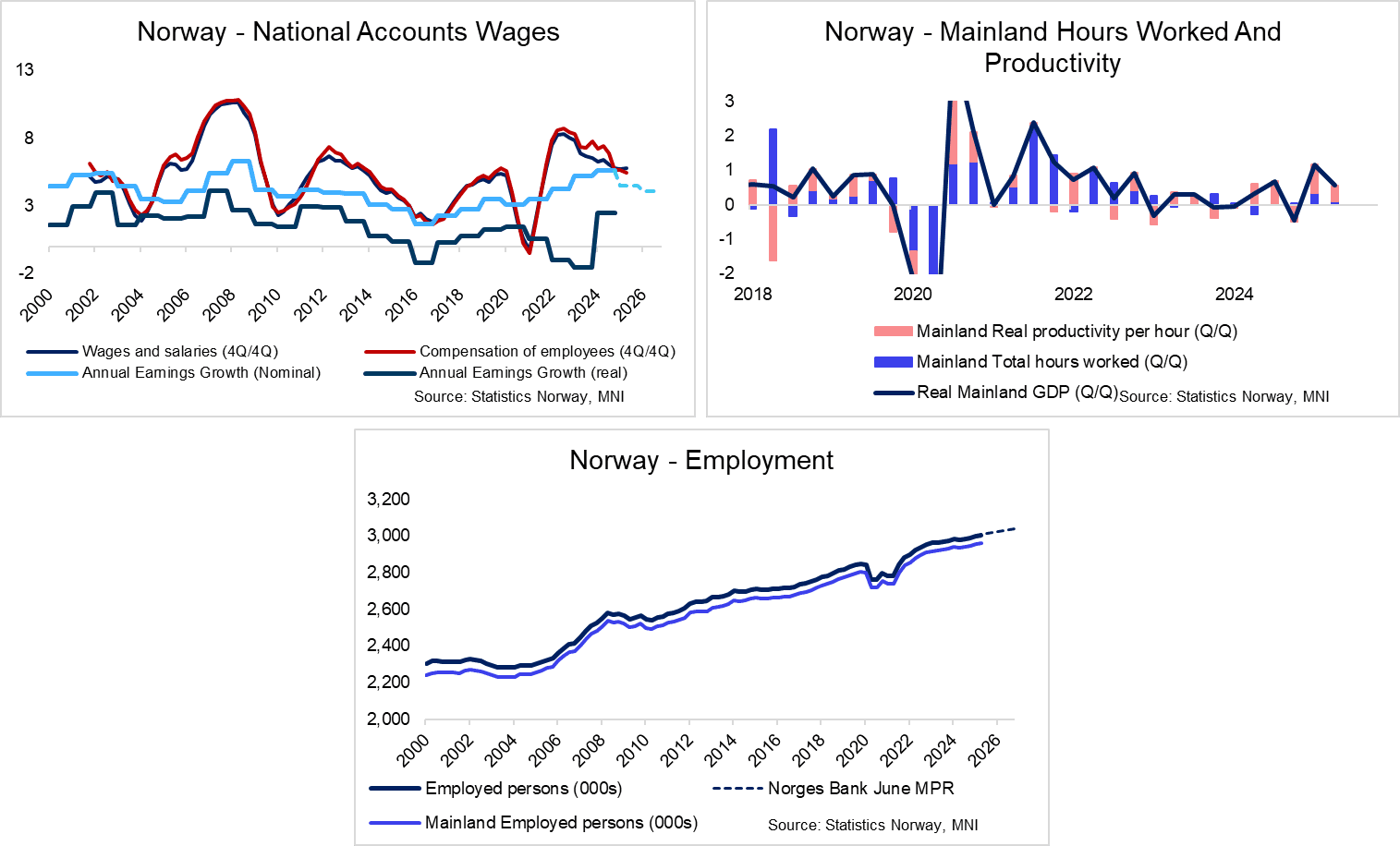

NORWAY: Firm Q2 Wage Growth Adds Another Hawkish Element To Report

Norwegian wage growth was firm in Q2 according to National Accounts data, providing another hawkish element for Norges Bank to consider. However, this was offset a little by another sequential increase in mainland real productivity growth.

