MNI US OPEN - UK Economy Unexpectedly Contracts in October

EXECUTIVE SUMMARY

- TRUMP SAYS US WOULD HELP WITH UKRAINE’S SECURITY IN PEACE DEAL

- BOJ TO KEEP NEUTRAL, TERMINAL RATE VIEW: MNI EXCLUSIVE

- CHINA PREPARES AS MUCH AS $70 BILLION IN CHIP SECTOR INCENTIVES: BBG

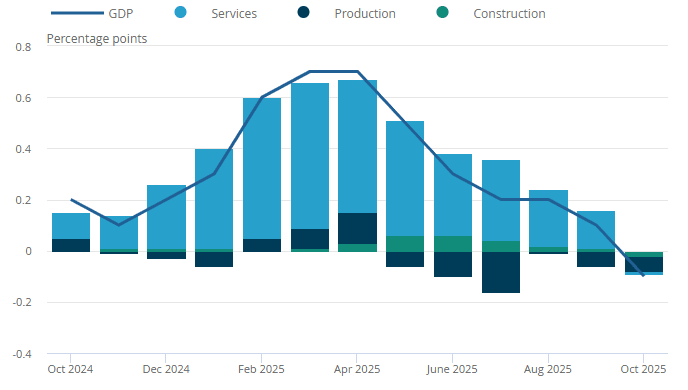

- WEAKNESS IN UK GDP BROAD-BASED BUT JUST UNDER HALF OF THE MISS MAY BE JLR

Figure 1: Contributions to three-month UK GDP growth

Source: ONS

NEWS

US/RUSSIA/UKRAINE (BBG): Trump Says US Would Help With Ukraine’s Security in Peace Deal

President Donald Trump said the US would be willing to contribute assistance to Ukraine as part of a security agreement to end the war with Russia, but continued to express frustration with the pace of talks. “Yeah, we would help,” Trump told reporters Thursday in the Oval Office. “We would help with security, because it’s, I think, a necessary factor in getting it done.” Still, he expressed disappointment that Ukraine President Volodymyr Zelenskiy had not more readily signed off on an American peace plan, adding to pressure on officials in Kyiv who pushed back on an earlier US proposal seen as too accommodating to Moscow.

US (WSJ): Trump Signs Executive Order to Curtail State AI Laws

President Trump signed an executive order Thursday that aims to override state laws on artificial intelligence. The order would allow the Justice Department to punish states with rules deemed restrictive for AI, in a move to bring the U.S. under one federal standard. Silicon Valley executives had been lobbying the president to ban state AI laws that they said could cause the U.S. to lose the AI race to China.

US (MNI): Fed Board Unanimously Reappoints Reserve Chiefs

The Federal Reserve's Board of Governors voted unanimously to reappoint 11 reserve bank presidents to new five year terms beginning next March 1, the central bank said Thursday. By law, all reserve bank presidents and first vice presidents serve five-year terms, with each of the current terms expiring on February 28, 2026, a Fed press statement said. In December 2024, the board of directors of each Reserve Bank, representing a wide range of business and community leaders across each district, started a process to assess their president and first vice president across several performance dimensions.

US/VENEZUELA (NYT): U.S. Issues New Sanctions Targeting Maduro’s Family and the Oil Sector

The United States on Thursday issued new sanctions on Venezuela’s oil sector and on members of President Nicolás Maduro’s family, while taking steps to keep tens of millions of dollars’ worth of oil from a large tanker that U.S. forces seized off the country’s coast. Venezuela’s economy depends on oil and has been hurt by U.S. sanctions, leading Mr. Maduro’s government to smuggle and sell crude through a web of tankers and middlemen. The new sanctions target three nephews of the wife of Mr. Maduro and six shipping companies.

FRANCE (MNI): Senate Set to Review PLFSS, but State Budget Main Challenge for Government

The Senate is set to take up the Social Security Financing Bill for its second reading this morning, following its narrow passage in the National Assembly earlier this week. Le Monde reports that there is the prospect of debate on the PLFSS being shortened via the use of a "...'preliminary question' (or preliminary motion to reject the bill) - which, if passed, would allow the bill to be rejected outright, without being examined article by article. The government could then immediately "ask the National Assembly to make a final decision." LCP reports that the National Assembly is looking to hold its final vote on the bill on Tuesday, 16 December.

