MNI US OPEN - PMIs Creep Higher in UK, France & Germany

EXECUTIVE SUMMARY

- MNI 2025 JACKSON HOLE PREVIEW

- FED’S COOK SAYS SHE WON’T BE BULLIED INTO STEPPING DOWN

- EUROZONE FLASH PMI SHOW SIGNS OF TARIFFS REDUCING EXPORT VOLUMES

- ZELENSKIY RULES OUT CHINA AS ONE OF POSTWAR SECURITY GUARANTORS

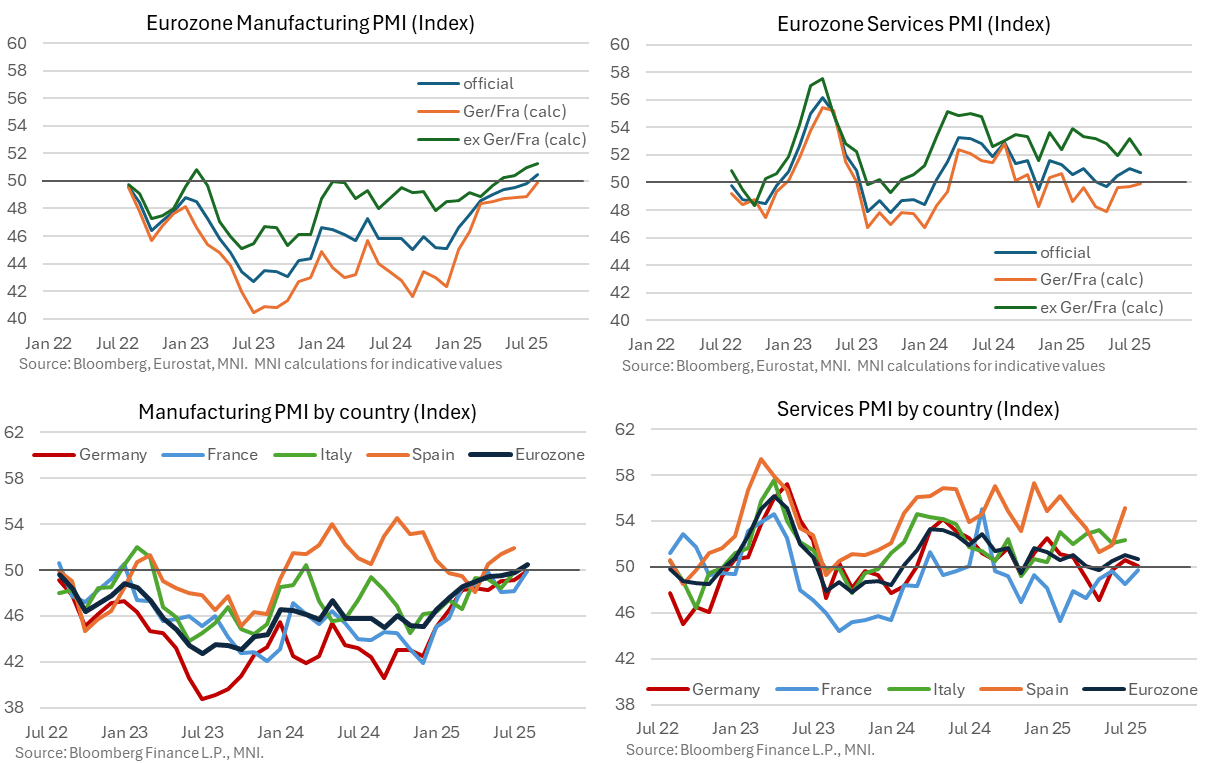

Figure 1: Eurozone manufacturing PMI stronger-than-expected and services broadly in line

NEWS

The key event at the annual Jackson Hole Economic Policy Symposium (Aug 21-23) is Chair Powell's speech on Friday (1000ET/1500UK). Attention will of course mostly be on any nod Powell makes to a potential September Fed rate cut, a prospect which we discuss in this preview. MNI's Markets Team believes that in contrast to Jackson Hole 2024, Powell will avoid an overtly dovish nod at this meeting, given how split the Committee appears to be on the need to cut rates.

