut.

CHINA DATA (MNI): China Pork Prices Down 1.4% M/M at Start of August

MNI (Beijing) China's pork prices, an important component in the nation’s CPI measure, fell 1.4% m/m during the first 10 days of August, data from the National Bureau of Statistics showed on Thursday. The data release, which tracks m/m changes in market prices of 50 important means of production in nine categories, showed 18 products increased, 29 fell and three remained unchanged. Notably, the price of LNG and steel rebar fell 2.2% and 1.1%, offset by a gain in coking coal of 3.6%.

AUSTRALIA DATA (MNI): Aussie Unemployment Down 10bp to 4.2%

The unemployment rate fell 10 basis points to 4.2% in July, matching expectations, as the economy added 24,500 jobs, Australian Bureau of Statistics data showed Thursday. Employment growth was driven by a 60,000 increase in full-time roles, partly offset by a 36,000 drop in part-time jobs. Female full-time employment rose by 40,000, while male full-time employment increased by 20,000. The employment-to-population ratio edged up to 64.2%, with the participation rate steady at 67.0%.

FOREX: USD/JPY Ends Consolidation Phase With Break Lower

- USDJPY has turned lower, ending the consolidation phase that dictated play last week. Weakness today puts the price through support drawn off the early August lows as well as 146.71, a key retracement. Price action this week marks a full reversal of the previously overbought condition.

- Meanwhile, speculation around the Trump-Putin meeting in Alaska at the end of the week continues to build - after which TASS have confirmed that Trump and Putin are to hold a joint press briefing. Trump is set to pursue an immediate ceasefire in the conflict - at which point more sincere negotiations and talks can begin over a conclusion to the war.

- Territory remains the key issue, with Kyiv ruling out the handing over of eastern territories, and Putin requiring some concessions as a result of his multi-year special operation. Oil and risk markets remain sensitive to the issue, with Trump warning of "very severe consequences" if no interim agreement is reached. Reports now suggest talks are to start at 1130 local time on Friday, in Joint Base Elmendorf-Richardson, Anchorage, Alaska. That's 2030BST/1530ET. The summit will include one-on-one talks as well as delegation talks between US and Russian ministers, followed by a joint press briefing with both the Russian and US Presidents.

- NOK trades stronger despite the unchanged Norges Bank rate decision - as the Bank's decision to play down the likely downward revision to near-term inflation forecasts in the September MPR and a lack of attention to the rise in LFS unemployment leans slightly hawkish. The August language is certainly not ruling out a September cut, but Norges Bank seem happy to keep their options open in noting that "The policy rate forecast we presented in June indicated one or two additional rate cuts in the course of the year". As a result, EURNOK is narrowing the gap to support at the 20-day EMA (11.8755), clearance of which would expose the 50-day EMA at 11.8080.

- PPI data is the scheduled highlight Thursday, with markets expecting PPI inflation to rise by ~0.2ppts on both the M/M and Y/Y metrics. Weekly jobless claims numbers are also set to cross. Fed speakers include Musalem and Barkin.

EGBS: Bund Futures Tracking USTs Higher; Eurozone Q2 GDP Confirms Flash

Bund futures have followed USTs higher through the morning, currently +17 ticks at 130.00. Bunds have struggled to consolidate above the 50-day EMA during August, which has cancelled any bullish theme that followed the formation of a bullish engulfing candle on Jul 28. Firm resistance is seen at the August 5 high of 130.60.

- US Treasury price action has been supported by more dovish signals from Fed officials in recent days, even as SF Fed President Daly pushed back against the idea of a 50bp September cut in a WSJ interview this morning.

- We note that the recovery in EGBs from Tuesday's low may have also been aided by this week's net supply flows, which are strongly negative.

- German yields are 1-2bps lower, with the curve bull flattening.

- 10-year EGB spreads to Bunds are little changed from yesterday’s close. The BTP/Bund spread remains below the 80bp handle, which has been assisted by a persistent pullback in EUR rates vol since mid-April.

- Details of tomorrow’s Trump-Putin meeting have crossed, but have not been impactful for markets.

- The second estimate of Eurozone Q2 GDP confirmed flash estimates at 0.1% Q/Q, with quarterly employment also growing at that clip. Meanwhile, June industrial production was weaker-than-expected, with May also seeing downward revisions.

- Broader macro focus turns to today’s US data calendar, which includes weekly jobless claims data and July PPI.

GILTS: Early Bull Flattening Holds

The early rally in gilts holds, with cues from wider core global FI markets providing support.

- The breakdown of the Q2 GDP was more worrying than the firmer than expected headline figures, with public spending doing a lot of the heavy lifting, while business investment and private consumption were soft. This may have factored into the rally in gilts as well.

- Elsewhere, June’s monthly economic activity data was firmer than expected.

- Futures have traded through yesterday’s high, topping out at 92.15 so far, but have still not closed Tuesday’s opening gap lower (~92.25).

- Bulls need to close that gap before targeting the August 5 high (92.84). A break there would help negate Tuesday’s bearish close.

- To the downside, initial support comes in at the August 12 low (91.51).

- Yields +1bp to -1bp, curve biased flatter.

- 2s10s and 5s30s remain above nearest round numbers (70bp & 140bp, respectively).

- SONIA futures -2.0 to +0.5, while BoE-dated OIS contracts are little changed to 1bp less dovish vs. closing levels, showing 15bp of easing through December and 26bp of cuts through February.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Sep-25 | 3.970 | +0.3 |

Nov-25 | 3.876 | -9.1 |

Dec-25 | 3.815 | -15.2 |

Feb-26 | 3.705 | -26.2 |

Mar-26 | 3.656 | -31.1 |

Apr-26 | 3.574 | -39.3 |

EQUITIES: E-Mini S&P at New Highs, Targets Retracement Levels Next

The bounce off post-NFP lows in global equity indices persists, with the Eurostoxx 50 future recovering back above the 50-day EMA. Markets look to build a base above this level, through which additional strength refocuses attention on 5486.00, the May 20 high. To the downside, recent impulsive weakness did result in a temporary breach of the bear trigger - this makes the April 30 hi/lo range at 5078-5138 the area of downside interest. Wednesday saw new record highs in the e-mini S&P, clearing resistance through the 6477.31 mark. This cements the underlying uptrend, exposing projection levels into 6523.63 next. Vol-based resistance kicks in at 6521.12. Through recent phases of weakness, the 50-day EMA at 6240.28, has held as support - and will be important on any subsequent declines. Clearance of this average is required to signal a stronger reversal.

- Japan's NIKKEI closed lower by 625.41 pts or -1.45% at 42649.26 and the TOPIX ended 33.96 pts lower or -1.1% at 3057.95.

- Elsewhere, in China the SHANGHAI closed lower by 17.022 pts or -0.46% at 3666.443 and the HANG SENG ended 94.35 pts lower or -0.37% at 25519.32.

- Across Europe, Germany's DAX trades higher by 62.34 pts or +0.26% at 24248.8, FTSE 100 lower by 6.57 pts or -0.07% at 9158.6, CAC 40 up 19.64 pts or +0.25% at 7824.61 and Euro Stoxx 50 up 7.77 pts or +0.14% at 5396.02.

- Dow Jones mini up 2 pts or +0% at 45027, S&P 500 mini down 3.75 pts or -0.06% at 6485.25, NASDAQ mini down 22 pts or -0.09% at 23925.5.

Time: 09:55 BST

COMMODITIES: Gold Off Weekly Lows, But Bounces Appear Shallow

WTI futures traded poorly into the Wednesday close, extending losses on the clearance of the 50-day EMA and bear trigger. Markets have built on this S/T momentum lower, with support breaking at $62.77. The clear break here exposes $58.17, the May 30 low. Gains early last week marked an extension of a corrective cycle - which may now have concluded to result in cleaner positioning. $69.41 marks the 50.0% retracement of the Jun 23-24 downleg - an important level on any recovery from here. Gold prices are off the weekly low, however bounces appear shallow at these levels, keeping price within the mid-point of the recent range. The phase of weakness into the end of July supported the view that short-term pullbacks are corrective - for now - and the bull cycle that started Jun 30 remains intact. However, the yellow metal has traded through support at $3333.9, the 50-day EMA. A clear break of this level continues to signal scope for a deeper retracement and exposes the next key support at $3248.7, the Jun 30 low. Key near-term resistance is $3439.0, the Jul 23 high.

- WTI Crude up $0.29 or +0.46% at $62.94

- Natural Gas down $0.03 or -1.13% at $2.796

- Gold spot down $7.71 or -0.23% at $3346.86

- Copper down $1.1 or -0.24% at $454.8

- Silver down $0.26 or -0.68% at $38.23

- Platinum up $0.45 or +0.03% at $1343.95

Time: 09:55 BST

| Date | GMT/Local | Impact | Country | Event |

| 14/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 14/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 14/08/2025 | 1230/0830 | *** | PPI | |

| 14/08/2025 | 1230/0830 | *** | PPI | |

| 14/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 14/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 14/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 14/08/2025 | 1800/1400 | Richmond Fed's Tom Barkin | ||

| 15/08/2025 | 2350/0850 | *** | GDP | |

| 15/08/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 15/08/2025 | 0200/1000 | *** | Retail Sales | |

| 15/08/2025 | 0200/1000 | *** | Industrial Output | |

| 15/08/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M | |

| 15/08/2025 | 0430/1330 | ** | Industrial Production | |

| 15/08/2025 | 0700/0900 | * | CH Flash GDP | |

| 15/08/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/08/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 15/08/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/08/2025 | 1315/0915 | *** | Industrial Production | |

| 15/08/2025 | 1400/1000 | * | Business Inventories | |

| 15/08/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 15/08/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 15/08/2025 | 1400/1000 | * | Business Inventories | |

| 15/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 15/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 15/08/2025 | 2000/1600 | ** | TICS |