BOJ (MNI EXCLUSIVE): BOJ to Keep Neutral, Terminal Rate View

MNI discusses the BOJ's neutral rate stance. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

JAPAN (BBG): Japan’s Auto Union Seeks Higher Wage Gains as BOJ Watches Trends

Japan’s car industry union will seek a slightly more ambitious wage hike goal in the upcoming round of negotiations compared to the previous year, adding momentum to talks as the Bank of Japan tracks pay trends in the US tariffs-hit sector. The Confederation of Japan Automobile Workers’ Union will aim for a minimum ¥12,000 ($77.08) monthly base wage increase, according to a draft plan for negotiations culminating in March released Friday. Under a target that sought a ¥12,000 raise instead of seeking that level as a minimum, the union secured a ¥9,520 increase this year, amounting to a 3.58% gain.

CHINA (BBG): China Prepares as Much as $70 Billion in Chip Sector Incentives

China is considering a package of incentives worth as much as $70 billion to bankroll and support its chipmaking industry, pouring more state money into a sector it deems pivotal to its technological conflict with the US. Officials are deliberating proposals to earmark a package of subsidies and other financing support in the range of 200 billion yuan ($28 billion) to 500 billion yuan, people familiar with the matter said, asking to remain anonymous to discuss private talks. The final details of those incentives, exact amounts and target companies are still getting worked out, the people added.

CHINA (MNI EXCLUSIVE): China’s Steel Futures Face Near-Term Downward Pressure

Chinese advisors share their steel outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com: mailto:sales@marketnews.com

RBA (MNI INTERVIEW): RBA Feb Meeting Live, 4% Rate Over 2026 Eyed

A former senior RBA economist shares his cash rate outlook for 2026. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

THAILAND (BBG): Thai Premier Seizes Chance for Early Vote as Wartime Leader

Thailand’s prime minister is gambling on early elections as a nationalist wave fueled by the border conflict with Cambodia offers his conservative bloc a chance to best pro-democracy rivals that have won every election this century. Anutin Charnvirakul, who’s only been in power for about three months, moved to dissolve parliament on Thursday night to avoid a no-confidence vote, setting the stage for polls in early February. The country’s election commission will announce a date by early next week.

PERU (MNI): BCRP on Hold Again as Expected, Door Still Open to Further Cut

The BCRP left its reference rate unchanged at 4.25% for a third consecutive meeting last night, in line with the majority of analyst expectations. The accompanying policy statement was very similar, with the Board maintaining a data dependent stance and giving no guidance on future decisions. With the real policy rate close to the neutral level, several analysts expect the BCRP to remain on hold ahead, although the door remains open to another cut, given the benign inflation backdrop.

DATA

UK DATA (MNI): Weakness in GDP Broad-Based but Just Under Half of the Miss May Be JLR

- UK OCT GDP -0.1% M/M, -0.1% 3M/3M, +1.1% 3M Y/Y

- UK OCT IND PROD +1.1% M/M, -0.8% Y/Y

- UK OCT SERVICES INDEX -0.3% M/M, +0.0% 3M/3M

- UK OCT CONSTRUCTION OUTPUT -0.3% 3M/3M, +1.1% 3M Y/Y

- UK OCT TRADE BALANCE GBP -4.82BN

The weakness in GDP is rather broad-based but just under half of this miss can be attributed to the continuation of JLR impacts. Overall, this is still a disappointing print though. On the weakness in services this month, the ONS notes that there was a 4.3% M/M fall in "wholesale and retail trade and repair of motor vehicles and motorcycles" as well as "a 1.1% decrease in retail trade in October, except of motor vehicles and motorcycles, following four consecutive monthly growths in this industry." "Computer programming, consultancy and related activities" was also down 3.6% M/M.

UK DATA (MNI): Consumer Inflation Expectations Tick a Little Lower (BOE/Ipsos)

There was a marginal improvement in consumer inflation expectations according to the BOE / Ipsos survey: Inflation expectations over the next 12 months to 3.5% in November from 3.6% in August. The hawks will still likely be holding out for a greater improvement while the doves will likely not have expected a more substantial pullback until spot inflation falls. Overall, we don't think this data has a meaningful impact on either the probability of a cut next week or the prospects for the 2026 Bank Rate outlook. The next print in March will be much more important in our view.

