MNI US OPEN - Trump Announces Fresh Tariffs on Pharmaceuticals

EXECUTIVE SUMMARY

- TRUMP PLANS NEW TARIFF PUSH WITH 100% RATE ON PATENTED DRUGS

- TRUMP TAKES AIM AT CHIP MAKERS WITH NEW PLAN TO THROTTLE IMPORTS: WSJ

- JAPAN SEPT TOKYO CORE CPI RISES 2.5% VS. AUG 2.5%

- 12-MONTH EUROZONE CONSUMER INFLATION EXPECTATIONS ACCELERATE

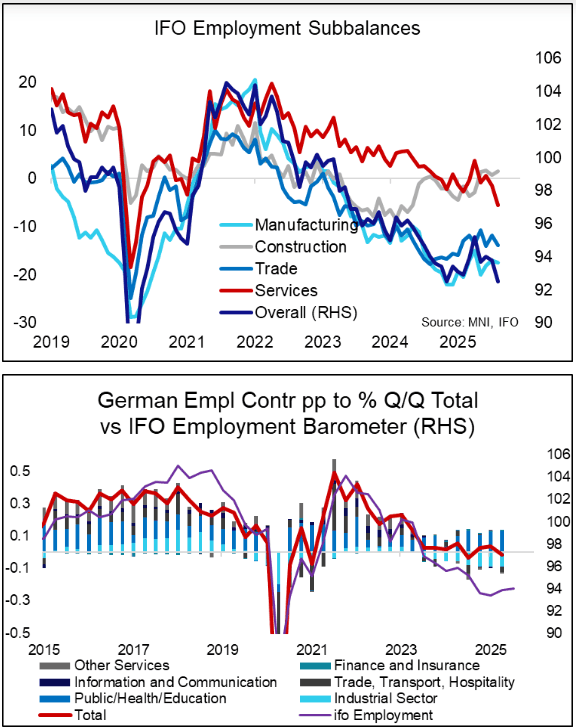

Figure 1: German IFO Employment Barometer Reaches 5-Year Low in September

NEWS

US (BBG): Trump Plans New Tariff Push With 100% Rate on Patented Drugs

President Donald Trump announced a fresh round of tariffs on pharmaceuticals, heavy trucks and furniture, including a 100% duty on patented drugs unless the producer is building a manufacturing plant in the US. “Starting October 1st, 2025, we will be imposing a 100% Tariff on any branded or patented Pharmaceutical Product, unless a Company IS BUILDING their Pharmaceutical Manufacturing Plant in America,” Trump posted on social media Thursday, without offering specifics on which producers will be impacted. “There will, therefore, be no Tariff on these Pharmaceutical Products if construction has started.”

US (WSJ): Trump Takes Aim at Chip Makers With New Plan to Throttle Imports

The Trump administration is weighing a new plan to reduce dramatically the U.S.'s reliance on semiconductors made overseas, hoping to spur domestic manufacturing and reshape global supply chains. The policy's goal is to have chip companies manufacture the same number of semiconductors in the U.S. as their customers import from overseas producers. Companies that don't maintain a 1:1 ratio over time would have to pay a tariff, according to people familiar with the concept.

FED (BBG): Logan Says Fed Should Consider Replacing Its Benchmark Rate

Lorie Logan, president of the Federal Reserve Bank of Dallas, has proposed replacing the central bank’s benchmark federal funds rate — the primary tool the central bank has used to steer the nation’s economy since the 1980s — with a much more widely used market bellwether. In a speech delivered Thursday and in an accompanying essay, Logan unexpectedly rekindled a debate that market participants say is long overdue.

US/TURKEY (BBG): Turkey Announces Jumbo Boeing Order After Trump-Erdogan Meeting

Boeing Co. landed one of its biggest deals this year, with Turkish Airlines agreeing to buy as many as 225 jets following a White House meeting between President Donald Trump and Turkey’s Recep Tayyip Erdogan. Turkey’s flagship carrier will purchase 50 787 Dreamliners, with options for 25 more, according to a stock exchange filing Friday. Deliveries are scheduled between 2029 and 2034. Talks with Boeing for 150 narrowbodies — 100 firm and 50 options for the 737 Max 8 and Max 10 — have also been completed, pending a final agreement with engine maker CFM International Inc., Turkish Airlines said.

