EQUITIES: E-Mini Trend Condition Unchanged, Direction Remains Upward

Eurostoxx 50 futures remain in a bull-mode condition. Last week’s gains resulted in a breach of key resistance at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend. The impulsive climb opens the 5700.00 handle next, with potential for a test of 5727.18 further out, a Fibonacci projection. Moving average studies are in a bull-mode position too, highlighting a dominant uptrend. Initial firm support is 5525.00, Aug 22 high. The trend condition in S&P E-Minis is unchanged and the direction remains up. Recent fresh cycle highs confirm a continuation of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6812.29, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6700.59. It has recently been pierced, a clear break of it would signal scope for a deeper pullback.

- Japan's NIKKEI closed lower by 215.89 pts or -0.45% at 47734.99 and the TOPIX ended 7.75 pts higher or +0.24% at 3235.66.

- Across Europe, Germany's DAX trades higher by 66.25 pts or +0.27% at 24450.78, FTSE 100 higher by 31.2 pts or +0.33% at 9514.7, CAC 40 up 47.93 pts or +0.6% at 8021.8 and Euro Stoxx 50 up 16.29 pts or +0.29% at 5629.91.

- Dow Jones mini up 70 pts or +0.15% at 46922, S&P 500 mini up 12.25 pts or +0.18% at 6773.75, NASDAQ mini up 66.75 pts or +0.27% at 25106.75.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA OPTIONS: SFIM6 Call Buyer, Targeting 3-4 BOE Cuts Across Next 12m

SFIM6 97.25 calls, bought for 2.0 in 2.5k.

- SFIM6 currently trades at 96.405.

- This trade is targeting almost five BOE cuts across the next 12 months, compared to futures which currently price between one and two 25bp cuts.

- A reminder that following the weak KPMG-REC jobs report overnight, we conclude that the probability of a November 25bp cut is increased a little, with it following the DMP survey last week to be another downbeat labour result.

- However, we still need to see continued deterioration in the official labour market statistics and other labour surveys ahead of the November decision (including Agents' survey). And importantly, any earlier indications regarding pay settlements for 2026 will be key to the decision, too.

SWEDEN: More Tax Cuts Proposed For Autumn Budget

Headlines from Finance Minister Svantesson's ongoing press conference:

- "*SWEDISH GOVERNMENT PROPOSES REDUCTION TO TAX ON EARNED INCOME"

- "*SWEDISH GOVERNMENT PROPOSES CUT TO PENSION TAX AHEAD OF BUDGET"

- "*SWEDISH GOVERNMENT PROPOSES CUT TO TAX ON ELECTRICITY BILLS"

Follows last week's announcement for a temporary halving of food VAT to 6% from April 2026.

These policies form part of the SEK80bln of expansionary measures announced at the end of the August, set to be formally presented at the Autumn budget on September 22.

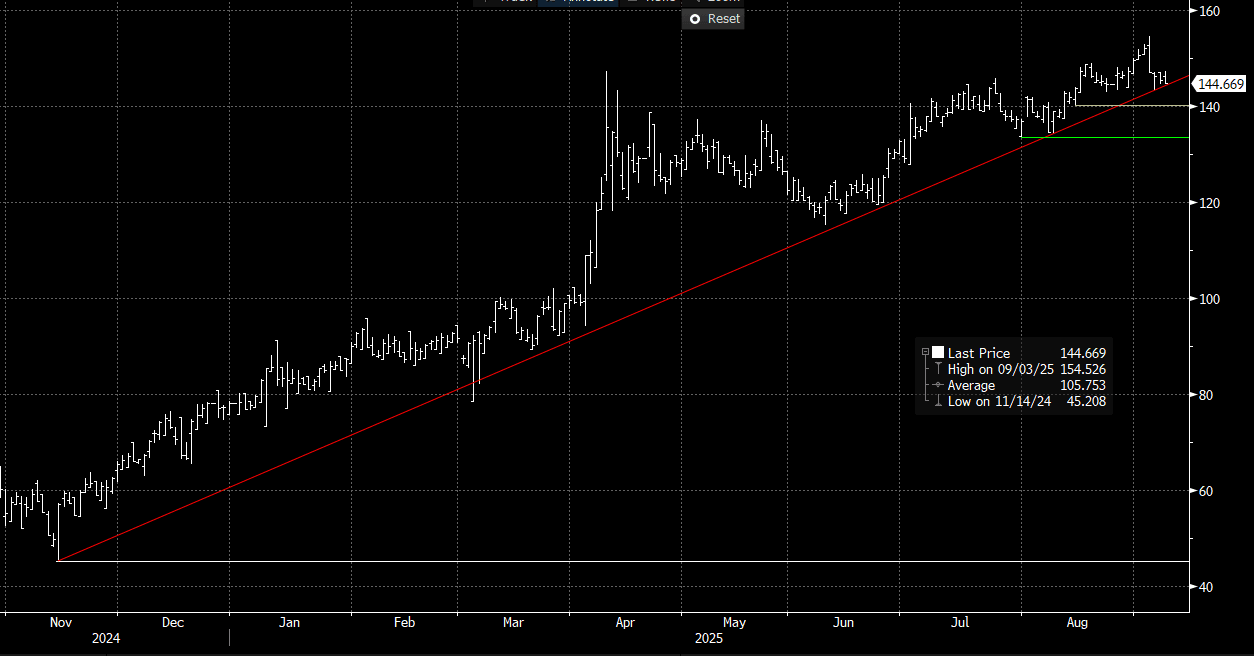

GILTS: Steady Start For Futures; 5s30s Testing Trendline Support

Uneventful start to the week for Gilt futures, currently +7 ticks at 91.30 with volumes running below recent averages for this time of day. Last week’s rally has highlighted a stronger technical corrective cycle, with the move higher also allowing an oversold trend condition to unwind. Friday’s high was pierced at the open, exposing 91.45 as the next upside target (Aug 15 high).

- The UK curve has lightly bull flattened, with 2/5-year yields little changed and 30-year yields around 0.5bps lower.

- 5s30s is 0.7bps lower at 144.7bps, extending the run of relief flattening that began last Wednesday. The spread is currently hovering around trendline support drawn from the November 2024 low. A clear breach of this support would leave scope for a retracement back towards ~140bps (Aug 14 low).

- 10-year yields are little changed at 4.643%, now 20bps below last Wednesday’s 4.845% high.

- A reminder that the KPMG-REC jobs report released overnight was weak, but had little market impact. The BRC shop sales monitor is released overnight, with monthly activity data for July due on Friday. Most data interest remains on next week’s labour market and inflation data.

- This week, Gilts will likely take cues from global core FI moves, with some focus reserved for political headline flow following Starmer’s reshuffle last Friday.

Figure 1: UK 5s30s Curve (Source: Bloomberg Finance L.P)