MNI US OPEN - RBNZ Strengthens Easing Bias With 50bp Cut

EXECUTIVE SUMMARY

- EU SEES NEW US TRADE DEMANDS HOLLOWING OUT DEAL STRUCK BY TRUMP: BBG

- RBNZ STRENGTHENS EASING BIAS WITH 50BP CUT

- ERROR IN UK FISCAL DATA BENEFITS GOVERNMENT; BUT ANOTHER ONS DATA ISSUE

- JAPAN REAL WAGES NEGATIVE FOR EIGHTH CONSECUTIVE MONTH

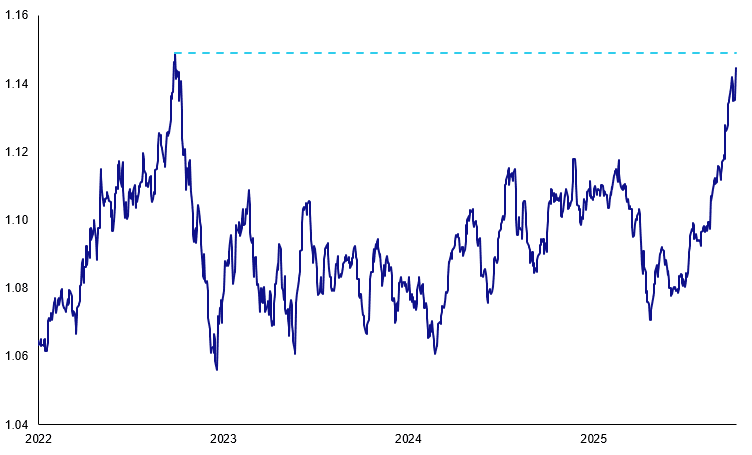

Figure 1: AUD/NZD prints new multi-year high following RBNZ rate cut (chart shows high price)

Source: MNI, Bloomberg Finance L.P.

NEWS

US/EU (BBG): EU Sees New US Trade Demands Hollowing Out Deal Struck by Trump

European Union officials see new US demands for concessions as well as other measures as potentially undercutting a recent agreement that brought the allies back from the brink of a trade war. Earlier this month, US President Donald Trump’s administration sent the EU a fresh proposal for implementing “reciprocal, fair and balanced” trade, according to people familiar with the matter, who spoke on the condition of anonymity to discuss private deliberations.

US (WaPo): Trump Hints At Health Care Deal to End Shutdown, But Key Hurdles Remain

President Donald Trump's pledge Monday that he is open to a health care compromise that could end the government shutdown has Democrats keen to make a deal — and conservatives eager to blow it up. "I'd like to see a deal made for great health care," Trump told reporters in the Oval Office on Monday, responding to questions about Affordable Care Act subsidies set to expire at the end of the year. He later wrote on his Truth Social platform that no deal would be possible until Democrats agree to end the shutdown, which Democrats say they will not do without an agreement on the subsidies.

RBNZ (MNI): MPC Strengthens Easing Bias With 50bp Cut

The Reserve Bank of New Zealand’s Monetary Policy Committee cut the Official Cash Rate by 50 basis points to 2.5% on Wednesday, strengthening its easing bias and citing persistent spare capacity as a downside risk to activity and inflation. The cut, which brought the OCR to its lowest level since July 2022 with 300bp of cumulative easing since August 2024, was largely expected, though markets had only priced about a 50% chance of a reduction by 50 rather than 25bp.

FRANCE (MNI): Suspension of Pension Reform Would Risk Intra-Coalition Rancour

Caretaker Prime Minister Sebastien Lecornu, speaking outside Matignon after the first day of meetings with various political parties in an effort to break through the country's political paralysis, claims that "talks so far are showing a willingness to get this budget through by year-end". Lecornu will present his findings to President Emmanuel Macron later this evening. Adds, "Reducing the deficit is key for France's credibility." There have been some signals that the caretaker administration is considering rolling back Macron's flagship pension reforms in order to gain support from the centre-left Socialist Party (PS).

