MNI US OPEN - Trump to Set Unilateral Tariffs in Two Weeks

EXECUTIVE SUMMARY

- TRUMP SAYS AGAIN HE’LL SET UNILATERAL TARIFFS IN TWO WEEKS

- JAPAN AND US STILL FAR APART IN TARIFF TALKS, PM CITED AS SAYING

- ISRAEL APPEARS READY TO ATTACK IRAN, OFFICIALS IN U.S. AND EUROPE SAY

- UK MONTHLY GDP, TRADE DISAPPOINT BUT LABOUR DATA MORE IMPORTANT FOR MPC

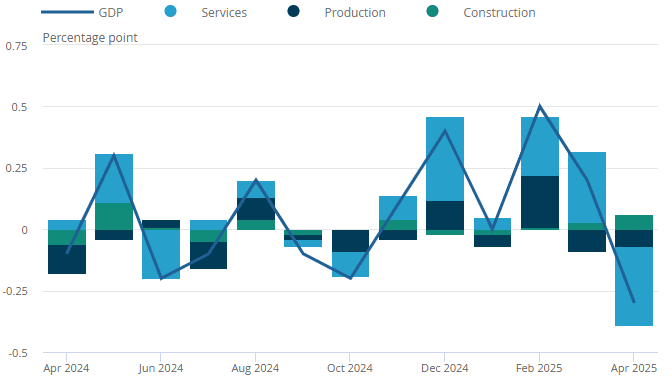

Figure 1: Services sector main contributor to 0.3% fall in UK GDP in April

Source: ONS

NEWS

US (BBG): Trump Says Again He’ll Set Unilateral Tariffs in Two Weeks

President Donald Trump said he intended to send letters to trading partners in the next one to two weeks setting unilateral tariff rates, ahead of a July 9 deadline to reimpose higher duties on dozens of economies. “We’re going to be sending letters out in about a week and a half, two weeks, to countries, telling them what the deal is,” Trump told reporters Wednesday at the John F. Kennedy Center for the Performing Arts in Washington where he was attending a performance. “At a certain point, we’re just going to send letters out. And I think you understand that, saying this is the deal, you can take it or leave it,” he added.

US/CHINA (MNI): China, U.S. to Maintain Dialogue - MOFCOM

MNI (Beijing) China and the U.S. will keep talking using the economic and trade negotiation mechanism, constantly enhancing consensus, reduce misunderstandings and strengthen cooperation, He Yadong, spokesman of the Ministry of Commerce told reporters Thursday. Beijing will consider reasonable demands for rare earth-related items in the private sector, and keep strengthening the approval of compliant applications for export licenses, said He. MNI reported earlier that the framework reached during China-U.S. talks in London could pave the way for a trade deal by mid-August, potentially including Chinese purchases of U.S.

US/JAPAN (BBG): Japan and US Still Far Apart in Tariff Talks, PM Cited as Saying

Japanese Prime Minister Shigeru Ishiba still sees distance with the US when it comes to trade talks, according to an opposition party leader who met with the leader to discuss US tariffs. Ishiba is expected to meet US President Donald Trump on the sidelines of the Group of Seven leaders gathering in Canada starting Sunday. Ahead of that potentially key meeting, the prime minister gathered with opposition party leaders Thursday to canvass their thoughts on the American levies.

US/N.KOREA (BBG): Trump Open to Dialogue With Kim Jong Un, White House Says

President Donald Trump remains open to communications with North Korean leader Kim Jong Un, the White House said in its latest comments expressing willingness to resume dialogue with the nuclear-armed North, despite little signal from Kim seeking engagement. “The President remains receptive to correspondence with Kim Jong Un and he’d like to see the progress that was made at that summit in Singapore,” White House Press Secretary Karoline Leavitt told reporters on Wednesday when asked about a media report that said Trump tried to send a letter to Kim but was rebuffed.

US (BBG): Trump Wishes Musk Well, No Desire for Longterm Feud, Vance Says

It would be Elon Musk’s loss if he and President Trump didn’t make amends, Vice President JD Vance says. Vance says we are grateful for Musk did for Trump but it’s up to him. Vance responds to a reporter’s question about if Trump would accept Musk as an informal adviser.

