EGBS: German Curve Bear Flattens Following PMIs

The German curve has bear flattened after the Eurozone August flash composite PMI was stronger-than-expected, driven by the manufacturing sector. 2-year yields are up 2.5bps to 1.96%, while 30-year yields are little changed at 3.29%. The 5s30s curve is hovering just below the 100bps level, off Tuesday’s 103bp high.

- Bund futures after – 12 ticks at 129.34, off post-French PMI lows of 129.14. The PMIs have contributed to some early volatility, but a technical bear threat remains present. Firm support is seen at the August 15 low of 128.64, with immediate support at the 129.00 figure.

- The Eurozone flash PMI saw manufacturing stronger-than-expected at 50.5 (vs 49.5 cons, 49.8 prior) and services broadly in line at 50.7 (vs 50.8 cons, 51.0 prior). That helped the composite reading rise to a 15-month high of 51.1 (vs 50.9 prior).

- Overall, the data underscores the ECB’s view that policy is in a “good place”, but isn’t enough to significantly dampen expectations for one more 25bp cut this cycle.

- MT OAT supply was digested smoothly, with the sale concentrated towards the on-the-run lines. French linker supply is due later this morning.

- 10-year EGB spreads to Bunds are little changed from yesterday’s close.

- Global focus turns to this afternoon’s US data, before the Fed’s Jackson Hole Symposium kicks off this evening.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOE: Bailey Sees UK Experience With Steeper Curve Part of Global Phenomenon

Bailey speaking on global curves and the UK experience:

- "BANK OF ENGLAND'S BAILEY: WE HAVE SEEN STEEPER YIELD CURVES, THAT IS GLOBAL PHENOMENON" - Reuters

- UK EXPERIENCE IS NOT OUT OF LINE WITH OTHER MARKETS

- CAUSE OF STEEPER YIELD CURVE REFLECTS GREATER UNCERTAINTY ON TRADE POLICY"

He's speaking in front of lawmakers on the BoE's financial stability report - unlikely to get much on monetary policy specifically - but any references to UK inflation or the jobs market will be watched carefully. Livestream here: https://www.parliamentlive.tv/Event/Index/e1eb2a6b-6c37-43d3-a69b-566e1b7a84ab

AUSTRIA T-BILL AUCTION RESULTS: 3/6-month ATB Results

| Type | 3-month ATB | 6-month ATB |

| Maturity | Oct 30, 2025 | Jan 29, 2026 |

| Allotted | E758mln | E852mln |

| Previous | E500mln | E779mln |

| Amount | E1bln | E1bln |

| Target | E1bln | E1bln |

| Previous | E500mln | E1bln |

| Avg yield | 1.935% | 1.900% |

| Previous | 1.860% | 1.960% |

| Bid-to-cover | 1.99x | 2.06x |

| Previous | 2.75x | 1.8x |

| Bid-to-offer | 1.51x | 1.76x |

| Previous | 2.75x | 1.4x |

| Previous date | Jun 24, 2025 | Apr 22, 2025 |

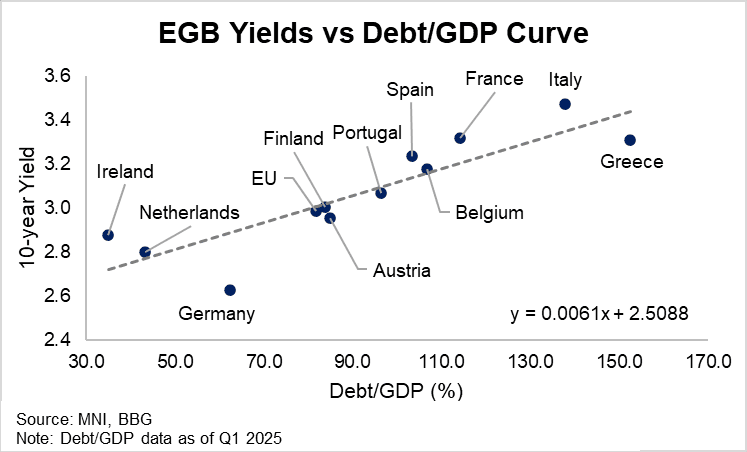

EGBS: Fiscal and Issuance Flow Supportive Of BTP/Obli Outperformance vs OATs

Incorporating yesterday’s Q1 Eurozone fiscal data, a simple chart of debt/GDP to 10-year yields crudely isolates Spanish, French and Italian bonds as cheap (i.e. trading above the linear line of best fit). While well documented French political and fiscal risks continue to warrant a yield premium for OATs, there may be scope for continued relative outperformance of Oblis and BTPs in the coming months.

- We wrote yesterday that while Italian interest expense growth exceeds that of nominal GDP, this is mitigated by the Government’s Q1 primary surplus of 0.4%. Meanwhile, strong Spanish real GDP growth post Covid has kept a healthy gap between interest expense growth and nominal GDP growth. Spain’s primary deficit also narrowed to 0.6% in Q1 from 0.7% in Q4. On the other hand, the difference between French interest expense growth and nominal GDP narrowed a notable 0.8pp to -0.7pp in Q1, a concerning development for the debt/GDP outlook given France's 3.6% primary deficit (despite ongoing attempts at fiscal consolidation).

- The outlook for net issuance also favours Italian and Spanish paper over France: We expect the mid-August Bono/Obli auction to be cancelled, while there is a sizeable E24bln Spanish redemption due on July 30. We also expect the mid-month 3/7/15-50-year BTP auction to be cancelled, with a E13bln BTP redemption then due on August 15. Meanwhile, we expect the two August OAT auctions to go ahead as planned, and there are no French redemptions due until October.

- Elsewhere, 10-year Bund yields trade rich to the debt/GDP curve owing to German paper’s haven/reserve status in the EGB space. Greece’s impressive fiscal consolidation continues to support GGBs, with 10-year yields currently trading just below OATs.