ECB (BBG): Nagel Says ECB Stance Is Right One With Inflation Close to 2%

The European Central Bank’s policy settings are appropriate for a situation in which inflation is hovering around the 2% target, Governing Council member Joachim Nagel said in an interview with Greek newspaper Kathimerini. “We are currently in a good situation: inflation in the euro area is close to our medium-term target of 2% and expected to remain there over the next years,” Nagel was quoted as saying. “Based on the information currently available to us, I can affirm that our monetary policy stance is the right way forward.”

ECB (BBG): ECB’s Rehn Warns of Downside Risks to Inflation Outlook

European Central Bank Governing Council member Olli Rehn warned that there’s the danger that consumer-price growth slows below the 2% goal. “At the moment we are roughly at that target — in that sense, the situation is currently good,” the Bank of Finland governor told the Karon Grilli podcast. “However, over the next couple of years, there are downside inflation risks in sight — due, among other things, to the strengthening of the euro and stabilization of wage and service inflation.”

ECB (BBG): ECB’s Escriva Says a Rate Cut Isn’t Necessarily the Next Move

European Central Bank Governing Council member José Luis Escrivá said policymakers don’t have a bias toward cutting interest rates at present and could equally end up hiking them instead. The Bank of Spain governor, speaking in an interview on Wednesday at the Bloomberg Future of Finance conference in Madrid, insisted that the current stance doesn’t preclude a move either up or down.

UK (MNI): Error in Fiscal Data Benefits Government; But Another ONS Data Issue

A correction in the public finance data means that the tracking versus the OBR numbers YTD will only be GBP9.4bln (rather than the GBP11.4bln estimated when the data was released on 19 September). And it means that VAT is now tracking GBP1.5bln below the OBR's target versus GBP3.5bln below target in that release. This is of course good news for the government and will be fully incorporated in the next monthly release on 21 October (which will be the last release the OBR will incorporate into its forecasts for the Budget). But it is yet another error at the ONS - albeit this one was due to HMRC data that was sent to the ONS. An HMRC calculation error was also behind the VED issue that caused a correction to PPI recently.

UK (FT): Big Bond Investors Tell Reeves to Build Bigger Fiscal Buffer

Two of the world’s biggest bond investors have urged Rachel Reeves to build a larger buffer into the UK’s public finances in her November Budget to avoid years of uncertainty over tax-and-spend decisions. Pimco and BlackRock said the chancellor needed to go beyond the slim £9.9bn of margin she left against her key borrowing rule at the last two fiscal events, which would force her into harsher tax raises or spending cuts.

UK (The Times): Billions More to Be Spent on Medicine as Keir Starmer Rips Up Rules

Sir Keir Starmer is preparing to rip up NHS value-for-money rules in order to hand more money to the pharmaceutical industry. The prime minister is ready to increase the price at which medicines are deemed cost-effective for the first time ever, under plans to prevent drug companies quitting Britain. Ministers are now locked in a stand-off over where to find billions of pounds to pay more for medicines. NHS chiefs are resisting a raid on their budgets to fund it, while the Treasury says there is no extra cash ahead of a tax-raising budget.

BOE (BBG): Soaring AI Valuations Spur Market Correction Risk, BOE Says

Stretched valuations for artificial intelligence companies and challenges to the Federal Reserve’s independence have fuelled the risks of a “sharp market correction,” the Bank of England said on Wednesday, in its strongest warnings yet. In its quarterly financial stability update, the UK central bank said asset valuations had continued to rise and credit spreads tighten since its June review, despite “persistent material uncertainty around the global macroeconomic outlook.’’

BOE (MNI INTERVIEW): Ex-BOE Markets Head Doubts Mass Repo Tactic

Paul Fisher, former BOE Executive Director Markets, talks to MNI about repo strategy and reserve remuneration. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

BOJ (MNI INTERVIEW): BOJ Dec Hike Possible - Ex-Chief Economist

A former BOJ chief economist shares his policy rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

THAILAND (BBG): Thailand Unexpectedly Holds Rate Under New Chief; Baht Gains

The Bank of Thailand unexpectedly kept its key interest rate unchanged at the first policy meeting under new Governor Vitai Ratanakorn, defying expectations for another cut as officials preserve policy space amid a fragile economy and strong baht. The central bank’s Monetary Policy Committee voted five to two on Wednesday to hold the one-day repurchase rate at 1.50%, as predicted by only six of 26 economists surveyed by Bloomberg. Nineteen had expected a quarter-point cut, while one forecast a half-point reduction.

