GERMAN DATA: IFO Employment Barometer Reaches 5-Year Low In September

Sep-26 07:57

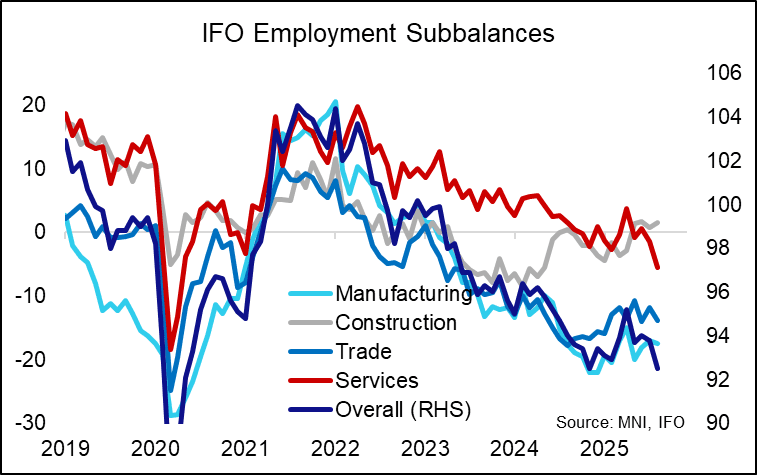

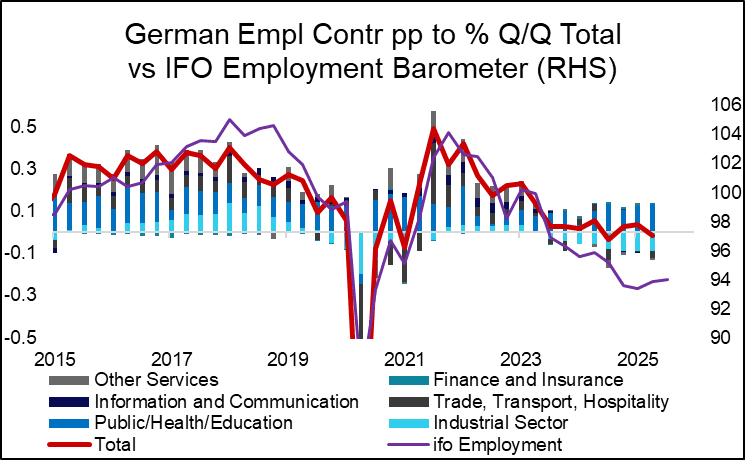

The IFO employment barometer fell in September, to 92.5 points, down from 93.8 in August. This is the lowest level in the series since June 2020. "The mood on the labor market remains subdued [...] because the upturn has failed to materialize for the time being, many companies are applying the brakes on their headcount", IFO comments.

- The main driver for the overall deterioration was a weaker services reading, falling to -5.5 points, the lowest since May 2020 and comparing to August's -1.4. As the headline reading, the series has been on a downtrend since 2022. "Individual companies in the transport and logistics sector have already announced layoffs", IFO comments.

- The index for manufacturing has also deteriorated but remains above cycle lows. The correlation to employment changes is the strongest in the sector.

- 'Hard' German labour market data is scheduled for next Tuesday, with the (seasonally-adjusted) unemployment rate expected to remain stable at 6.3% (consensus consisting of 5 analysts for now).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Futures Rebound From Fresh Cycle Lows

Aug-27 07:56

Gilt futures (Z5) registered a fresh cycle low at the open, basing at 90.22 before a recovery to 90.55 as wider core global FI firms.

- Bears remain in technical control. Fresh extension lower would target the key support at the May 22 low (90.11) on a continuation chart. Bulls need to retake 91.24 to start turning the tide in their favour.

- Yields ~2bp lower across the curve.

- Fiscal fragility remains the key topic from a domestic perspective, while the recent hawkish repricing further forwards on the curve holds.

- 2s have probed 4.00% in recent days, but bears have failed to force a sustained break above that level. The benchmark hasn’t closed above 4.00% since June 9.

- 10s haven’t tested the April 9 high (4.800%), topping out at 4.765% yesterday.

- 30s ~7bp off their multi decade high (latter located at 5.659%).

- 2s10s last 77.2bp, unable to retest the July high of 80.4bp.

- 5s30s ~2bp below cycle highs (~149bp), registered earlier this month.

- Little of note on the UK macro calendar today, but the DMO will come to market with GBP5bln of the 4.375% Mar-28 gilt this morning.

- Note that the minutes of the latest DMO consultation with market participants pointed to an ongoing preference for a reduction in WAM. Details of syndication preferences can be found in recent bullets. We will provide deeper thoughts on the update tomorrow.

BONDS: Spiking higher in the Past few minutes

Aug-27 07:54

- A peculiar bid in Govies in the last few minutes, and speaking to many desks very little was seen as a new news, or headline.

- There was some notable pick up in flows, Bund was bought in 6k, Bobl 5k, that's despite the German supply coming up this Morning.

- Schatz was bought in 5k, BTP 1k and ERU5 in 5k.

- Volumes are on the low side overall and may have helped exacerbate some of the moves.

- Bund is testing the initial resistance at 129.62.

USD: Putting some pressure on the EUR

Aug-27 07:45

- Some broader lows for the EUR here, initially a function of the Dollar bid, but the Currency is now testing intraday lows against the GBP, USD, JPY, CAD, CHF, TRY.

- The Dollar breaks new highs versus the GBP, AUD, TWD, CNH, CHF, PLN, CZK, NOK, MXN, NZD, CAD, and the SEK.

- The EURUSD is testing the 50day EMA right here at 1.1599.

- As the worst performer, the NZDUSD targets 0.5829, Yesterday's low, but Market Participants will look at 0.5800 for better support.