GILTS: Bear Flattening On Local & Eurozone PMIs

Aug-21 09:25

Gilts trade just above session lows.

- An opening rally was quickly sold into.

- Firmer-than-expected Eurozone & UK PMIs have weighed at different stages, with some offset provided by a downtick in core global equity futures.

- Futures traded as high as 91.22 before fading to 90.82.

- The bearish technical theme remains intact in the contract. Initial support and resistance located at 90.43 & 91.32, respectively.

- Yields 2.5-3.5bp higher across the curve, light flattening.

- Gilts ~1.5bp wider vs. Bunds after yesterday’s outperformance. 10-Year spread out to 197bp, any moves above 200bp have lacked conviction in recent sessions.

- The latest round of monthly public finance data looked a little better than both consensus and OBR forecasts. However, this was countered by revisions to the Apr-Jun data.

- Speculation surrounding the form that further fiscal tightening will take remains evident. Telegraph sources reported that Chancellor Reeves is to “consider cutting the tax-free pension lump sum in a move that would be expected to raise more than £2bn a year”.

- Note that the details of today’s flash PMI data pointed to a stagflationary backdrop, noting falling backlogs of work and employment, alongside rising input costs.

- SONIA futures flat to -4.5 given moves in the long end.

- BoE-dated OIS little changed to 2.5bp less dovish through ’25 meetings, showing ~10bp cuts through Dec.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Sep-25 | 3.975 | +0.8 |

Nov-25 | 3.911 | -5.6 |

Dec-25 | 3.870 | -9.7 |

Feb-26 | 3.774 | -19.4 |

Mar-26 | 3.736 | -23.2 |

Apr-26 | 3.665 | -30.2 |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSTRIA T-BILL AUCTION RESULTS: 3/6-month ATB Results

Jul-22 09:21

| Type | 3-month ATB | 6-month ATB |

| Maturity | Oct 30, 2025 | Jan 29, 2026 |

| Allotted | E758mln | E852mln |

| Previous | E500mln | E779mln |

| Amount | E1bln | E1bln |

| Target | E1bln | E1bln |

| Previous | E500mln | E1bln |

| Avg yield | 1.935% | 1.900% |

| Previous | 1.860% | 1.960% |

| Bid-to-cover | 1.99x | 2.06x |

| Previous | 2.75x | 1.8x |

| Bid-to-offer | 1.51x | 1.76x |

| Previous | 2.75x | 1.4x |

| Previous date | Jun 24, 2025 | Apr 22, 2025 |

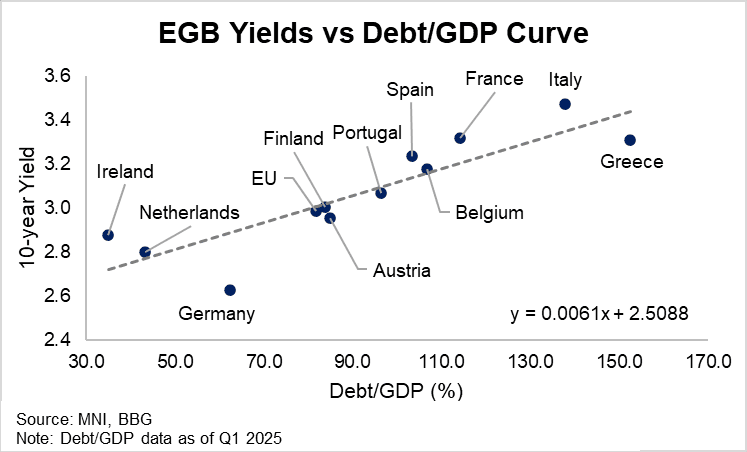

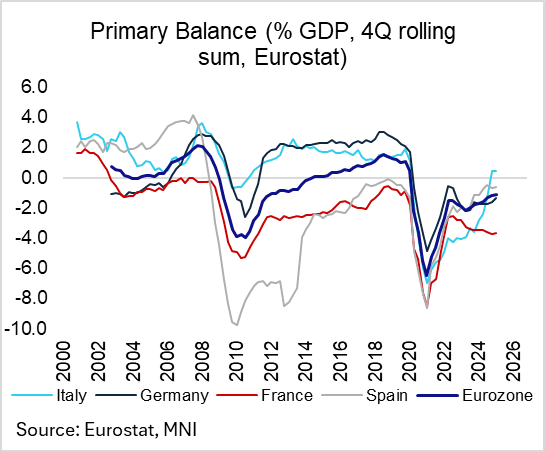

EGBS: Fiscal and Issuance Flow Supportive Of BTP/Obli Outperformance vs OATs

Jul-22 09:12

Incorporating yesterday’s Q1 Eurozone fiscal data, a simple chart of debt/GDP to 10-year yields crudely isolates Spanish, French and Italian bonds as cheap (i.e. trading above the linear line of best fit). While well documented French political and fiscal risks continue to warrant a yield premium for OATs, there may be scope for continued relative outperformance of Oblis and BTPs in the coming months.

- We wrote yesterday that while Italian interest expense growth exceeds that of nominal GDP, this is mitigated by the Government’s Q1 primary surplus of 0.4%. Meanwhile, strong Spanish real GDP growth post Covid has kept a healthy gap between interest expense growth and nominal GDP growth. Spain’s primary deficit also narrowed to 0.6% in Q1 from 0.7% in Q4. On the other hand, the difference between French interest expense growth and nominal GDP narrowed a notable 0.8pp to -0.7pp in Q1, a concerning development for the debt/GDP outlook given France's 3.6% primary deficit (despite ongoing attempts at fiscal consolidation).

- The outlook for net issuance also favours Italian and Spanish paper over France: We expect the mid-August Bono/Obli auction to be cancelled, while there is a sizeable E24bln Spanish redemption due on July 30. We also expect the mid-month 3/7/15-50-year BTP auction to be cancelled, with a E13bln BTP redemption then due on August 15. Meanwhile, we expect the two August OAT auctions to go ahead as planned, and there are no French redemptions due until October.

- Elsewhere, 10-year Bund yields trade rich to the debt/GDP curve owing to German paper’s haven/reserve status in the EGB space. Greece’s impressive fiscal consolidation continues to support GGBs, with 10-year yields currently trading just below OATs.

EGB OPTIONS: Bund Z5 Put Spread Buyer

Jul-22 09:11

RXZ5 127.00/125.50 put spread, paper pays 35 in 5k.