DATA

GERMANY DATA (MNI): August Manufacturing Sees Broad-Based Drop to Cycle Lows

- GERMANY AUG IND PROD -4.3% M/M (VS +1.3% JUL)

Industrial production in August was much weaker than expectations (-4.3% M/M vs -0.9% cons). Destatis mentions some one-offs for the particularly weak print but the drop to cycle lows remains. On a 3m/3m comparison, IP printed -1.3%. "In August 2025, production in industry excluding energy and construction was down 5.6% from July 2025 after seasonal and calendar adjustment. Within industry, decreases were reported in all three major groups".

SWEDEN DATA (MNI): Flash CPIF Ex-energy in Line With Riksbank Projection; No Policy Signal

- SWEDEN FLASH SEP CPIF +3.09% Y/Y

- SWEDEN FLASH SEP CPIF EX-ENERGY +2.70% Y/Y

CPIF ex-energy at 2.70% Y/Y was in line with the Riksbank's September MPR projection, but a touch below consensus (2.69% Riksbank, 2.8% cons, 2.92% prior). Riksbank likely remains on hold at 1.75% going forward, this flash print doesn't change that outlook. Headline CPIF inflation was 3.09% Y/Y (vs 3.04% Riksbank, 3.25% prior). Full CPI details released next Wednesday.

JAPAN DATA (MNI): Japan Aug Real Wages Negative for Eighth Month

Japan’s inflation-adjusted real wages, a key gauge of households’ purchasing power, fell 1.4% year-on-year in August, marking the eighth consecutive month of decline, preliminary data from the Ministry of Health, Labour and Welfare showed Wednesday. The drop followed a 0.2% fall in July. The data underscore that wage growth continues to lag behind inflation, leaving households under pressure from elevated living costs and increasing calls for the government to step up measures to ease price burdens. The year-on-year rise in total CPI excluding imputed rents slowed to 3.1% in August from 3.6% in July.

JAPAN DATA (MNI): Japan Sentiment Indexes Post 5th Straight Rise

Japan’s Economy Watchers sentiment index rose for a fifth straight month in September, though the government left its overall assessment of the economy unchanged, Cabinet Office data showed Wednesday. The current conditions index, which reflects the views of workers in sectors sensitive to consumer trends, increased to a seasonally adjusted 47.1 in September from 46.7 in August. The outlook index for two to three months ahead also climbed for a fifth consecutive month, rising 1.0 point to 48.5. Sentiment among households and in the labour market improved, while the reading for businesses declined, the survey showed.

FOREX: JPY Slippage Extends, USD Rally Contained by Lower Long-End

- The greenback is higher against all others in G10 headed through to the NY crossover, however the further fade for the US 10y yield across the European morning has contained further strength. The RBNZ 50bps rate cut, further political uncertainty in Japan & France, and a tax collection revision in the UK have been the primary market drivers.

- NZDUSD hit the lowest levels since April and is eyeing a test of next support at 0.5728, the 61.8% retracement of the April/July range as the RBNZ stated “the Committee remains open to further reductions in the OCR” following their outsized cut to prop up the lacklustre domestic economy.

- Meanwhile, JPY weakness continues to run further than market expectations, boosting USDJPY for a fifth consecutive session to hit 152.89. Market moves follow the softer real wages data - which endorse Takaichi's preference for slower rate hikes, however government formation is still the active driver as coalition talks with Komeito continue, delaying the reconvening of the Diet. For USDJPY, this week’s gains reinforce current bullish trend conditions, with technical breaches paving the way for an extension towards 154.39, a Fibonacci retracement point. Initial support to watch lies at 150.92, the Aug 1 high.

- EURGBP meanwhile is edging to new daily lows, despite the tightening of the French-German bond yield spread and seeming optimism of PM Lecornu that a budget agreement can be reached in the near-term. This has pressed through the 50-dma of 0.8676, which had successfully provided intraday support on three occasions over the past month, putting attention on 0.8597, the Aug 14 low. The break lower here stems from the reduction in UK borrowing estimates following ONS VAT revisions this morning - adding to the view that the worst may be behind us for the longer-end of the UK Gilt market headed into November's Budget.