GERMANY DATA (MNI): Little Revisions in German Final CPI

Headline HICP and CPI unrevised. Looking at CPI details on first sight: Services (3.5% vs 3.5% prior), goods (1.1% vs 1.2% prior), energy (main headline upside driver, -0.1% vs -0.9% prior), and food (1.3% prior) all unrevised from the flash readings on a Y/Y basis. As expected after the state-level data, core goods have seen a material slowdown in November in Germany, with clothing and footwear at 0.5% Y/Y (1.2% prior) and furniture and housing equipment at 0.1% Y/Y (0.8% prior). Within the services-heavy

subcategories, also as expected after state-level data, trends were mixed but category for Y/Y in November vs October were within 0.1pp for all categories including health, communication, recreation and culture, education, and hospitality were.

FRANCE DATA (MNI): France HICP Downwardly Revised by 0.04pp

- FRANCE NOV HICP -0.2% M/M, +0.8% Y/Y

- FRANCE NOV CPI -0.2% M/M, +0.9% Y/Y

France November HICP was downwardly revised by 0.04pp in the final reading, to 0.79% Y/Y (vs 0.83% flash, 0.84% October). National CPI (non-HICP) meanwhile was also downwardly revised by 0.04pp, now printing 0.90% Y/Y (0.94% flash, 0.94% October). Remaining with CPI for now for underlying categories, services was the driver behind the downwardly revision, now printing 2.18% Y/Y (2.25% flash). There were no major revisions to the other main special aggregates in the final reading: Energy is -4.60% Y/Y (-4.60% flash), food 1.36% (1.36% flash), and manufactured products -0.60% Y/Y (-0.61% flash).

SPAIN DATA (MNI): HICP Up Marginally From Flash, Supports Upward Trend

- SPAIN NOV HICP +0.0% M/M, +3.2% Y/Y

Spain HICP ticked up marginally from flash to 3.16% Y/Y (rounding to 3.2%, flash rounded to 3.1%). It was broadly unchanged from October (3.18% 2dp Oct), while the monthly rate was unrevised from flash at 0.0% M/M (vs 0.5% Oct). This continues the gradual upward trend since May. Broad COICOP categories mostly remained unchanged from flash and October, but the largest moves were in Housing, water, electricity, gas and fuels at 5.6% Y/Y (vs 7.5% Oct) - the fall driven mostly by energy - and Clothing and footwear 0.5% (vs -0.4% Oct).

SWEDEN DATA (MNI): LFS Unemployment Rate Should Cement "Steady Rates" Guidance Next Week

- SWEDEN NOV UNEMPLOYMENT SA 9.1% (FCST 8.8%)

- SWEDEN NOV UNEMPLOYMENT NSA 8.2%

Smaller fall in the seasonally adjusted unemployment rate than had been expected in November (9.1% vs 8.8% cons, 9.3% prior). Analyst forecasts submitted to Bloomberg ranged from 8.7-9.0%. Big picture, there are signs that the labour market is starting to recover (e.g. in Public Employment Service and survey data), but a stubbornly high LFS unemployment rate should mean the Riksbank continues to guide for steady rates as the base case next week. Any tacit endorsement of market pricing for a hike by the end of next year could be included in the updated rate path projection.

CHINA DATA (MNI): China November M2 Slows to Half-year Low

- CHINA END-NOV M2 +8.0% Y/Y VS MEDIAN +8.2%; END-OCT +8.2% Y/Y

- CHINA END-NOV M1 +4.9% Y/Y VS +6.2% Y/Y END-OCT

- CHINA JAN-NOV NEW LOANS CNY15.36 TRLN VS MEDIAN CNY15.39 TRLN

MNI (Beijing) China's M2 money supply grew by 8.0% y/y in November, marking the lowest reading since May, missing market forecasts of 8.2% growth and slowing from October's 8.2% gain, data released on Friday by the People's Bank of China showed. New yuan loans increased for the second month by CNY390 billion in November, rising from October's CNY220 billion. Total social financing rose by CNY2.49 trillion, rising from CNY810 billion in October. While M1 rose by 4.9% y/y, decelerating from October's 6.2% growth. M0 grow by 10.6% y/y, flat from the previous reading.