FED (BBG): Fed’s Cook Says She Won’t Be Bullied Into Stepping Down

Federal Reserve Governor Lisa Cook signaled her intention to remain at the central bank, defying calls for her resignation by President Donald Trump over allegations of mortgage fraud. “I have no intention of being bullied to step down from my position because of some questions raised in a tweet,” Cook said in an emailed statement via a Fed spokesperson. “I do intend to take any questions about my financial history seriously as a member of the Federal Reserve and so I am gathering the accurate information to answer any legitimate questions and provide the facts.”

US/EU (MNI EXCLUSIVE): EU-US Joint Trade Statement Seen Lacking Key Detail

The prospects for an EU-US joint statement on trade are becoming clearer. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

UKRAINE (BBG): Zelenskiy Rules Out China as One of Postwar Security Guarantors

Ukrainian president Volodymyr Zelenskiy pushed back against Russia’s idea to add China as a security guarantor in the event of a ceasefire. “We don’t need guarantors who don’t help Ukraine, and didn’t help Ukraine at the moment when we really needed it,” Zelenskiy told reporters in Kyiv. “We need security guarantees only from those countries that are ready to help us.”

INDIA (BBG): Modi Tax Cut to Spark Tough Talks With Cash-Strapped States

Indian Prime Minister Narendra Modi will likely face tough negotiations with states, who are expected to shoulder the bulk of revenue losses from his surprise move to lower consumption taxes within three months. Modi proposed a major rejig of the complex goods and services tax last week, a move many businesses had been pushing for since the system was rolled out in 2017. Stocks rallied as investors bet lower taxes on everyday goods would boost consumer spending and help offset the drag on economic growth from higher US tariffs.

THAILAND (MNI): Lawfare Against Shinawatras Fuels Political Instability

A series of three high-profile court cases scheduled to take place in quick succession over the next few weeks represents a critical juncture in Thailand’s political cycle. A decline in popular support for the ruling Pheu Thai Party (PTP) and its leaders deprive them of their traditional advantage ahead of the looming legal ordeal. Unfavourable verdicts against key members of the powerful Shinawatra clan could exacerbate headwinds for the beleaguered PTP administration.

CORPORATE (WSJ): Meta Freezes AI Hiring After Blockbuster Spending Spree

Meta Platforms has frozen hiring in its artificial-intelligence division after spending months scooping up 50-plus AI researchers and engineers, according to people familiar with the matter. The hiring freeze, which went into effect last week and coincides with a broader restructuring of the group, also prohibits current employees from moving across teams inside the division. The duration of the freeze wasn’t communicated internally.

DATA

EUROZONE DATA (MNI): Signs of Tariffs Reducing Export Volumes

- EUROZONE AUG FLASH MANUF PMI 50.5 (49.5 FCAST, 49.8 JUL)

Unsurprising developments the Eurozone-wide August flash PMI following the French and German releases earlier, with manufacturing stronger-than-expected at 50.5 (vs 49.5 cons, 49.8 prior) and services broadly in line at 50.7 (vs 50.8 cons, 51.0 prior). That helped the composite reading rise to a 15-month high of 51.1 (vs 50.9 prior).

EUROZONE JUN CONSTRUCTION OUTPUT -0.8% M/M, +1.7% Y/Y (MNI)

GERMANY DATA (MNI): Manufacturing Flash PMI Stronger Than Expected

- GERMANY AUG FLASH MANUF PMI 49.9 (48.8 FCAST, 49.1 JUL)

Similar to France, the German flash August manufacturing PMI was stronger than expected, albeit still just below the neutral 50 level. Manufacturing was 49.9 (vs 48.8 cons, 49.1 prior) - a 38-month high. Services was a touch weaker-than-expected at 50.1 (vs 50.3 cons, 50.6 prior), but the manufacturing reading still reading helped the composite index rise to 50.9 (vs 50.2 cons, 50.6 prior). Overall, the manufacturing sector continues to exhibit relative resilience despite tariff impositions and trade policy uncertainty. Weaker oil prices and a stronger exchange rate have likely contained input cost pressures.

FRANCE DATA (MNI): Stronger Than Expected PMIs Though Some Signs of Weakness Remain

- FRANCE AUG FLASH MANUF PMI 49.9 (48.1 FCAST, 48.2 JUL)

Stronger than expected set of French August flash PMIs, with both the manufacturing (49.9 vs 48.1 cons, 48.2 prior) and services (49.7 vs 48.5 cons, 48.5 prior) above consensus and just below the neutral 50 handle. The composite reading was 49.8 (vs 48.6 prior). It has not printed in expansionary territory since August 2024. Although a step in the right direction, there are still elements of demand weakness in the print, and continued political uncertainty is probably weighing on 12-month ahead expectations.