EUROPE/RUSSIA (BBG): Europeans Privately Tell Russia They’re Ready to Shoot Down Jets

European diplomats warned the Kremlin this week that NATO is ready to respond to further violations of its airspace with full force, including by shooting down Russian planes, according to officials familiar with the exchange. At a tense meeting in Moscow, British, French and German envoys addressed their concerns about an incursion by three MiG-31 fighter jets over Estonia last week, according to the officials, who spoke on condition of anonymity as the talks took place behind closed doors. Following the conversation, they concluded that the violation had been a deliberate tactic ordered by Russian commanders.

UK (The Times): Reform on Brink of Outright Majority if Election Were Held Today

YouGov’s second seat-by-seat poll since Labour’s election victory last year suggests that Nigel Farage’s chances of entering Downing Street have significantly increased, putting him in pole position to become prime minister. Reform, which currently has just five MPs, is on track to have 311, which would make it comfortably the largest party in a hung parliament. It is a significant improvement on the same last such poll in June, when the party was on track to have 271 MPs and would put it within touching distance of the 326 MPs needed for an outright majority.

UK (The Telegraph): Starmer Allies Would Stop Burnham From Running for Parliament

Sir Keir Starmer’s allies are planning to block Andy Burnham’s return to Parliament, The Telegraph can reveal. Senior party figures want to bar the Labour Mayor from being selected for a Parliamentary seat, after he revealed that MPs were pushing for him to launch a leadership challenge against the Prime Minister. Mr Burnham’s candid comments about his desire to replace Sir Keir, which came in a Telegraph interview, have stirred up a civil war between supporters of the two men in Westminster.

DATA

EUROZONE DATA (MNI): 12-Month Eurozone Consumer Inflation Expectations Accelerate

- ECB 1-YEAR CONSUMER INFLATION EXPECTATIONS 2.8%

- ECB 3-YEAR CONSUMER INFLATION EXPECTATIONS 2.5%

Consumer inflation expectations across the eurozone over the next 12 months increased to 2.8% in August, accelerating from 2.6% in July, according to the latest ECB Consumer Expectations Survey. Expectations for three years ahead were unchanged at 2.5%, while the outlook inflation five years ahead increased to 2.2%, from 2.1%

in Jul the highest value observed since August 2022. Uncertainty about inflation expectations over the next 12 months increased slightly in August, the survey showed.

GERMANY DATA (MNI): IFO Employment Barometer Reaches 5-Year Low in September

The IFO employment barometer fell in September, to 92.5 points, down from 93.8 in August. This is the lowest level in the series since June 2020. "The mood on the labor market remains subdued [...] because the upturn has failed to materialize for the time being, many companies are applying the brakes on their headcount", IFO comments. The main driver for the overall deterioration was a weaker services reading, falling to -5.5 points, the lowest since May 2020 and comparing to August's -1.4. As the headline reading, the series has been on a downtrend since 2022. "Individual companies in the transport and logistics sector have already announced layoffs", IFO comments.

SPAIN DATA (MNI): Q2 GDP Revised Up, Annual Adjustments Revise Up Back Data

- SPAIN Q2 FINAL GDP +3.1% Y/Y

- SPAIN Q2 FINAL GDP +0.8% Q/Q

Spain Q2 final GDP +0.8% Q/Q, +3.1% Y/Y - revised up from flash (+0.7% Q/Q, +2.8% Y/Y). There were also revisions to previous quarters back to Q1 2022, in line with the annual update that was published on 19 September. Looking at the most recent quarters, Q225, Q325 and Q425 were all revised up by a tenth in Q/Q terms. Since the beginning of 2024, the quarterly Y/Y numbers have all been revised up by 0.2-0.4ppt.

ITALY DATA (MNI): Stagnant Business Sentiment But Some Signs of Tariff Reprieve

Italian business confidence was essentially stagnant in September, printing at 93.7 after 93.6 in July and August. That said, sentiment remains above the 2005-2019 average of 91.6. Details of the manufacturing and consumer confidence readings suggest some positive readthrough from lower US tariff policy uncertainty. The industry breakdown saw a tick up in services to 95.6 (vs 95.1 in August, 93.9 in July and 95.6 in June), but a more notable fall in retail to 101.6 (vs 102.7).

SWEDEN DATA (MNI): Sharp Fall in Swedish Vehicle Exports to US Before EU-US Trade Deal

The Swedish goods trade balance slipped into deficit in August (-SEK8.9bln vs SEK3.6bln prior), but that's in line with seasonal norms. On a 12-month rolling basis, net exports were SEK65.9bln, down from SEK68.5bln in July for the lowest trade surplus since last November. This reflected a larger declined in 12-month rolling exports compared to imports. Country-level data is only available as of June. In June, Sweden's trade surplus with the US declined to SEK102.0bln, the lowest since mid-2022.

JAPAN DATA (MNI): Japan Sept Tokyo Core CPI Rises 2.5% vs. Aug 2.5%

- JAPAN SEPT TOKYO CORE CPI +2.5% Y/Y; AUG +2.5%

- JAPAN SEPT TOKYO CORE-CORE CPI +2.5% Y/Y; AUG +3.0%

- JAPAN SEPT SERVICES PRICES +1.5% Y/Y; AUG +2.0%

Tokyo’s core CPI rose 2.5% y/y in September, unchanged from August and above the Bank of Japan's 2% target for the 11th straight month, the Ministry of Internal Affairs and Communications said Friday. The index was lifted by energy prices (+2.7% vs -5.3% in August) but dragged down by food excluding perishables (+6.9% vs +7.4%). Core-core CPI, excluding fresh food and energy, a key gauge of underlying inflation, slowed to 2.5% y/y from 3.0% but remained above 2% for the seventh month.

RATINGS: Potential for Further Positive Action on Spain, Negative for France

Potential sovereign rating reviews of note scheduled for after hours on Friday include:

- Fitch on Spain (current rating: A-; Outlook Positive) & Sweden (current rating: AAA; Outlook Stable)

- Moody’s on Spain (current rating: Baa1; Outlook Positive)

- S&P on the Czech Republic (current rating: AA-; Outlook Stable)

- Morningstar DBRS on Croatia (current rating: A, Stable Trend

- Scope Ratings on Croatia (current rating: A-; Outlook Stable) & France (current rating: AA-; Outlook Stable)

FOREX: DXY Consolidating Bullish Advance, USDJPY Eyes 150.00

- Although the USD index has eased off its recovery highs made Thursday, the DXY is broadly consolidating the impressive advance following the stronger set of US data on Thursday, boosting the post-Fed recovery to around 2.5%. The technical breach of the 50-day EMA for the index is a positive development, placing extra focus on upcoming US data releases and in particular next week’s US employment report.

- Intra-day ranges across the G10 have remained contained on Friday, allowing both GBP and NZD to consolidated at depressed levels following their significant technical breaks.

- For GBPUSD (-0.83%) specifically, we highlighted the breach of two support trendlines, drawn from both the Aug 01 and the January lows. Spot moved sharply lower to bridge the gap to the first target of 1.3333, the Sep 3 low and a key support. Below here, a key medium-term level resides at 1.3140.

- For NZDUSD (-0.86%), spot sits comfortably below the noted pivot level of 0.5800, of which the downside break has bolstered the bearish theme. 0.5728 and 0.5636 are the most obvious targets for a deeper selloff.

- USDJPY rose to within 4 pips of the 150 mark overnight, and its notable that the USDJPY recovery has outpaced that of the DXY, rallying 3.07% at its peak. A bullish candle pattern on Sep 17 - a hammer - provided an early reversal signal which remains valid. Sights are on 150.92, the Aug 1 high and key resistance.

- On Friday, the monthly Personal Income and Outlays report for August will provide greater clarity on recent momentum. Core PCE will also be watched with it widely expected to print softer than the 0.35% M/M seen for core CPI.

EGBS: Bund Futures Off Session Lows, 10-Year Yields Still Within 2.6-2.8% Range

Demand in Bund futures came just ahead of initial support at yesterday’s low (127.88), with the contract basing at 127.89. Bunds are now +11 ticks at 128.11.

- Looking at the cash space, that leaves the September high of 2.801% in 10s untouched, with the contract trading almost exclusively within the 20bp 2.60-2.80% range since late July.

- The German curve lean bull flatter, with 5s30s down another 1bp and narrowing the gap to trendline support (drawn from the June 20 low) at ~95.5bps.

- BTP/Bund spread widening into today's heavy Italian supply and a move off session highs in European equities also provided support to Bunds.

- Smooth passage Italian supply, including a solid bid/cover at the 10-Year BTP offering, has allowed BTP/Bunds to tick away from session highs, now little changed at ~83.5bps.

- Data hasn’t been market moving (as expected). ECB 3-year consumer expectations were steady at 2.5%, but below the 2.4% consensus. Spanish GDP saw broad-based revisions going back to 2023 – generally pointing to a better trajectory in 2024/25.

- Global focus turns to the US August PCE report at 1330BST.

GILTS: Off Lows Alongside Peers, Bearish Theme Remains Present

Gilts have recovered after initially selling off at the open, with cues from wider core global FI dominating thus far.

- Futures printed as low as 90.26, trading through support at the September 4 low (90.31), before a recovery to 90.60, +10 on the day.

- Still, the bearish technical pressure is deepening, with moving average studies already in a bear mode set up.

- Further weakness would expose Fibonacci support (89.94), while initial resistance is located at the September 24 high (91.28).

- Yields 2-3bp lower, curve steeper at the margin.

- Ongoing UK fiscal deterioration continues to limit rallies at this stage and keeps the curve steepening theme intact, with 2s10s and 5s30s remaining within their steepening trends despite the recent pullback.

- Increasing pressure on PM Starmer is also noted, but this hasn’t become a meaningful issue for markets as of yet.

- SONIA futures off lows alongside the recovery in bonds, last -1.0 to +1.0.

- BoE-dated OIS prices ~4.55bp of easing through December, with the next 25bp cut still not fully discounted until the end of the April MPC.

- Little of note on the UK calendar ahead of the weekend, which will leave cross-market and macro cues at the fore.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Nov-25 | 3.960 | -0.7 |

Dec-25 | 3.923 | -4.5 |

Feb-26 | 3.814 | -15.3 |

Mar-26 | 3.783 | -18.5 |

Apr-26 | 3.706 | -26.2 |

Jun-26 | 3.691 | -27.7 |

EQUITIES: EuroStoxx 50 Futures Close to Recent Highs, Trend Conditions Bullish

Eurostoxx 50 futures are trading closer to their recent highs. The contract has cleared resistance around the 20-day EMA - a bullish development - and the subsequent rally reinforces a bullish theme. The move signals potential for a climb towards 5525.00, the Aug 22 high and a bull trigger. On the downside, key support to monitor is 5302.00, the Sep 2 low. Clearance of this level is required to reinstate a bearish theme. A bull cycle in S&P E-Minis remains intact and the latest pullback is considered corrective - for now. The contract has pierced initial support at the 20-day EMA, at 6634.71. A clear breach of this average would signal scope for a deeper retracement, potentially towards the 50-day EMA, at 6519.15. Key short-term resistance has been defined at 6756.75, the Sep 22 high where a break would resume the primary uptrend.

- Japan's NIKKEI closed lower by 399.94 pts or -0.87% at 45354.99 and the TOPIX ended 1.67 pts higher or +0.05% at 3187.02.

- Elsewhere, in China the SHANGHAI closed lower by 25.196 pts or -0.65% at 3828.106 and the HANG SENG ended 356.48 pts lower or -1.35% at 26128.2.

- Across Europe, Germany's DAX trades higher by 112.15 pts or +0.48% at 23647.59, FTSE 100 higher by 37.01 pts or +0.4% at 9250.94, CAC 40 up 50.13 pts or +0.64% at 7845.55 and Euro Stoxx 50 up 27.25 pts or +0.5% at 5472.14.

- Dow Jones mini up 82 pts or +0.18% at 46353, S&P 500 mini up 3.75 pts or +0.06% at 6663.75, NASDAQ mini down 22.75 pts or -0.09% at 24606.5.

Time: 10:00 BST

COMMODITIES: Despite This Week's Gains, WTI Future Trend Remains Bearish

WTI futures are trading at this week’s highs. Despite recent gains, the trend condition remains bearish and the recovery is considered corrective - for now. Initial resistance to watch is $65.43, the Sep 2 high. A clear break of it would suggest potential for a stronger recovery, towards key short-term resistance at $68.43, the Jul 30 high. On the downside, key support and the bear trigger has been defined at $60.85, Aug 13 low. The trend condition in Gold is unchanged and a bull cycle remains in play. A fresh all-time high once again, on Tuesday, confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is the $3800.0 handle. Initial firm support lies at $3622.2, the 20-day EMA. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend.

- WTI Crude up $0.18 or +0.28% at $65.17

- Natural Gas down $0.02 or -0.59% at $2.905

- Gold spot up $4.55 or +0.12% at $3753.93

- Copper down $1.05 or -0.22% at $474.8

- Silver down $0.05 or -0.12% at $45.1255

- Platinum up $10.22 or +0.67% at $1539.39

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 26/09/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 26/09/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 26/09/2025 | 1300/0900 | Richmond Fed's Tom Barkin | ||

| 26/09/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 26/09/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 26/09/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 26/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/09/2025 | 1700/1300 | Fed Vice Chair Michelle Bowman |