NEW ZEALAND DATA (MNI): PMI Edges Up, Employment Index Bounces, New Orders Ease

New Zealand's BusinessNZ manufacturing PMI edged up to 51.4 in Nov, from a revised 51.2 outcome in Oct. This leaves us off recent cycle highs (53.6) in Feb of this year. Post Covid highs in the index were in the 60-65 region, so whilst the index remains in expansion, the pace of recovery looks to be fairly modest. In terms of the detail, it was mixed. Encouragingly, the employment sub index rose to 52.4 from 48.3 in Oct. This is the highest read since April of this year. New orders moderated though to 51.9, from 54.5 in Oct. Production edged up to 52.8 from 52.0 prior.

RATINGS: Stable Outlooks Set for Review After Close

Potential rating reviews of note scheduled for after hours on Friday include:

- Fitch on the European Financial Stability Facility (EFSF) (current rating: A+), the European Stability Mechanism (ESM) (current rating: AAA; Outlook Stable) & Norway (current rating: AAA; Outlook Stable).

- Moody’s on Finland (current rating: Aa1; Outlook Stable) & Slovakia (current rating: A3; outlook stable)

FOREX: DXY Consolidating Recent Weakness, USDCAD Extends Bearish Theme

- Having held resistance well across November, the USD Index’s pull lower has gathered downside momentum this week, assisted by a not so hawkish cut from the Fed and the associated constructive risk backdrop. This prompted the DXY to extend its three-week pullback to ~2.25% yesterday, with the DXY currently consolidating a 0.6% decline this week.

- CAD is an outperformer on Friday, extending the recent bull theme as the global FI hawkish repricing was particularly substantial for Canada. Expectations for BoC hikes through next year stand firm by now following stronger labour market data and a hawkish BoC meeting this week.

- This keeps the bear theme in USDCAD firmly intact as spot narrows the gap to 1.3727, the September 17 low. Short-term gains would be considered corrective and would allow an oversold condition to unwind, with initial firm resistance to watch is 1.3936, the 20-day EMA.

- Following yesterday's SNB decision, CHF this morning holds most gains seen over the past couple of sessions against a wide set of G10. USDCHF remains a key detriment of dollar weakness post FOMC. The pair narrowed in on clustered horizontal support into the 0.7829-78 area - marking the series of lows printed across Q3/Q4 this year.

- GBP has seen moderate pressure following the below-expectation October GDP figures. This led EURGBP to a 0.8775 overnight high, with recent gains signalling a possible reversal and the end of the corrective phase. Initial firm resistance to watch is unchanged at 0.8802, the Dec 2 high, while key short-term support has been defined at 0.8721, the Dec 9 low.

- The data calendar remains light for the rest of the day, with only Canada housing data being scheduled. Fedspeak is set to pick up, with Paulson, Hammack and Goolsbee appearing today. Goolsbee may be of particular focus as he was a hawkish dissenter in the FOMC earlier this week.

EGBS: German Curve Unwinding Recent Bear Flattening, Several Risks Next Week

The German curve continues to gradually unwind recent bear flattening, with 5s30s 1bp steeper at 99.5bps. Next week’s regional calendar is heavy. The front-end is likely to be influenced by December flash PMIs and the ECB decision, while the belly/long-end will be looking for cues from 2026 sovereign issuance plans - especially from Germany.

- German yields are +0.5 to +2bps higher across the curve, with market moving headline flow relatively sparse this morning.

- Bund futures are -12 ticks at 127.46. Although off Wednesday’s 127.05 low, technical conditions in Bund remain bearish. Initial resistance is the Dec 8 high at 128.08.

- 10-year EGB spreads to Bunds are biased up to 1bp narrower, aided by an extension higher in European equity futures. The 10-year BTP/Bund spread is consolidating back below the 70bp figure. Given the extent of narrowing since 2022, the bar to further tightening next year has likely been raised. However, the combination of improving Italian fiscal fundamentals and domestic political stability continues to increase the attractiveness of BTPs for domestic and foreign investors.

- Final November HICP inflation readings from Germany, France and Spain did not bring many surprises. The upward revision in Spain was due to rounding (3.16% Y/Y vs 3.1% flash).

Figure 2: German 5s30s Curve

Source: Bloomberg Finance L.P.

GILTS: Curve Twist Steepens After Soft GDP

Gilts are back from early highs.

- Softer-than-expected UK GDP data provided the initial rally.

- Twist steepening of the curve promoted by the data driving dovish BoE repricing, while also calling into question the optimistic economic growth forecasts that accompanied the Budget. Slower GDP growth would erode some of the government’s envisaged fiscal headroom if the trend was to persist.