UK DATA (MNI): Falling Backlogs of Work and Employment, Rising Input Costs

- UK AUG FLASH MANUF PMI 47.3 (48.3 FCAST, 48.0 JUL)

Highlights from the PMI press release focus on strong new business volumes but not enough high enough to stop backlogs of work falling while input costs are increasing and employment continuing to decline. With the BOE focused on inflation expectations, the reports of higher food costs in here will be concerning to the MPC: "New business volumes expanded at the strongest pace since October 2024."

UK DATA (MNI): Public Finance Data Balanced Out by Revisions

- UK JUL PSNB GBP+1.05 BN

- UK JUL PSNB-X GBP+1.05 BN

- UK JUL PSNCR GBP3 BN

- UK JUL CGNCR GBP6.18 BN

Public finance data looks a little better than both consensus and OBR forecasts for the month of July with PSNBex GBP1.1bln on the month (consensus GBP2.0bln). However, this is entirely balanced out by a GBP1.1bln revision tothe cumulative Apr-Jun numbers. All in all, at first glance the accrual based numbers therefore don't seem to move the needle much. The date of the Budget has still not been set (November looking likely) and we are likely to get at least one and an outside chance of two more updates incorporated in OBR forecasts before then (and likely 3 updates seen by the market).

NORWAY DATA (MNI): Mainland Investment Drives Q2 Beat; Hawkish Signals for Norges

The Q2 mainland GDP beat (0.6% Q/Q vs 0.3% Norges Bank and consensus) was driven by higher-than-expected business and residential investment. Notably, Q2 mainland GDP growth was 0.9% Q/Q when excluding volatile industries like fishing and electric power growth. This adds to the hawkish message from the print in our view. Alongside this GDP report, the Q3 Regional Network Survey will be key in determining what contribution domestic demand makes to the September MPR rate path projection.

NORWAY DATA (MNI): Firm Q2 Wage Growth Adds Another Hawkish Element to Report

Norwegian wage growth was firm in Q2 according to National Accounts data, providing another hawkish element for Norges Bank to consider. However, this was offset a little by another sequential increase in mainland real productivity growth. Wages and salaries per employee rose 5.77% Y/Y (vs 5.25% in Q1), with 4Q/4Q growth ticking up to 5.83% (vs 5.75% prior). Meanwhile, compensation per employee growth was 5.27% Y/Y (vs 5.25% prior) and 5.43% 4Q/4Q (vs 5.63% prior).

JAPAN DATA (MNI): August Manufacturing PMI Rises But Still Sub 50.0

Japan preliminary PMIs for August were mixed. Manufacturing improved to 49.9 from 48.9, but services eased to 52.7 from 53.6. This left the composite index slightly higher at 51.9 (versus 51.6 in July). The manufacturing index is up from March lows (just under 48.5), but hasn't yet re-captured the expansion point. The index has spent little time above 50.0 in recent years. In terms of the detail, output rose to 50.5 from 47.6, while new orders were also up on July levels.

AUSTRALIA DATA (MNI): PMI Suggests H2 Pickup in Growth

The S&P Global PMI is suggesting that growth picked up in Australia in Q3. The preliminary August composite index rose to 54.9 from 53.8 driven by improvements in both the manufacturing and services sectors as well as higher new orders, including external, and increased hiring to fill them. This is the fastest growth in activity since April 2022, before the RBA began its tightening cycle. The PMI suggests that while Q2 growth could again be lacklustre there was probably an improvement in H2.

AUSTRALIA DATA (MNI): Inflation Expectations Back Below 4%

In June, Melbourne Institute consumer inflation expectations jumped 1pp to 5%. They moderated to 4.7% in July and in August to 3.9%, the first print below 4% since March's 3.6%. Looking at the trend, the series has been moving sideways for around the last year. It is still too soon to say that inflation expectations are drifting down again with the next few months key in determining that. However, the August moderation in addition to S&P Global reporting an easing in the pace of output price inflation to just above the historical average are likely to reassure the RBA that inflation is sustainably within the target band.

