MNI US OPEN - Little Prospect of Breakthrough in Ukraine Talks

EXECUTIVE SUMMARY

- LOW-LEVEL RUSSIAN DELEGATION DAMPENS PROSPECT OF MAJOR BREAKTHROUGH

- TRUMP SAYS INDIA OFFERED TO REMOVE ALL TARIFFS ON US GOODS

- UK PRELIMINARY 1Q GDP DATA MIXED

- AUSTRALIA UNEMPLOYMENT STEADY AT 4.1%

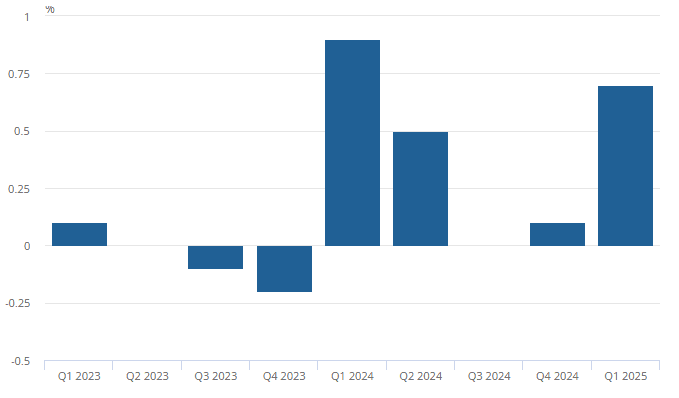

Figure 1: UK QoQ GDP growth a touch above expectations at 0.7% in 1Q

Source: ONS

NEWS

RUSSIA/UKRAINE (MNI): Low-Level Russian Delegation Dampens Prospect of Major Breakthrough

Russia's sending of a low-level delegation to talks with Ukraine taking place in Istanbul today has lowered expectations of any substantial progress being made towards a peace deal or ceasefire. Despite significant outside pressure, Russian President Vladimir Putin will not be in attendance. Instead, a very junior delegation has been sent, which includes presidential adviser, Vladimir Medinsky, a deputy foreign minister, Mikhail Galuzin and deputy defence minister Alexander Fomin. The Ukrainian side (as well as its European allies) is likely to view this as a signal of Russia's lack of interest in reaching an agreement. Talks are due to get underway shortly. Ukrainian President Volodymyr Zelenskyy will not attend the talks, instead meeting with Turkish President Recep Tayyip Erdogan in Ankara.

US/INDIA (BBG): Trump Says India Offered to Remove All Tariffs on US Goods

President Donald Trump said India has made an offer to drop tariffs on US goods, as the Asian nation seeks an agreement on import taxes. Speaking Thursday at an event with business leaders in Qatar, Trump said the Indian government has “offered us a deal where basically they are willing to literally charge us no tariff.” Trump did not offer further details of New Delhi’s apparent offer and the Indian government did not immediately respond to a request for comment.

US/IRAN (BBG): Trump Says US and Iran Are Closer to Reaching a Nuclear Deal

President Donald Trump said the US might be getting closer to an agreement with Iran to curb the Islamic Republic’s nuclear program. “I think we’re getting close to maybe doing a deal,” Trump said in Qatar at an event with business leaders on Thursday. “You probably read the story that Iran has sort of agreed to the terms.” Trump appeared to be referring to an NBC interview with Ali Shamkhani, an adviser to Iran’s Supreme Leader Ali Khamenei, in which Shamkhani reiterated Tehran’s position that it’s willing to limit uranium enrichment in exchange for sanctions relief. “We’ll see what happens,” Trump said. “But we’re in very serious negotiations with Iran for long-term peace. And if we do that, it’ll be fantastic.”

US/EU (MNI): Sefcovic - Agreed w/Lutnick to Intensify Technical Engagement on Tariff Deal

Delivering doorstep comments ahead of a meeting of EU trade ministers, European Commissioner for Trade Maros Sefcovic says that "Yesterday I had another constructive call with the US Secretary of Commerce Howard Lutnick," and went on to confirm that "We have agreed to intensify our engagement at technical levels and I am in regular contact with him. I think we will see each very soon, most probably here in Brussels or at the OECD meetings."

US/CHINA (BBG): US, Chinese Trade Negotiators Meet for Talks in South Korea

US and Chinese officials met for trade talks in South Korea on Thursday, just days after both sides met in Switzerland and agreed to pause some tariffs for 90 days. US Trade Representative Jamieson Greer sat down with China’s chief trade representative Li Chenggang in Jeju, South Korea, according to a South Korean official with knowledge of the matter. No other details have been provided yet and the US Embassy in Seoul didn’t immediately respond to a request to confirm the meeting.

US/S.KOREA (BBG): US, South Korea Hold Series of Trade Talks to Ease Tariff Impact

South Korea is holding a series of trade talks with US officials visiting Jeju for a regional summit, aiming to soften the blow from President Donald Trump’s tariffs. South Korea’s top two trade officials are meeting with US Trade Representative Jamieson Greer on the sidelines of the Asia-Pacific Economic Cooperation meeting on Thursday and Friday. The discussions kicked off with lower-level talks on Wednesday, and will be followed by meetings between Greer and Trade Minister Cheong Inkyo on Thursday, then with Industry Minister Ahn Duk-geun on Friday.

US (FT): US Poised to Dial Back Bank Rules Imposed in Wake of 2008 Crisis

US authorities are preparing to announce one of the biggest cuts in banks’ capital requirements for more than a decade, marking the latest sign of the deregulation agenda of the Trump administration. Regulators were in the next few months poised to reduce the supplementary leverage ratio, according to several people familiar with the matter. The rule requires big banks to have a preset amount of high-quality capital against their total leverage, which includes assets such as loans and off-balance sheet exposures such as derivatives.

US (WSJ): GOP Tax Debate Gets Testy as Conservatives Fume Over SALT

Conservative House members are fuming at some of their Republican colleagues from New York, New Jersey and California, whose insistence on a much larger state and local tax deduction is one of the biggest remaining hurdles to the party’s giant tax-and-spending bill. The current plan, approved Wednesday by the House Ways and Means Committee, includes a $30,000 cap for individuals and married couples that starts phasing down when income reaches $400,000. That is a boost from today’s $10,000, but it isn’t high enough for lawmakers like Reps. Mike Lawler (R., N.Y.) and Nick LaLota (R., N.Y.), whose negotiations with House leaders on what is known as the SALT cap are expected to drag into the weekend.

GERMANY (MNI): German Foreign Minister Supports 5% of GDP Military Spending

German Foreign Minister Johann Wadephul has publicly backed US President Donald Trump's calls for a massive increase in defense spending by the NATO states to five percent of their economic output, newspaper SZ comments on his speech today in Turkey: "Wadephul commented that this five percent could be divided into different areas. It may be agreed that traditional defense spending of 3.5 percent of gross domestic product (GDP) would be sufficient, provided that 1.5 percent of economic output was also spent on infrastructure for military use. Such an approach was recently proposed by NATO Secretary General Mark Rutte."

UK/EU (FT): Plans to Reset UK-EU Relations Hit Trouble Over Fishing Rights and Youth Mobility

Preparations for a post-Brexit “reset” of relations between the UK and the EU were thrown into turmoil on Wednesday after EU member states demanded further concessions from London over fishing rights and youth mobility. With only five days until an EU-UK summit in London, EU diplomats rejected European Commission attempts to bridge gaps between the two sides that have led to increasingly fraught negotiations. A draft EU communiqué setting out the terms of an improved EU-UK relationship will not now be finalised until Sunday, just a day ahead of the summit, after EU member states dug in over the terms of a deal.

CHINA (MNI EXCLUSIVE): China's Cities to Target Lower Homebuying Costs

MNI looks at how local Chinese authorities plan to support their property markets. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

DATA

EUROZONE DATA (MNI): Q1 GDP Revised Down a Tenth; Employment Above ECB Projections

- EUROZONE FLASH Q1 GDP +0.3% Q/Q, +1.2% Y/Y

- EUROZONE MAR IP +2.6% M/M, +3.6% Y/Y

Eurozone Q1 GDP was revised down on a rounded basis to 0.3% Q/Q, from an initial estimate of 0.4% and versus 0.2% in Q4. We noted this morning that a downward revision was certainly possible given the unrounded initial estimate was 0.352%. Eurostat's press release indicates that sequential growth rates in the four largest Eurozone economies (Germany, France, Italy and Spain) were unchanged from the initial release on a rounded basis, as was Ireland at 3.2% Q/Q.

UK DATA (MNI): UK GDP Data Mixed

- UK Q1 GDP +0.7% Q/Q, +1.3% Y/Y

- UK MAR IND PROD -0.7% M/M, -0.7% Y/Y

- UK MAR MANUF OUTPUT -0.8% M/M, -0.8% Y/Y

- UK MAR CONSTRUCTION OUTPUT +0.5% MM, +0% 3M3M, +1.4% YY

- UK MAR SERVICES INDEX +0.4% M/M, +0.7% 3MM

- UK MAR TRADE BALANCE GBP -3.7BN

Interesting mix: monthly GDP (which doesn't include trade) boosted by a strong services print of 0.4% M/M. Constuction also a bit stronger. Manufacturing a little soft. The quarterly GDP saw strong investment and GFCF than expected so surprised a tenth to the upside. Consumption was soft, however, at 0.2% Q/Q while government spending was also soft. The details of quarterly GDP are also quite hard to get a great read from. Aircraft imports were a big driver of GFCF. Looking at the breakdown of the Q/Q change in GDP: There was a positive contribution of 0.52ppt from GFCF (gross fixed capital formation), net trade contributed 0.36pt and household consumption contributed 0.12ppt.

FRANCE DATA (MNI): Final HICP Upwardly Revised by 0.10pp; 0.92% Y/Y

- FRANCE APR HICP +0.7% M/M, +0.9% Y/Y

- FRANCE APR CPI +0.6% M/M, +0.8% Y/Y

France final April HICP was slightly upwardly revised from the flash estimate, by 0.10pp for both Y/Y (to 0.92% from 0.82% vs March's 0.88%) and M/M (to 0.66% from 0.56% flash) measures. Revisions for the national CPI were driven by services printing 2.4% Y/Y (0.1pp upward) in energy -7.8% Y/Y (0.1pp upward). Food inflation meanwhile was unrevised at 1.2% Y/Y, as was manufactured goods inflation at -0.2% Y/Y. Elsewhere, core CPI printed +1.3% Y/Y - in line with prints from March and February.

NORWAY DATA (MNI): Solid Mainland Growth in Q1 Driven by Consumption and Investment

Norway Q1 mainland GDP was a solid 1.0% Q/Q - consistent with the "incorrect" figures published by Statistics Norway on Tuesday. That's notably above Norges Bank's 0.6% projection from the March MPR, so will have a net hawkish impact on the June MPR rate path, and possibly temper any expectations for a cut at that meeting. The surprise to Norges Bank's projection appears to be driven by both consumption and mainland investment.

SWITZERLAND DATA (MNI): Q1 Flash GDP Stronger Than Expected

Swiss Q1 GDP came in at 0.7% Y/Y according to SECO's flash estimate. That is considerably higher than consensus at 0.4% (and Q4's 0.5% Q/Q). "This growth was driven significantly by the services sector, with industry also showing overall expansion.", SECO added. SNB chairman Schlegel has recently flagged downside risks to their 1.0% - 1.5% 2025 growth estimate following the wide-scale US tariff announcement - he has not publicly provided commentary on that yet after tensions eased recently. Also, US restrictions on pharmaceutical firms announced (which are heavily represented in Switzerland) appeared lighter than feared when announced last week.

AUSTRALIA DATA (MNI): Aussie Unemployment Steady at 4.1%

- AUSTRALIA APR UNEMPLOYMENT RATE +4.1%

- AUSTRALIA APR EMPLOYED PERSONS CHANGE 89K

- AUSTRALIA APR F-T EMPLOYED PERSONS CHANGE 59.5K

- AUSTRALIA APR LABOR PARTICIPATION RATE +67.1%

The unemployment rate held steady at 4.1% over April, in line with expectations, while employment increased by 89,000, higher than the 22,000 jobs expected, data from the Australian bureau of statistics showed Thursday. Employment has grown by 390,000 people, or 2.7%, over the year, higher than the population growth rate for people aged 15 years and over, which was 2.1% over the same period, the ABS noted. “The participation rate for 35-44 year olds had the largest annual growth, up 1.9 percentage points to 88.3%,” said Sean Crick, head of labour statistics at the ABS.

FOREX: Japanese Yen Outperforms Amid Dented Risk Sentiment

- Major equity benchmarks are softer on Thursday, marginally eroding some of the weekly advance. This dynamic has boosted the likes of JPY and CHF, with lower core yields providing another moderate tailwind to the low yielders.

- For USDJPY, spot broke through the prior session lows in early European trade to print as low as 145.49, however, we note it is yet to close the gap to last Friday’s close at 145.37. This level will remain in short-term focus, before 145.10, the 20-day EMA. Overall, the latest USDJPY pullback underpins the view that gains since Apr 22 appear corrective.

- Underperformance for the higher beta currencies in G10, such as the antipodeans sees the likes of AUDJPY and NZDJPY falling around 0.8% today. For AUDJPY, the prior trendline resistance break now provides solid support at the 93.00 handle, with both the 20- and 50-day exponential moving averages intersecting just below this mark.

- The moderate risk-off tone is having little negative impact on the Euro, allowing EURUSD to rise back above the 1.12 handle on Thursday and broadly consolidate its recovery from its 50-day EMA support. Recent weakness appears corrective and key trend signals continue to highlight an uptrend.

- Stronger-than-expected UK growth data has only provided a modest boost to GBP, with cable hovering just below the 1.33 mark. A continuation higher would refocus attention on the key resistance and a bull trigger, at 1.3444, the Apr 28 / 29 high.

- Focus shifts to the flurry of US data releases, including PPI and retail sales, followed shortly after by an appearance from Fed Chair Powell.

EGBS: Crude Pullback Lends Support to Core FI; BTP/Bund Moves Away From 100bps

Bund futures trade near the top of today’s 37 tick range, currently +9 ticks at 129.48. Initial resistance is 129.71, the May 13 high. The sharp pullback in crude oil prices on hopes of a US/Iran nuclear deal has lent support to core FI today, with weaker equity futures also helping.

- German yields are 2-3bps lower on the session, with the short-end lightly outperforming.

- After marking below the psychological 100bps handle yesterday, the 10-year BTP/Bund spread has widened back to 102bps as European equities roll over.

- Eurozone Q1 GDP was revised down on a rounded basis to 0.3% Q/Q, from an initial estimate of 0.4% and versus 0.2% in Q4. We noted this morning that a downward revision was certainly possible given the unrounded initial estimate was 0.352%.

- Delivering doorstep comments ahead of a meeting of EU trade ministers, European Commissioner for Trade Maros Sefcovic says that "Yesterday I had another constructive call with the US Secretary of Commerce Howard Lutnick," and went on to confirm that "We have agreed to intensify our engagement at technical levels and I am in regular contact with him. I think we will see each very soon, most probably here in Brussels or at the OECD meetings".

- ECB-speak is scheduled from De Guindos, Cipollone and Villeroy. The latter two are on a CBDC panel, which may limit scope for near-term monetary policy comments.

- That leaves focus on this afternoon's US data and appearance from Fed Chair Powell.

GILTS: Yields a Little Lower, Cross-Asset Cues Dominate

Gilt futures hold away from yesterday’s lows, with crude oil continuing to trade lower and European equity benchmarks in the red.

- Contract last +10 at 91.15.

- Initial support and resistance located at 90.96 & 91.95, respectively, bear cycle intact.

- Yields 1.0-2.5bp lower, light outperformance in the long end.

- 2-Year yields still top 4.00% after yesterday’s close above, while 10s print at 4.70%, respective April highs remain unchallenged.

- Spread to Bunds ~1.5bp wider on the day at 202.5bp, with contained swings either side of 200bp seen in recent sessions.

- Soft pricing metrics were seen at the GBP2.0bln sale of the 0.125% Jan-28 gilt. Still, the yield on the line moved 0.5bp lower post-supply, representing a removal of concession.

- GBP STIR pricing little changed on the day. SONIA futures +1.5 to -1.5.

- BoE-dated OIS shows 1.5bp of cuts for next month, 18bp through August, 24bp through September, 37bp through November and 44bp through year-end, contracts are flat to 2.5bp more dovish on the day.

- Dovish BoE dissenter Dhingra will speak this afternoon (15:00 BST), although the topic of her address (“EU macroeconomic policy in an age of shocks”) may limit scope for updated comments surrounding her dovish stance.

- That will leave macro cues at the fore. U.S. PPI (which may be deemed stale, akin to the recent CPI reading) and weekly jobless claims readings headline the data calendar.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Jun-25 | 4.194 | -1.7 |

Aug-25 | 4.033 | -17.8 |

Sep-25 | 3.968 | -24.2 |

Nov-25 | 3.838 | -37.3 |

Dec-25 | 3.772 | -43.9 |

Feb-25 | 3.686 | -52.4 |

Mar-25 | 3.676 | -53.5 |

EQUITIES: Bullish Theme in Eurostoxx 50 Futures Intact Despite Latest Pullback

A bullish theme in the Eurostoxx 50 futures contract remains intact. Gains on Monday reinforce current bullish conditions. The contract is extending the recent breach of 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg. The continuation higher signals scope for a climb towards 5516.00, the Mar 3 high and the key bull trigger. Initial firm support to watch lies at 5162.15, the 50-day EMA. Clearance of this level would signal a possible reversal. A bullish trend condition in S&P E-Minis remains intact and this week’s appreciation reinforces current conditions. The contract has cleared an important resistance at 5837.25, the Mar 25 high and a bull trigger. This strengthens the bullish theme, paving the way for a continuation near-term. Sights are on the 6000.00 handle next. Initial firm support to watch lies at 5658.48, the 50-day EMA.

- Japan's NIKKEI closed lower by 372.62 pts or -0.98% at 37755.51 and the TOPIX ended 24.33 pts lower or -0.88% at 2738.96.

- Elsewhere, in China the SHANGHAI closed lower by 23.127 pts or -0.68% at 3380.821 and the HANG SENG ended 187.49 pts lower or -0.79% at 23453.16.

- Across Europe, Germany's DAX trades lower by 60.29 pts or -0.26% at 23467.79, FTSE 100 lower by 24.8 pts or -0.29% at 8559.97, CAC 40 down 20.12 pts or -0.26% at 7816.67 and Euro Stoxx 50 down 24.26 pts or -0.45% at 5379.18.

- Dow Jones mini down 179 pts or -0.43% at 41939, S&P 500 mini down 33.25 pts or -0.56% at 5875.25, NASDAQ mini down 152.25 pts or -0.71% at 21240.5.

Time: 09:50 BST

COMMODITIES: WTI Futures Fall Sharply But Still Above Bear Trigger at $54.67

A downtrend in WTI futures remains intact and recent gains are considered corrective. Key resistance to watch is $63.54, the 50-day EMA. It has been pierced, a clear break of it would highlight a stronger reversal. This would open $66.41, the Apr 4 high. For bears a reversal lower would refocus attention on $54.67, the Apr 9 low and bear trigger. Clearance of this support would confirm a resumption of the downtrend. A corrective cycle in Gold remains in play and the metal has traded lower this week. A key support at $3202.0, the May 1 low has been breached. The break of this level signals scope for a deeper retracement, towards $3085.0, 76.4% of the Apr 7 - Apr 22 upleg. Note that the 50-day EMA at $3165.0, has been breached, strengthening a bearish threat. Initial resistance is $3268.0, the 20-day EMA.

- WTI Crude down $2.43 or -3.85% at $60.88

- Natural Gas down $0.03 or -0.74% at $3.469

- Gold spot down $15.99 or -0.5% at $3160.27

- Copper down $4.4 or -0.95% at $460.95

- Silver down $0.33 or -1.02% at $31.8927

- Platinum down $6.58 or -0.67% at $978.61

Time: 09:50 BST

| Date | GMT/Local | Impact | Country | Event |

| 15/05/2025 | 1015/1215 | ECB's De Guindos At ISDA Meeting | ||

| 15/05/2025 | 1130/1330 | ECB's Cipollone In Digital Currency Fireside Chat | ||

| 15/05/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 15/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 15/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 15/05/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/05/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/05/2025 | 1230/0830 | *** | Retail Sales | |

| 15/05/2025 | 1230/0830 | *** | PPI | |

| 15/05/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/05/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 15/05/2025 | 1230/0830 | *** | Retail Sales | |

| 15/05/2025 | 1240/0840 | Fed Chair Jerome Powell | ||

| 15/05/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/05/2025 | 1315/0915 | *** | Industrial Production | |

| 15/05/2025 | 1400/1000 | * | Business Inventories | |

| 15/05/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 15/05/2025 | 1400/1500 | BOE Dhingra At New Economics Foundation conference | ||

| 15/05/2025 | 1400/1000 | * | Business Inventories | |

| 15/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 15/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 15/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 15/05/2025 | 1800/1400 | *** | Mexico Interest Rate | |

| 15/05/2025 | 1805/1405 | Fed Governor Michael Barr | ||

| 16/05/2025 | 2350/0850 | *** | GDP | |

| 16/05/2025 | 0430/1330 | ** | Industrial Production | |

| 16/05/2025 | 0730/0930 | ECB's Cipollone At EU Cyber Resilience Board Meeting | ||

| 16/05/2025 | 0800/1000 | *** | HICP (f) | |

| 16/05/2025 | 0900/1100 | * | Trade Balance | |

| 16/05/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 16/05/2025 | 1230/0830 | *** | Housing Starts | |

| 16/05/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 16/05/2025 | 1230/0830 | New York Fed's Roberto Perli | ||

| 16/05/2025 | 1230/0830 | *** | Housing Starts | |

| 16/05/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 16/05/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 16/05/2025 | 1500/1700 | ECB's Lane On Central Bank Communication Panel | ||

| 16/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/05/2025 | 2000/1600 | ** | TICS |