ISRAEL/IRAN (NYT): Israel Appears Ready to Attack Iran, Officials in U.S. and Europe Say

Israel appears to be preparing to launch an attack soon on Iran, according to officials in the United States and Europe, a step that could further inflame the Middle East and derail or delay efforts by the Trump administration to broker a deal to cut off Iran’s path to building a nuclear bomb. The concern about a potential Israeli strike and the prospect of retaliation by Iran led the United States on Wednesday to withdraw diplomats from Iraq and authorize the voluntary departure of U.S. military family members from the Middle East. It is unclear how extensive an attack Israel might be preparing. But the rising tensions come after months in which Prime Minister Benjamin Netanyahu of Israel has pressed President Trump to seize on what Israel sees as a moment of Iranian vulnerability to a strike.

IRAN (MNI): Official Claims 'Friendly' Country Warns of Possible Israeli Attack

Reuters reports comments from an unnamed senior Iranian official. Says that mounting regional tensions are "psychological warfare" aimed at influencing Tehran's nuclear talks with the US on Sunday (15 June). Says that Iran will not abandon its right to uranium enrichment despite heightened regional tensions. Adds that a "friendly" country in the region has alerted Tehran about a potential Israeli attack. This comes hours after CBS reported that the US ordered the evacuation of non-essential embassy staff and their dependents in the Iraqi capital, Baghdad. This is due to the US being concerned that possible Israeli strikes on Iran could lead to Tehran targeting US sites in the region.

IRAN (MNI): IAEA Pass Resolution Declaring Iran Non Compliant, Awaits Tehran Response

The International Atomic Energy Agency (IAEA)'s Board of Governors has passed a resolution declaring Iran in non-compliance with its nuclear safeguarding requirements. This is the first time since 2005 that such a resolution has been passed. In the event, 19 countries voted in favour of the resolution, with three (Burkina Faso, China, and Russia) voting against and 11 abstentions. On 11 June, Iran's envoy to the IAEA Reza Najafi said to AFP that Tehran would show a "very severe reaction" if the resolution passed. The resolution now goes to the UN Security Council, where it may adopt further sanctions. Najafi: "If such a scenario unfolds, Iran's options will be firm, and the United States and the E3 will bear full responsibility."

ECB (BBG): ECB’s Simkus Says It’s Important to Take a Pause on Rates

European Central Bank Governing Council member Gediminas Simkus called for a pause in interest-rate moves, citing “very big uncertainty” over US tariff policy. After eight reductions “we’ve arrived at the neutral level — it’s now important to maintain the freedom of potential decision, not to commit to one direction or another,” the Lithuanian central bank chief said in Vilnius on Thursday. “The economic situation is very unclear — no one knows what the US decisions will be on July 9.”

ECB (BBG): ECB’s Villeroy Says No Fixed Position on Future Rate Decisions

European Central Bank Governing Council member Francois Villeroy de Galhau said he has no fixed position on future interest rate moves and that decisions will depend on data. “For future rates, we’ll see depending on how inflation evolves,” he told Franceinfo radio on Thursday. “I never have a fixed position in advance — I believe in pragmatism and agility on monetary policy, we’ll see.”

NETHERLANDS/PENSIONS (PensioenPro): Van Hijum Wants to Give Funds Up to an Extra Year to Adjust Interest Rate Hedging

After entering, funds may take up to twelve months to implement new investment and interest rate hedging policies, according to a proposed decision. The extra time is welcome, because speculators are active on the swap market.

GERMANY (MNI): IFO Upwardly Revises Growth Forecasts, Calling Low Point Being Passed

IFO upwardly revised its German growth forecast, by 0.1pp to 0.3% 2025 and, more significantly, 0.7pp to 1.5% in 2026. "The crisis in the German economy reached its low point in the winter", IFO comment. "Economic researchers see risks in US trade policy. The import tariffs already imposed - assuming they remain at the current level - will impact economic growth by 0.1 percentage points in 2025 and 0.3 percentage points in 2026. If an agreement is reached in the trade conflict, growth in Germany could be higher, while an escalation could lead to a renewed recession."