NEW ZEALAND DATA (MNI): First Trade Deficit Since January

After five consecutive merchandise trade surpluses, NZ recorded a deficit in July of $578mn bringing the 12mth sum to $3.94bn down from $4.38bn. Export growth remains strong, which has been a bright spot in a soft economy. Goods exports rose 10% y/y in July with dairy products rising 17% y/y. The sector was helped by higher prices but also increased volumes for milk powder and butter. Beef exports rose 17% y/y with strong increases to the US and Canada but declining to China.

FOREX: JPY Softer Despite Futures Pointing to Lower Wall Street Open

- JPY is sliding against all others in G10, despite core equity markets remain weaker. US futures point to a lower open on Wall Street later today, extending the soft close from the Wednesday session. Pre-setting and positioning ahead of Powell's appearance at Jackson Hole remains the dominant theme, although weekly claims data and prelim PMI stats will also be carefully watched. Fed's Bostic is also set to speak, talking on the economy at 1230BST/0730ET.

- Prelim PMI numbers from across Europe provided the primary market impetus Thursday, with stronger numbers from France, Germany and the UK providing a boost for EUR and GBP. EUR/USD remains locked to the uptrend as dictated by the 50-dma (today at 1.1646). The trend structure remains bullish highlighted by moving average studies that are in a bull-mode position. A resumption of gains would expose key resistance and the bull trigger at 1.1829, the Jul 1 high. Clearance of this level would resume the uptrend.

- Meanwhile, EURNOK has moved away from session lows of 11.8631 but remains 0.4% lower on the session at 11.8821. The combination of a solid Q2 GDP report and further strength in crude oil/natural gas prices has provided support to the krone intraday, while the dovish leaning Norges Bank expectations survey may have provided some offset. The pullback in EURNOK from Tuesday's highs is considered corrective for now, with moving average studies still in a bull-mode setup. While the cross has pierced the 20-day EMA of 11.8967, the August 12 low at 11.8667 has contained intraday downside for now. Key support is seen at the 50-day EMA of 11.8298.

EGBS: German Curve Bear Flattens Following PMIs

The German curve has bear flattened after the Eurozone August flash composite PMI was stronger-than-expected, driven by the manufacturing sector. 2-year yields are up 2.5bps to 1.96%, while 30-year yields are little changed at 3.29%. The 5s30s curve is hovering just below the 100bps level, off Tuesday’s 103bp high.

- Bund futures after – 12 ticks at 129.34, off post-French PMI lows of 129.14. The PMIs have contributed to some early volatility, but a technical bear threat remains present. Firm support is seen at the August 15 low of 128.64, with immediate support at the 129.00 figure.

- The Eurozone flash PMI saw manufacturing stronger-than-expected at 50.5 (vs 49.5 cons, 49.8 prior) and services broadly in line at 50.7 (vs 50.8 cons, 51.0 prior). That helped the composite reading rise to a 15-month high of 51.1 (vs 50.9 prior).

- Overall, the data underscores the ECB’s view that policy is in a “good place”, but isn’t enough to significantly dampen expectations for one more 25bp cut this cycle.

- MT OAT supply was digested smoothly, with the sale concentrated towards the on-the-run lines. French linker supply is due later this morning.

- 10-year EGB spreads to Bunds are little changed from yesterday’s close.

- Global focus turns to this afternoon’s US data, before the Fed’s Jackson Hole Symposium kicks off this evening.

GILTS: Bear Flattening on Local & Eurozone PMIs

Gilts trade just above session lows.

- An opening rally was quickly sold into.

- Firmer-than-expected Eurozone & UK PMIs have weighed at different stages, with some offset provided by a downtick in core global equity futures.

- Futures traded as high as 91.22 before fading to 90.82.

- The bearish technical theme remains intact in the contract. Initial support and resistance located at 90.43 & 91.32, respectively.

- Yields 2.5-3.5bp higher across the curve, light flattening.

- Gilts ~1.5bp wider vs. Bunds after yesterday’s outperformance. 10-Year spread out to 197bp, any moves above 200bp have lacked conviction in recent sessions.

- The latest round of monthly public finance data looked a little better than both consensus and OBR forecasts. However, this was countered by revisions to the Apr-Jun data.

- Speculation surrounding the form that further fiscal tightening will take remains evident. Telegraph sources reported that Chancellor Reeves is to “consider cutting the tax-free pension lump sum in a move that would be expected to raise more than £2bn a year”.

- Note that the details of today’s flash PMI data pointed to a stagflationary backdrop, noting falling backlogs of work and employment, alongside rising input costs.

- SONIA futures flat to -4.5 given moves in the long end.