- Focus turns to the Fed meeting minutes, which should shed light on the FOMC's pre-shutdown thoughts on the US economy and policy into year-end. Speakers still due include ECB's Elderson, BoE's Pill and Fed's Musalem, Barr, Goolsbee & Kashkari.

EGBS: 10-Year OAT/Bund Spread Tightens on Cautious French Political Optimism

The 10-year OAT/Bund spread is 3bps tighter on the session at 83bps, amid hopes that French caretaker PM Lecornu will be able to gain enough support to pass a budget in last minute talks today.

- Lecornu is meeting with the Socialist and Green parties this morning. Reports overnight suggested that some in the Macronist bloc may be willing to suspend recent pension reforms as a concession to the left. A deal with the left would reduce near-term political uncertainty in France, but suspension of pension reform would keep domestic public finances on a damaging trajectory. Medium-term risks to OAT/Bund may still be skewed wider.

- EGB curves have bull flattened as a result of the cautious political optimism, with OAT 5s30s down 1bp to 155bps and German 5s30s down 0.5bps to 99bps.

- Futures volumes have been healthy, with ASML equity weakness also supporting the broader FI bid around the European cash equity open. German industrial production was much weaker-than-expected earlier (-4.3% M/M vs -1.0% cons, 1.3% prior)

- Bund futures are +25 ticks at 128.77, with initial resistance of 128.82 containing early upside. OAT futures are +48 ticks at 121.48.

- Germany will hold a 15-year Bund auction at 1030BST, while the ESM has sent an RFP for an upcoming transaction. We pencil in a transaction early next week of around E1.75bln (E1.5-2.0bln.

- Headlines from ECB’s Escriva were broadly consistent with the median Governing Council view (i.e. rates are appropriate at current levels for now, meeting-by-meeting approach with no forward guidance) and his previous comments.

GILTS: Off Highs, Curve Flatter

Gilts are off session highs.

- Early cross-market support came from soft German data and some optimism surrounding the avoidance of fresh elections in France, but that move has stalled.

- The ONS has detected errors in the PSNB data, meaning that the UK’s fiscal situation is marginally less downbeat than was previously envisaged, which has probably driven some gilt curve flattening (although the discrepancies are quite minor in the grander scheme of things).

- 10-Year gilts underperform vs. Bunds, spread 1bp wider on the day at ~202bp.

- Futures +18 at 90.72.

- Bears remain in technical control, initial support and resistance located at 90.26 & 91.08, respectively.

- Yields 1bp higher to 1bp lower, 2s10s ~5bp off September closing lows, while 5s30s is ~2bp off its September closing low.

- The GBP5bln auction of the new 4.00% May-29 gilt passed smoothly enough, with the cover ratio comparable to the recent averages of auctions of surrounding lines and a sub-1bp tail generated.

- GBP STIRs little changed on the day, showing ~5bp of easing through year-end. We continue to believe that markets are underestimating the chances of a Q4 rate cut.

- Comments from BoE chief economist Pill are due this afternoon (16:00 London).

- Pill will speak at the Maxwell Fry Annual Lecture at the University of Birmingham. We do not know the subject of the address.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Nov-25 | 3.959 | -0.8 |

Dec-25 | 3.920 | -4.7 |

Feb-26 | 3.816 | -15.2 |

Mar-26 | 3.785 | -18.2 |

Apr-26 | 3.710 | -25.7 |

Jun-26 | 3.687 | -28.0 |

Jul-26 | 3.639 | -32.8 |

Sep-26 | 3.628 | -33.9 |

EQUITIES: E-Mini Trend Condition Unchanged, Direction Remains Upward

Eurostoxx 50 futures remain in a bull-mode condition. Last week’s gains resulted in a breach of key resistance at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend. The impulsive climb opens the 5700.00 handle next, with potential for a test of 5727.18 further out, a Fibonacci projection. Moving average studies are in a bull-mode position too, highlighting a dominant uptrend. Initial firm support is 5525.00, Aug 22 high. The trend condition in S&P E-Minis is unchanged and the direction remains up. Recent fresh cycle highs confirm a continuation of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6812.29, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6700.59. It has recently been pierced, a clear break of it would signal scope for a deeper pullback.

- Japan's NIKKEI closed lower by 215.89 pts or -0.45% at 47734.99 and the TOPIX ended 7.75 pts higher or +0.24% at 3235.66.

- Across Europe, Germany's DAX trades higher by 66.25 pts or +0.27% at 24450.78, FTSE 100 higher by 31.2 pts or +0.33% at 9514.7, CAC 40 up 47.93 pts or +0.6% at 8021.8 and Euro Stoxx 50 up 16.29 pts or +0.29% at 5629.91.

- Dow Jones mini up 70 pts or +0.15% at 46922, S&P 500 mini up 12.25 pts or +0.18% at 6773.75, NASDAQ mini up 66.75 pts or +0.27% at 25106.75.

Time: 10:00 BST

COMMODITIES: Correction Off Recent Lows for WTI Futures Considered Corrective

WTI futures have recovered from the most recent low print - a correction. A bearish theme remains intact. Last week’s sell-off resulted in a move through key support and the bear trigger at $60.85, the Aug 13 low. Clearance of this level strengthens the bear threat and paves the way for an extension towards $57.50, the May 30 low. Initial firm resistance has been defined at $66.42, the Sep 29 high. Clearance of this level would highlight a reversal. A bull cycle in Gold remains in play and this week’s breach of $40000.0 reinforces the uptrend. The move higher maintains the price sequence of higher highs and higher lows. Furthermore, momentum studies highlight a condition known as momentum drag - where momentum remains in overbought territory and moves sideways - a bullish signal. Sights are on $4074.54, a Fibonacci projection. Support to watch is $3775.3, 20-day EMA.

- WTI Crude up $0.58 or +0.94% at $62.31

- Natural Gas up $0.03 or +0.8% at $3.526

- Gold spot up $53.38 or +1.34% at $4037.47

- Copper up $2.2 or +0.43% at $511.85

- Silver up $0.95 or +1.99% at $48.7596

- Platinum up $18.75 or +1.15% at $1645.77

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 08/10/2025 | 1030/1230 | ECB Elderson In Panel at Finance Conference | ||

| 08/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 08/10/2025 | 1320/0920 | St. Louis Fed's Alberto Musalem | ||

| 08/10/2025 | 1330/0930 | Fed Governor Michael Barr | ||

| 08/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 08/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 08/10/2025 | 1500/1600 | BOE Pill Speech at University of Birmingham | ||

| 08/10/2025 | 1600/1800 | ECB Lagarde Video Message at Werner Report Event | ||

| 08/10/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 08/10/2025 | 1800/1400 | *** | FOMC Minutes | |

| 08/10/2025 | 1915/1515 | Minneapolis Fed's Neel Kashkari | ||

| 08/10/2025 | 2145/1745 | Fed Governor Michael Barr | ||

| 09/10/2025 | 0600/0800 | ** | Trade Balance | |

| 09/10/2025 | 0830/0930 | BOE Mann Keynote at Resolution Foundation Event | ||

| 09/10/2025 | 1145/0745 | BOC Sr Deputy Gov Rogers speaks in Toronto (time TBC) | ||

| 09/10/2025 | - | ECB Lagarde & Cipollone at Eurogroup Meeting | ||

| 09/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 09/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 09/10/2025 | 1230/0830 | Fed Chair Jerome Powell | ||

| 09/10/2025 | 1245/0845 | Fed's Miki Bowman | ||

| 09/10/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 09/10/2025 | 1500/1700 | ECB Lane Round Table at Irish Investment Managers Event | ||

| 09/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 09/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 09/10/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 09/10/2025 | 1645/1245 | Fed Governor Michael Barr | ||

| 09/10/2025 | 1700/1300 | Minneapolis Fed's Neel Kashkari | ||

| 09/10/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 09/10/2025 | 1945/1545 | Fed's Miki Bowman |

Note: Due to U.S. government shutdown, some data may be unavailable.