- Wages and salaries per employee rose 5.77% Y/Y (vs 5.25% in Q1), with 4Q/4Q growth ticking up to 5.83% (vs 5.75% prior). Meanwhile, compensation per employee growth was 5.27% Y/Y (vs 5.25% prior) and 5.43% 4Q/4Q (vs 5.63% prior).

- Norges Bank forecast annual nominal earnings growth (which is less volatile than the two measures noted above) at 4.5% in 2025, in line with the Q2 Regional Network Survey.

- It seems wage deceleration will need to gather pace in H2 for this forecast to be realised, though there’s still some uncertainty here.

- Overall and mainland employment growth were in line with Norges Bank projections in Q2, rising 0.2% Q/Q (vs 0.4% prior). This was in line with the signal from the Q2 Regional Network Survey. Meanwhile, hours worked rose 0.1% Q/Q (vs 0.4% prior).

- This meant mainland real productivity per hour worked rose 0.5% Q/Q, building on Q1’s 0.8% reading.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: European Cash Markets Seen Opening Lower, Mimicking US

Headed into the cash open, European futures are lower by ~0.4% to mimic the late pullback in US markets into the Monday cash close. The Eurostoxx50 future is lower by 20 points at typing, but is already off lows to steer clear of any test on 5303.00 support and trend support into the 5286.9 100-dma.

- US earnings season really picks up today: Coca-Cola, RTX, Danaher, Texas Instruments, Chubb, Lockheed Martin, Capital One Financial, Intuitive Surgical and Philip Morris are among many set to report.

STIR: SONIA Lightly Underperforms Euribor Following UK Fiscal Data

SONIA futures are flat to to -2.0 ticks through the blues, slightly underperforming Euribor counterparts (flat to -1.5 ticks) following this morning’s higher-than-expected PSNB reading for June.

- BOE-dated OIS still essentially fully price a 25bp BOE cut in August, with almost 50bps of easing priced through year-end.

- BOE Governor Bailey is scheduled to testify on Financial Stability at the TSC today (1015BST). However, any comments around the labour market will be in focus, following last week’s data and his recent dovish interview with the Times.

- For the ECB, there remains uncertainty as to whether another 25bp cut will be delivered at the September or December macroeconomic projection meeting. No rate action is expected at Thursday’s decision - MNI’s full preview for that event will be out later today.

- The ECB's Q2 Bank Lending Survey at 0900BST will provide an important update on credit demand and lending standards across the region. It is a closely watched survey by ECB Governing Council members. In a recent hawkish interview, Executive Board member Schnabel referenced the Q1 survey's results as rationale for her view that policy is becoming accommodative (even if her view is considered a minority amongst the rest of the Board).

- It will be interesting to see if the BLS echoes the broad strokes of more regular and timely lending data. After displaying signs of plateauing through the first four months of 2025, the Eurozone credit impulse metric of 3mth flows vs 3mths a year ago fell four tenths to 1.5% of GDP in May, the lowest since December. Yesterday’s SAFE survey suggested rate cuts are continuing to feed through into lending conditions and demand. However, near term prospects for business activity remain subdued.

JPY: USD/JPY Briefly Prints a New High on BoJ Sources

"*BOJ IS SAID LIKELY TO LEAVE BENCHMARK RATE UNCHANGED NEXT WEEK" - bbg

"*BOJ IS SAID TO SEE LITTLE IMPACT FROM ELECTION ON RATE STANCE"

"*BOJ TO WATCH IMPACT OF TRADE TALKS BEFORE ANY HIKE, PEOPLE SAY"

"*BOJ IS SAID TO SEE UPWARD PRICE RISK IF BIG FISCAL LOOSENING"

- Some relief goes through in USD/JPY on that headline - pair prints a new daily high of Y147.93 (thereby topping the 50% retracement mark of yesterday's range) before running out of steam.

- Much of this sentiment was already well-priced - with very little expectation of a move higher in BoJ rates next week and, as mentioned just above, Ishiba's likely to stay in office for the short-term to focus on trade negotiations, which also removes the risk of fiscal expansion for now.