- BoE-dated OIS little changed to 2.5bp less dovish through ’25 meetings, showing ~10bp cuts through Dec.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Sep-25 | 3.975 | +0.8 |

Nov-25 | 3.911 | -5.6 |

Dec-25 | 3.870 | -9.7 |

Feb-26 | 3.774 | -19.4 |

Mar-26 | 3.736 | -23.2 |

Apr-26 | 3.665 | -30.2 |

EQUITIES: Recent Cycle Highs for Eurostoxx 50 Futures Strengthens Bull Theme

The trend set-up in Eurostoxx 50 futures is unchanged, it remains bullish and the contract traded to a fresh short-term cycle high on Tuesday. The recent print above the May and July highs strengthens a bull theme and signals scope for a climb towards 5575.00, the Mar 3 high (cont) and key resistance. Moving average studies remain in a bull-mode position, highlighting an uptrend. Support to watch lies at 5360.68, the 50-day EMA. The dominant uptrend in S&P E-Minis remains intact and the latest shallow retracement appears to be a correction. Moving average studies remain in a bull-mode position, highlighting a clear uptrend, and positive market sentiment. A resumption of gains would pave the way for a climb towards 6523.63, a Fibonacci projection. On the downside, supports to watch are; 6403.75, the 20-day EMA, and 6287.15, the 50-day EMA.

- Japan's NIKKEI closed lower by 278.38 pts or -0.65% at 42610.17 and the TOPIX ended 15.96 pts lower or -0.52% at 3082.95.

- Elsewhere, in China the SHANGHAI closed higher by 4.889 pts or +0.13% at 3771.099 and the HANG SENG ended 61.33 pts lower or -0.24% at 25104.61.

- Across Europe, Germany's DAX trades lower by 15.91 pts or -0.07% at 24260.97, FTSE 100 lower by 0.02 pts or 0% at 9288.15, CAC 40 down 30.24 pts or -0.38% at 7942.79 and Euro Stoxx 50 down 14.46 pts or -0.26% at 5457.86.

- Dow Jones mini down 102 pts or -0.23% at 44894, S&P 500 mini down 5.25 pts or -0.08% at 6408, NASDAQ mini up 2.25 pts or +0.01% at 23325.

Time: 10:00 BST

COMMODITIES: WTI Futures Recover From Lows But Bearish Theme Intact

A bear cycle in WTI futures remains intact and the contract continues to trade closer to its recent lows. A key support at $61.29, the Jun 30 low, has been breached, strengthening a bearish theme. A continuation lower would open $57.71, the May 30 low. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $63.86, the 50-day EMA. Despite the latest pullback - a correction - a bull cycle in Gold remains intact. Moving average studies are in a bull-mode position. The sideways trend that has been in place since the Apr peak appears to be a medium-term pause in the uptrend. A resumption of gains would open $3439.0, the Aug 23 high. Key resistance and the bull trigger is at $3500.1, the Apr 22 low. On the downside, first support to watch lies at $3268.2, the Jul 30 low.

- WTI Crude up $0.53 or +0.85% at $63.27

- Natural Gas up $0.01 or +0.29% at $2.761

- Gold spot down $9.91 or -0.3% at $3339.22

- Copper down $1.85 or -0.41% at $449.15

- Silver down $0.1 or -0.27% at $37.8115

- Platinum down $10.73 or -0.8% at $1327.81

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 21/08/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 21/08/2025 | 1130/0730 | Atlanta Fed's Raphael Bostic | ||

| 21/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 21/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 21/08/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 21/08/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 21/08/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 21/08/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 21/08/2025 | 1400/1000 | *** | NAR existing home sales | |

| 21/08/2025 | 1400/1000 | * | Services Revenues | |

| 21/08/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 21/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 21/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 21/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 21/08/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 30 Year Bond | |

| 22/08/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 22/08/2025 | 2330/0830 | *** | CPI | |

| 22/08/2025 | 0600/0800 | ** | Unemployment | |

| 22/08/2025 | 0600/0800 | *** | GDP (f) | |

| 22/08/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 22/08/2025 | 0900/1100 | Q2 Negotiated Wage Growth | ||

| 22/08/2025 | 1230/0830 | ** | Retail Trade | |

| 22/08/2025 | 1400/1000 | Fed Chair Jerome Powell | ||

| 22/08/2025 | 1400/1000 | *** | US Fed Chair Speech | |

| 22/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |