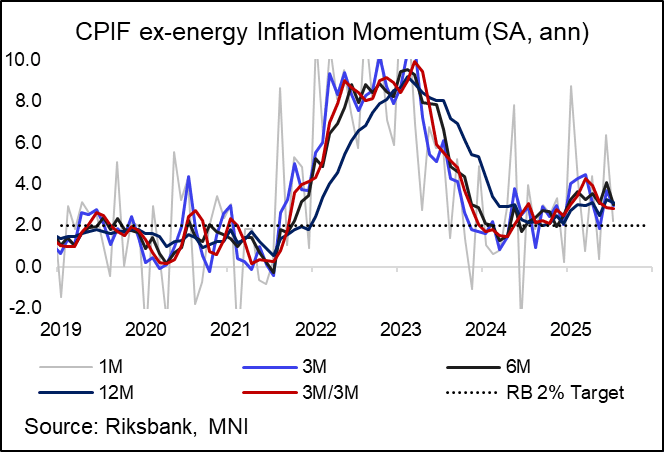

SWEDEN: July CPIF ex-energy Essentially Confirms Flash Estimates, Momentum Falls

Swedish July CPIF ex-energy essentially confirmed flash estimates, even as the rounded figure printed at 3.2% Y/Y (vs 3.1% flash, 3.3% prior). The unrounded reading was unchanged from the flash at 3.15% Y/Y (vs 3.28% prior). On a seasonally adjusted basis (MNI calculations using the X-13 methodology), CPIF ex-energy prices rose 0.18% M/M, allowing 3m/3m annualised momentum to ease to 2.81% (vs 2.85% prior). Spot inflation rates are probably too high for the Riksbank to cut rates next week (markets and analysts overwhelmingly favour a hold), but declining momentum alongside weak activity trends could prompt the board to guide for a September cut.

- Briefly looking at the details of the July print: There was generally a deceleration in services sub-components other than recreation and culture (which was seemingly driven by package holidays). Meanwhile rent inflation also eased a little.

- Core goods inflation also fell, alongside smaller falls in food inflation. Food inflation remains above 4% Y/Y though, and printed above some analyst expectations in July.

- Headline CPIF was confirmed at 2.97% Y/Y (vs 2.84% prior), pushed higher by electricity inflation as expected.

- Swedbank write that “Despite the summer uptick, we remain optimistic about inflation. Firstly, the basket effect, peaking now at 0.7 pp, makes current inflation numbers misleading – in fact, excluding food prices and accounting for the basket effect, annual CPIF was most likely well below 2% in July, and likely also CPIF excl. energy. Secondly, high prices on volatile and seasonal items in June-July usually reverse by August (September the latest). Thirdly, there is little upward pressure on prices from domestic demand and SEK will exert more downward influence on inflation by year-end, even absent any further appreciation”.

- A somewhat more hawkish view comes from Nordea, who note that “There are some technical effects (basket effects) that lift the year-on-year figures over the summer. However, monthly changes have also been somewhat high in recent months, not least for services. It is no dramatic uptick, but inflation is nevertheless too high for a rate cut in the near term. If the Riksbank cut rates, then the SEK could weaken, which in turn could delay the expected downturn in inflation”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB OPTIONS: RXU5 123.50 Puts Lifted

RXU5 123.50 puts paper paid 3 on +4.5K.

STIR: A Little Over 55bp Of Cuts Priced Through Dec Ahead Of UK Risk Events

A relatively flat start for GBP STIRs.

- SONIA futures -1.0 to +1.0.

- Meanwhile, BoE-dated OIS is flat to 1bp less dovish on the day, showing 22bp of cuts for August, 29bp through September, 47bp through November and 56bp through year-end.

- A reminder that a particularly soft REC labour market report and dovish comments from BoE Governor Bailey resulted in dovish repricing on Monday.

- Following those developments J.P.Morgan noted that they “continue to expect a 25bp cut in August, but there are increasing odds of a follow up cut in September which is currently far from fully priced in. Bailey’s comments raise the likelihood of a shift in tone from the BoE in August”.

- They went on to note that “for now the Bank remains cautious due to high inflation, and Bailey’s interview suggests this is partly due to the optics of a headline rate that is expected to continue running close to 3.5% in 2H25. While that is unlikely to change, the BoE will have a limit on its tolerance for weakening data in other areas. Downside surprises in week’s data, for example, would be significant, particularly if they came from the BoE’s core services metric, payroll jobs or private sector average earnings”.

- Bailey & Reeves will speak at Mansion House this evening, while CPI (Wednesday) and labour market (Thursday) data headline this week’s domestic calendar.

- Spillover from today's U.S. CPI data is also eyed.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 4.001 | -21.6 |

Sep-25 | 3.927 | -29.0 |

Nov-25 | 3.748 | -47.0 |

Dec-25 | 3.656 | -56.1 |

Feb-26 | 3.524 | -69.4 |

Mar-26 | 3.489 | -72.8 |

STIR: OIS Still Price One More 25bp Cut This Cycle, July Pause Likely

ECB-dated OIS continue to price one full 25bp cut this cycle, but show virtually no implied probability of a cut at next Thursday’s decision. Yesterday’s Reuters sources piece was consistent with market pricing. Although President Trump’s latest 30% tariff threat was “complicating” Governing Council decision making, it is unlikely to be enough to derail plans for a July pause. OIS assign a ~40% implied probability of a cut in September, which is the next projection meeting and a more appropriate time to assess the tariff outlook.

- A reminder that the ECB’s “severe” trade scenario in the June macroeconomic projections incorporated a 20% US tariff rate on EU exports (alongside EU retaliation) and a 120% levy on Chinese exports.

- Yesterday, Politico reported that the EU is preparing E72bln worth of retaliatory measures against the US, down from the E95bln package proposed in May. The previously agreed E21bln of retaliation has already been postponed till August 6 to allow negotiations with the US to continue.,

- The MNI Policy Team reported yesterday that the EU is considering turning its attention to securing a series of mini-trade deals with the US, including exemptions for cars, pharma and food, which would bypass the 30% tariff threat while talks for a more comprehensive deal continue past the Aug 1 deadline.

- Today’s regional calendar includes the German July ZEW survey and Eurozone May industrial production. Some commentators have noted that there are upside risks to the 1.0% M/M consensus for IP.

- Main global focus remains on the US CPI report at 1330BST.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Jul-25 | 1.920 | -0.3 |

| Sep-25 | 1.816 | -10.7 |

| Oct-25 | 1.784 | -13.9 |

| Dec-25 | 1.693 | -23.0 |

| Feb-26 | 1.680 | -24.3 |

| Mar-26 | 1.654 | -27.0 |

| Apr-26 | 1.662 | -26.2 |

| Jun-26 | 1.667 | -25.6 |

| Source: MNI/Bloomberg Finance L.P. | ||