NORWAY (MNI): Solid Activity/Employment Signals From Q2 RNS; NB in No Rush to Cut

Norges Bank's Q2 Regional Network Survey has been released - the last major input ahead of the June 19 decision. A first glance at the survey does not suggest Norges Bank should be in a rush to cut rates - certainly not at next week's decision (in line with consensus and market pricing). Activity and employment signals appear positive, there are limited changes in capacity utilisation, and wage growth expectations were revised up a touch. Recent growth data has pointed to an economy that is coping relatively well with rates at 4.50%. This survey underscores that view. However, guidance that "the policy rate will most likely be reduced in the course of 2025" remains intact.

DATA

UK DATA (MNI): Monthly GDP, Trade Disappoint; Labour Data More Important for MPC

- UK APR GDP -0.3% M/M, +0.7% 3MM, +1.1% 3M Y/Y

- UK APR SERVICES INDEX -0.4% M/M, +0.6% 3MM

- UK APR CONSTRUCTION OUTPUT +0.9% MM, +0.5% 3M3M, +3.3% YY

- UK APR IND PROD -0.6% M/M, -0.3% Y/Y

- UK APR MANUF OUTPUT -0.9% M/M, +0.4% Y/Y

- UK APR TRADE BALANCE GBP -7.03BN

Looking a bit more into the UK GDP data, there are some inconsistencies in the Bloomberg survey. As this is the first print of the quarter the prior series was not open for revisions and yet the 3m/3m GDP print came in line with expectations at 0.7% while the M/M print missed by two tenths at -0.3%. There are less survey respondents for the former, and they tend to be the larger institutions so this might not be as much of a surprise as expected. Looking at the breakdown it appears construction was stronger than expected with all other subcomponents softer. We are only one month into the quarter but with zero growth between Q1 and the April print, we would need some revisions or very strong May and / or June data in order to meet the BOE's 0.1% Q/Q forecast.

SWEDEN DATA (MNI): Weak Labour Demand Signals From PES Labour Market Report

The Public Employment Service's (PES) May labour market report does not do enough to push back against market pricing in favour of a 25bp Riksbank cut next Wednesday. The unemployment claims rate was steady at 7.0% for the seventh consecutive month, but monthly vacancies fell to the lowest since September 2020 (-24% Y/Y). This pulled the PES vacancies-to-unemployment claims ratio down to a 4-year low of 0.21. The softening of labour demand implied by the vacancies data is consistent

with the recent fall in the Economic Tendency Indicator's expected employment metric.

AUSTRALIA DATA (MNI): Inflation Expectations Highest Since 2023

Melbourne Institute consumer inflation expectations for June jumped to 5.0% from 4.1%, the highest and first print above 5% in almost two years. They were 4.4% in June 2024. They reached a trough in March of 3.6% and have been higher since likely boosted by concerns over the impact of US tariffs on inflation and higher petrol prices since then. The RBA will likely only be concerned if elevated inflation expectations and the causes persist and risk changing wage-setting behaviour.

FOREX: EUR Still Key Beneficiary in Soft USD Environment

- A poor monthly GDP release from the UK works further in favour of a sell-on-rallies theme for GBP, most evident in the return higher for EUR/GBP and the (initial) slippage for GBP/USD this morning, which has prevented a material test on 1.3600 so far. A technical correction lower would target 1.3504 ahead of layered support between 1.3434-44, marked by a series of historic highs (Sep'24, Apr'25) as well as the 38.2% retracement of the upleg off mid-May low. For EUR/GBP, the break higher has been exacerbated by a break of resistance at 0.8442, the 50-day EMA, highlighting a stronger reversal. 0.8541 will likely garner attention next, the May 2 high.

- A returning soft-USD theme continues to dictate play, with Trump's confirmation of incoming unilateral tariffs on countries without a trade deal affirming the year's USD downtrend.

- The EUR remains a key beneficiary of this market backdrop, with momentum boosting EUR/USD through the post-ECB peak at 1.1495, confirming an extension of the current bull cycle. Sights remain firmly on 1.1573 (Apr 21 high and bull trigger), even as gains for EUR/JPY have begun to slow.

- Softer risk sentiment stemming from increased geopolitical tensions around Iran headline are largely responsible, as President Trump talks down the likelihood of a nuclear deal with Iran, and reports continue to circulate of a potential Israeli operation on the region to stem Tehran's nuclear ambitions.

- After a string of weak releases, the weekly jobless claims data due today will be watched for any further signs of softness which, if backed up by a miss on expectations in today's PPI, would add to the downside dollar argument.

- ECB speak is plentiful, with Schnabel, Patsalides, Muller, de Guindos all on the docket. The Fed remain inside their pre-decision media blackout period.

EGBS: Dutch Pension Reform-led 10s30s Flattening Unwinds

Early flattening in the German/EUR swap 10s30s curves has partially unwound. The 10s30s Bund curve is now 0.3bps flatter today at 46.6bps, after reaching a low of 45bps around the equity cash open.

- News around Dutch pension reforms was touted as a driver of the moves in Bunds and swaps, with local media pointing to a proposal for a 12-month phase in period for reforms after funds subscribe. A reminder that the Dutch pension reform disincentivises hedging of pension funds’ long-term liabilities (e.g. using 30-year fixed receivers) owing to a move towards defined contribution schemes from defined benefit schemes. The phase in stage mentioned above would allow a slower transition and seemingly delay any related pension reallocation/reduction in flows.

- Moves in German ASWs were consistent with this narrative, with Buxl spreads tightening and Bund spreads widening slightly.

- Buxl futures are up 102 ticks at 121.74, off today’s 122.26 high. Bund futures are +41 ticks at 131.21, down from a 131.27 high. The technical trend in Bund futures remains bullish, with initial firm resistance at 131.47 (June 5 high).

- 10-year EGB spreads to Bunds are biased wider owing to the Bund outperformance, with risk sentiment also hampered by ongoing geopolitical tensions between Israel and Iran. 3/7/30-year BTP supply was digested smoothly.

- Several ECB policymakers have spoken this morning, with no fresh monetary policy signals to note.

GILTS: Bull Flattening After Data & EGB Spillover, 50bp BoE Cuts Show Thru Dec

Gilts hold the bulk of their early gains after the mostly softer-than-expected UK monthly economic activity data and some spillover from EGBs following latest Dutch pension reform news drove bullish flattening on the curve.

- Futures printed highest levels of the week at 93.10.

- The recent bullish cycle has extended. A break of session highs would expose Fibonacci resistance levels (93.26/47), which protect the May 8 high drawn off a continuation chart (93.59).

- Yields 3-5bp lower, curve flatter.

- 2s10s and 5s30s curves rangebound, after recent moves back above 60bp and 120bp, respectively.

- 10-Year gilt/Bund spread little changed on the day at 201.5bp, with the impact of the UK data offset by the readthrough from the Dutch pension news. Gilt bulls haven’t been able to force a close below 200bp in recent days.

- BoE-dated OIS prices 50bp of cuts through year-end vs. 48.5bp late yesterday.

- SFIZ5 and Z6 traded to the highest levels of the month. Z5 eyes May 12 highs (96.365), while Z6 eyes the May 9 top (96.545).

- Little of note on the UK calendar for the rest of the day, with ongoing assessment of the local data and macro inputs (U.S. PPI & weekly claims data) eyed.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Jun-25 | 4.206 | -0.7 |

Aug-25 | 4.016 | -19.7 |

Sep-25 | 3.950 | -26.3 |

Nov-25 | 3.793 | -42.0 |

Dec-25 | 3.710 | -50.3 |

Feb-26 | 3.598 | -61.5 |

Mar-26 | 3.569 | -64.3 |

EQUITIES: Moving Average Studies for Eurostoxx 50 Futures in Bull-Mode Position

Eurostoxx 50 futures are trading inside a range for now. The trend condition is bullish - moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen the bull theme. Key support to watch lies at 5295.43, the 50-day EMA. A clear break of this average would signal a possible reversal. The trend condition in S&P E-Minis remains bullish and the contract traded to a fresh cycle high yesterday, reinforcing current bullish conditions. The recent break of 5993.50, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. Sights are on 6080.75 next, the Feb 26 high. Key support to watch lies at 5816.70, the 50-day EMA.

