UK DATA: Consumer inflation expectations tick a little lower (BOE/Ipsos)

There was a marginal improvement in consumer inflation expectations according to the BOE / Ipsos survey. The hawks will still likely be holding out for a greater improvement while the doves will likely not have expected a more substantial pullback until spot inflation falls. Overall, we don't think this data has a meaningful impact on either the probability of a cut next week or the prospects for the 2026 Bank Rate outlook. The next print in March will be much more important in our view.

- Inflation expectations over the next 12 months fell marginally to 3.5% in November from 3.6% in August. However, looking at the unrounded numbers, the fall from 3.56% to 3.53% was much smaller. This is still the second highest reading since the beginning of 2024.

- The 12-months after also fell a tenth when rounded to 3.3% from 3.4%.

- The 5-year measures (longer term) fell to 3.7% from 3.8%, but at 3.749% it couldn't have been closer to rounding up to remain at 3.8%. After the August reading, the November reading was the next highest print since May 2019.

- The survey was conducted between 7 and 10 November 2025, so well in advance of the Budget.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

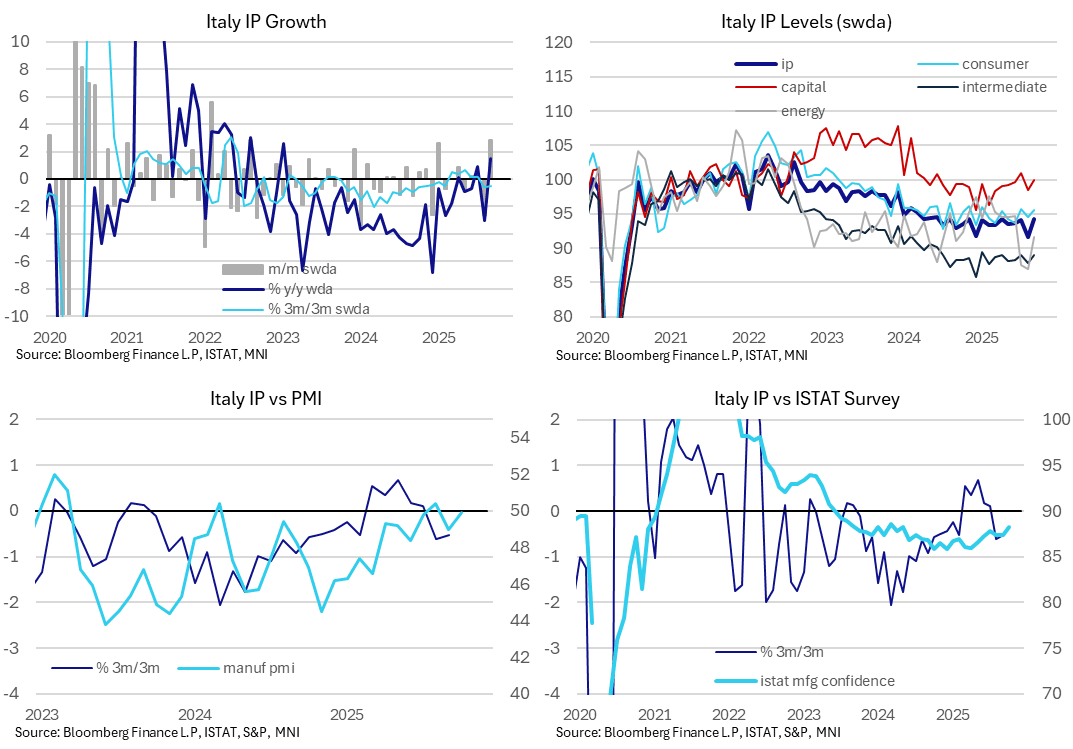

ITALY DATA: Underlying IP Momentum Sluggish, But Surveys Suggest Improvements

Italian industrial production rebounded in September, rising 2.8% M/M, well above the 1.5% consensus. August’s already weak reading was revised down to -2.7% (vs -2.4% initial). Stripping out the monthly volatility, which may be a function of seasonal factors, IP momentum remains sluggish. That said, sentiment data points towards a gradual recovery in the months ahead.

- On a 3m/3m SWDA basis, production was down 0.5% in September, after a 0.6% fall in August.