- A hold of resistance at yesterday’s high in futures and an uptick in European equities also provided some pressure.

- Yields now 2bp lower to 2bp higher, with 2s10s and 5s30s extending bounces from post-Budget lows.

- Futures -17 at 91.31.

- Recovery from Monday’s lows has eased the bearish threat, initial resistance located at 91.64. an extension of the early morning rally would switch focus to the November 27 high (91.93).

- Meanwhile, bears need to break a support cluster (90.62 & 90.53) to regain momentum.

- GBP STIRs edge away from dovish session extremes as the long end falters.

- BoE-dated OIS little changed to 2.5bp more dovish across liquid contracts. 22bp of easing priced for next week’s decision, 60bp of easing priced through ’26.

- SONIA futures flat to +3.0.

- Terminal rate pricing trades back below 3.40% after threatening to test 3.50% earlier in the week. A reminder that doves failed to force a meaningful break below 3.30% in recent weeks.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.756 | -21.8 |

Feb-26 | 3.687 | -28.7 |

Mar-26 | 3.607 | -36.7 |

Apr-26 | 3.502 | -47.2 |

Jun-26 | 3.458 | -51.7 |

Jul-26 | 3.399 | -57.5 |

Sep-26 | 3.386 | -58.8 |

Nov-26 | 3.369 | -60.6 |

Dec-26 | 3.377 | -59.7 |

Feb-27 | 3.380 | -59.4 |

EQUITIES: Thursday's Gains Strengthen a Bull Theme for Eurostoxx Futures

A bull cycle in Eurostoxx 50 futures remains intact and Thursday's gains strengthen a bull theme. Price is trading above the 20- and 50-day EMAs, and has cleared 5742.40, 76.4% of the Nov 13 - 21 bear leg. The breach of this price point paves the way for an extension towards 5825.00, the Nov 13 high and the bull trigger. First key support to watch lies at 5637.69, the 50-day EMA. A bull cycle in S&P E-Minis remains intact and a fresh short-term cycle high yesterday strengthens the bull theme. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. Sights are on the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support to watch is at 6823.86, the 20-day EMA.

- Japan's NIKKEI closed higher by 687.73 pts or +1.37% at 50836.55 and the TOPIX ended 66.59 pts higher or +1.98% at 3423.83.

- Elsewhere, in China the SHANGHAI closed higher by 16.028 pts or +0.41% at 3889.346 and the HANG SENG ended 446.28 pts higher or +1.75% at 25976.79.

- Across Europe, Germany's DAX trades higher by 129.74 pts or +0.53% at 24425.46, FTSE 100 higher by 30.87 pts or +0.32% at 9734.15, CAC 40 up 56.21 pts or +0.7% at 8140.49 and Euro Stoxx 50 up 31.77 pts or +0.55% at 5784.94.

- Dow Jones mini up 87 pts or +0.18% at 48834, S&P 500 mini down 13 pts or -0.19% at 6894.25, NASDAQ mini down 139.5 pts or -0.54% at 25574.5.

Time: 10:00 GMT

COMMODITIES: Gold Narrows Gap to Key Resistance and Bull Trigger at $4381.50

A bearish theme in WTI futures remains intact and the move down this week reinforces this theme. Note that moving average studies are in a bear-mode position, highlighting a dominant medium-term downtrend. A stronger resumption of the bear leg would open key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. Gold traded higher yesterday, reinforcing a bullish theme. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch is the 50-day EMA, at $4060.3. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

- WTI Crude up $0.09 or +0.16% at $57.65

- Natural Gas down $0.05 or -1.25% at $4.178

- Gold spot up $37.83 or +0.88% at $4318.39

- Copper down $3.3 or -0.6% at $546.5

- Silver up $0.54 or +0.85% at $64.111

- Platinum up $19.48 or +1.15% at $1718.81

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 12/12/2025 | 1300/0800 | Philly Fed's Anna Paulson | ||

| 12/12/2025 | - | ECB de Guindos at ECOFIN Meeting | ||

| 12/12/2025 | 1330/0830 | * | Building Permits | |

| 12/12/2025 | 1330/0830 | ** | Wholesale Trade | |

| 12/12/2025 | 1330/0830 | Cleveland Fed's Beth Hammack | ||

| 12/12/2025 | 1535/1035 | Chicago Fed's Austan Goolsbee | ||

| 12/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 15/12/2025 | 2350/0850 | *** | Tankan |