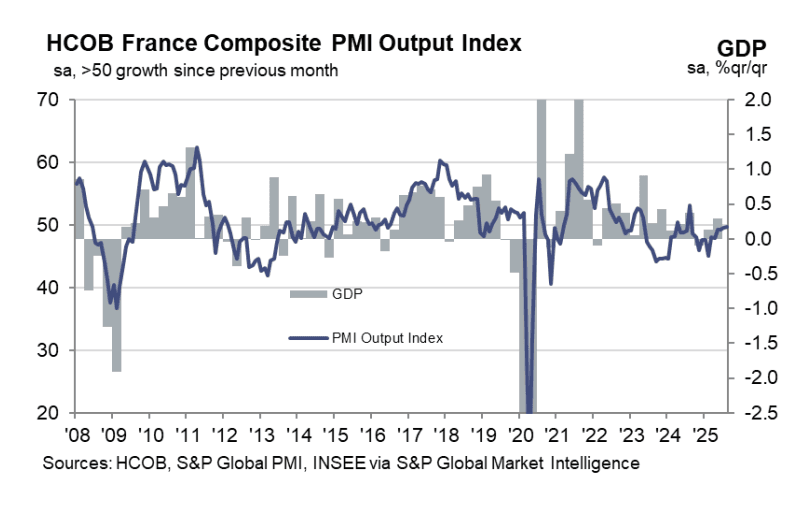

FRANCE DATA: Stronger Than Expected PMIs Though Some Signs Of Weakness Remain

Stronger than expected set of French August flash PMIs, with both the manufacturing (49.9 vs 48.1 cons, 48.2 prior) and services (49.7 vs 48.5 cons, 48.5 prior) above consensus and just below the neutral 50 handle. The composite reading was 49.8 (vs 48.6 prior). It has not printed in expansionary territory since August 2024.

- Although a step in the right direction, there are still elements of demand weakness in the print, and continued political uncertainty is probably weighing on 12-month ahead expectations.

- Also note that the French PMI has been more revision prone than Germany in recent months, so the flash print may need to be taken with some salt.

Highlights from the release:

- “While business activity was more-or-less stable in August, there remained evidence of demand weakness as total new order volumes decreased for a fifteenth successive month”.

- “While there were some mentions of reduced market activity abroad, particularly in the US, some companies did note a general pick-up in client interest. Indeed, August’s softer deterioration in overall demand was partly due to a reduced drag from international sources as new export business fell at a slower pace than in July”

- “For the first time since last November, private sector employment across France increased midway through the third quarter” … “Stronger hiring trends were seen across both monitored sectors”

- “Cost inflation picked up across both sectors, with panel members commenting on wage pressures and higher raw material prices”.

- “For a third month in a row, French private sector businesses raised their own charges. The extent to which selling prices rose also quickened, although the overall rate of output charge inflation was only marginal overall”.

- “Looking ahead to the next 12 months, French private sector firms were pessimistic on balance, marking the first time since November last year that this has been the case”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

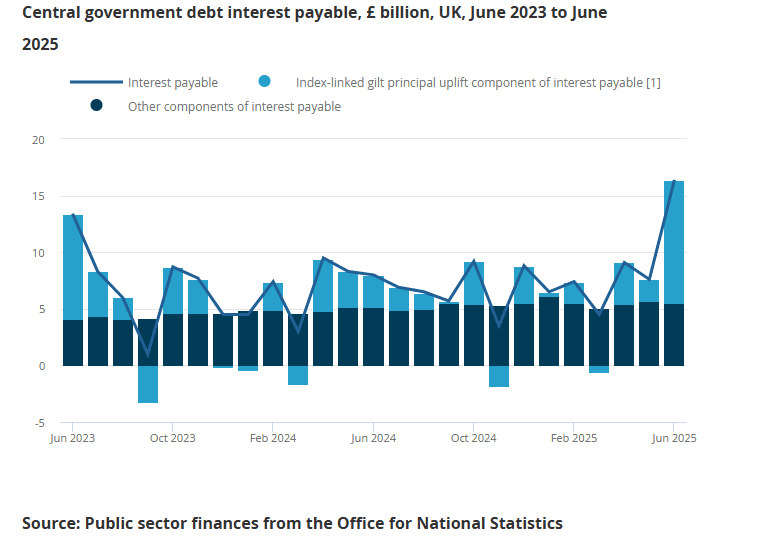

UK FISCAL: Higher Linker Interest Payments Push PSNB Higher In June

Looking a little more at this morning’s public sector finance data, the GBP20.7bln PSNB figure for June was GBP6.6bln more than June 2024 and “the second-highest June borrowing since monthly records began in 1993, after that of June 2020”, according to the ONS. The OBR projected a reading of GBP17.1bln in March 2025, with BBG consensus standing at GBP17.5bln.

- Central government current receipts were GBP5.7bln more than a year ago at GBP86.6bln. Following the change in employer NI contributions from April 2025, compulsory social contributions were up GBP3.1bln Y/Y to GBP17.4bln.

- Expenditures rose a more notable GBP12.4bln versus June 2024, totalling GBP97.1bln. This was largely due to a GBP8.4bln rise in interest payable to GBP16.4bln - GBP2.4bln above the OBR’s projection. There was a 1.7% rise in RPI between March-April 2025, which was reflected in increased linker interest payments in June (“capital uplift”).

SILVER TECHS: Bullish Price Sequence

- RES 4: $40.285 - 1.618 proj of the Apr 7 - 25 - May 15 swing

- RES 3: $40.000 - Psychological round number

- RES 2: $39.655 - 1.500 proj of the Apr 7 - 25 - May 15 swing

- RES 1: $39.132 - High Jul 14

- PRICE: $38.834 @ 08:07 BST Jul 22

- SUP 1: $37.271 - 20-day EMA

- SUP 2: $35.942 - 50-day EMA

- SUP 3: $33.967 - Low Jun 3

- SUP 4: $32.615 - Low May 22

Trend signals in Silver are unchanged and continue to point north. On Jul 11, Silver cleared a key short-term resistance at $37.317, the Jun 18 high. This confirmed a resumption of the uptrend. Note too that moving average studies are in a bull-mode position, highlighting a clear uptrend. Sights are on the $39.655 next, a Fibonacci projection. On the downside, initial support to watch lies at $37.271, the 20-day EMA.

USDCAD TECHS: Key Short-Term Resistance Intact For Now

- RES 4: 1.3920 High May 21

- RES 3: 1.3862 High May 29

- RES 2: 1.3798 High Jun 23

- RES 1: 1.3744/74 50-day EMA / High Jul 17

- PRICE: 1.3692 @ 08:04 BST Jul 22

- SUP 1: 1.3639/3557 Low Jul 08 / 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

Resistance in USDCAD at 1.3744, the 50-day EMA, remains intact for now. It has been pierced, however, a clear break of it is required to highlight a possible stronger short-term reversal. This would open 1.3798 initially, the Jun 23 high. For now, a bear trend remains in place. A resumption of weakness would refocus attention on key support at 1.3540, the Jun 16 low. Clearance of this level would confirm a resumption of the downtrend.