- The manufacturing PMI was essentially neutral in October, printing at 49.9 after 49.0 in September and 50.4 in August. Meanwhile, ISTAT’s manufacturing confidence series rose to a 17-month high of 88.3 in October.

- On a single-month basis, the manufacturing component of IP (which has a weight of around 90%) rose 1.4% M/M (vs -1.9% prior), with mining and quarrying (12.0% M/M) and electricity, gas, steam and air conditioning supply (8.3% M/M) seeing much larger sequential changes.

- Within manufacturing, rebounds were seen in all major categories other than textiles (-4.4% M/M vs 3.6% prior).

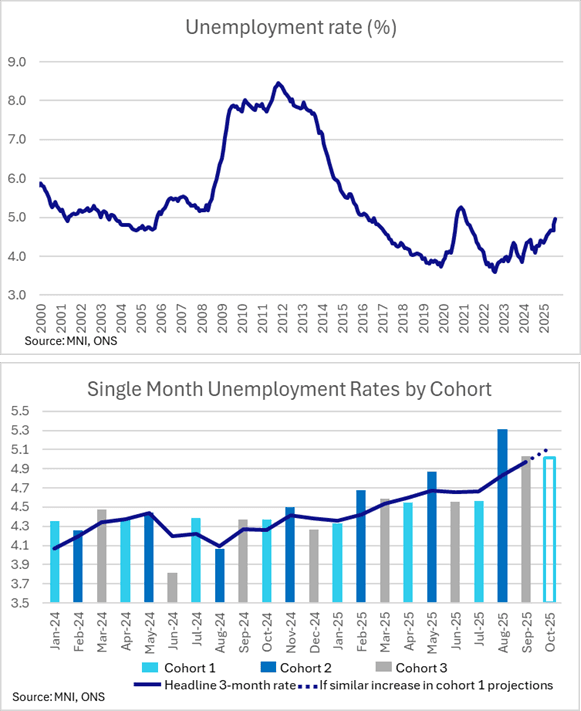

UK DATA: Unemployment on course to reach November MPR peak rate ahead of Dec MPC

- Just like AWE data, unemployment data is produced using the 3-month average of three single month prints – and each of these three months has a different cohort.

- For some time now the cohort seen in November 2024, February, May and August has consistently seen higher single month prints than the other two cohorts (which have seen broadly similar readings to each other).

- There was a significant 0.44ppt increase in the single month unemployment rate seen in the print released last month from 4.87% in May to 5.31% in August which led to the headline 3-month rate increasing from 4.66% to 4.83%.

- Expectations had been that the September single month print would see a smaller jump relative to June. As it turns out, however, a marginally larger 0.47ppt change was seen in this cohort’s single month print from 4.56% in June to 5.03% in September. This left the headline 3-month rate at 4.97% (around a tenth above consensus).

- To put this into context, the 4.97% print today is the Bank of England’s Q4 forecast and it has been reached a quarter earlier than expected (making last week’s MPR projections already look a bit stale).

- If we assume that we see a similar increase in the single month rate between July and October we would be left with a headline 3-month unemployment rate marginally above 5.1%. Indeed, to round up to a 5.1% print the next cohort only needs to see a 0.25ppt increase between October and July - so almost 2 tenths lower than seen in the other two cohorts.

- The latest MPR projections only see a 5.1% print reached by Q2-26 before falling back to 5.0% or lower through the rest of the forecast. This does therefore seem to be meaningful downside news.

- Note that if we do see this 5.1% print in the October data, the MPC would see this print on the Monday morning ahead of their December policy decision. Obviously we still have inflation data to come, but it does appear that the labour market data is doing its job to convince Governor Bailey that the soft print seen ahead of the November MPC meeting was not a one-off.

GILT SYNDICATION: 1.75% Sep-38 linker: Guidance unchanged

- Size: GBP Benchmark (MNI expects GBP GBP4.5-5.5bln)

- Books in excess of GBP55bln (inc JLM interest of GBP3.9bln)

- Guidance unchanged : 1.125% Nov-37 linker (GB00B1L6W962) +10.50 / +10.75bps

- ISIN: GB00BMY62Z61

- Expected Settlement Date: 13-November-2025 (T+1)

- JLMs: GSIB (B&D/DM) / JPM / NOMURA / SANTANDER

- Timing: Books open, today’s business (MNI expects books to close at 10:00GMT)

Source: Market source and MNI colour