- Japan's NIKKEI closed lower by 248.1 pts or -0.65% at 38173.09 and the TOPIX ended 5.75 pts lower or -0.21% at 2782.97.

- Elsewhere, in China the SHANGHAI closed higher by 0.342 pts or +0.01% at 3402.658 and the HANG SENG ended 331.56 pts lower or -1.36% at 24035.38.

- Across Europe, Germany's DAX trades lower by 320.65 pts or -1.34% at 23629.29, FTSE 100 lower by 8.81 pts or -0.1% at 8855.51, CAC 40 down 62.29 pts or -0.8% at 7713.61 and Euro Stoxx 50 down 57.89 pts or -1.07% at 5335.26.

- Dow Jones mini down 222 pts or -0.52% at 42680, S&P 500 mini down 31.25 pts or -0.52% at 5996.75, NASDAQ mini down 124.5 pts or -0.57% at 21761.25.

Time: 09:50 BST

COMMODITIES: Gains for WTI Futures This Week Mark Acceleration of Bull Phase

WTI futures have traded higher this week and yesterday’s gains mark an acceleration of the current bull phase. The contract has cleared all key retracement points of the Apr 2 - 9 bear leg and this signals scope for an extension towards $71.10 the Apr 2 high and a key hurdle for bulls. A break of this level would strengthen the bullish condition. On the downside, initial firm support to watch is $63.04, 50-day EMA. A bullish theme in Gold remains intact and the latest pullback appears corrective. Medium-term trend signals remain bullish - moving average studies are in a bull-mode position, highlighting a dominant uptrend. An extension higher would open $3435.6 next, the May 7 high. A break of this hurdle would strengthen bullish conditions. On the downside, support to monitor is $3249.9, the 50-day EMA.

- WTI Crude down $0.53 or -0.78% at $67.63

- Natural Gas up $0.08 or +2.31% at $3.581

- Gold spot up $4.11 or +0.12% at $3358.67

- Copper down $2 or -0.42% at $479.3

- Silver down $0.27 or -0.73% at $35.9665

- Platinum up $5.01 or +0.4% at $1264.83

Time: 09:50 BST

| Date | GMT/Local | Impact | Country | Event |

| 12/06/2025 | - | *** | Money Supply | |

| 12/06/2025 | - | *** | New Loans | |

| 12/06/2025 | - | *** | Social Financing | |

| 12/06/2025 | 1200/1400 | ECB de Guindos At Financial Integration Conference | ||

| 12/06/2025 | 1220/1420 | ECB Schnabel At Financial Integration Conference | ||

| 12/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 12/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 12/06/2025 | 1230/0830 | * | Household debt-to-income | |

| 12/06/2025 | 1230/0830 | *** | PPI | |

| 12/06/2025 | 1400/1000 | * | Services Revenues | |

| 12/06/2025 | 1415/1615 | ECB Elderson At Senior Supervisors Conference | ||

| 12/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 12/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 12/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 12/06/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/06/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 13/06/2025 | 2301/0001 | ** | KPMG/REC Jobs Report | |

| 13/06/2025 | 0430/1330 | ** | Industrial Production | |

| 13/06/2025 | 0600/0800 | *** | Final Inflation Report | |

| 13/06/2025 | 0600/0800 | *** | HICP (f) | |

| 13/06/2025 | 0645/0845 | *** | HICP (f) | |

| 13/06/2025 | 0700/0900 | *** | HICP (f) | |

| 13/06/2025 | 0830/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey | |

| 13/06/2025 | 0900/1100 | ** | Industrial Production | |

| 13/06/2025 | 0900/1100 | * | Trade Balance | |

| 13/06/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 13/06/2025 | 1230/0830 | ** | Wholesale Trade | |

| 13/06/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 13/06/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 13/06/2025 | 1500/1700 | ECB Elderson At Senior Supervisor's Conference | ||

| 13/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 13/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |