MNI US OPEN - Hyped CPI to be Scrutinized for Quality Concerns

EXECUTIVE SUMMARY:

- TRUMP SEEKS ELUSIVE TRADE DEAL WITH XI IN HIGH-STAKES MEETING

- CANCELLATION OF CANADA TRADE TALKS PUTS CARNEY IN TOUGH POSITION

- TAKAICHI PLEDGES TO BOOST INFLATION, DEFENSE RESPONSE

- MACRON WEIGHS STRONGEST TRADE TOOL AGAINST CHINA

- MUCH-ANTICIPATED CPI COULD BE LAST RELIABLE PRINT OF THE YEAR

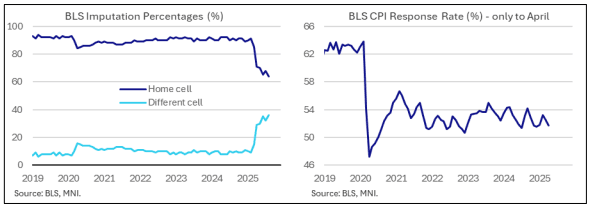

Figure 1: Inflation data quality in focus as response rate remains poor

NEWS

US/CHINA (BBG): Trump Seeks Elusive Trade Deal With Xi in High-Stakes Meeting

US President Donald Trump is aiming for a quick win in a pivotal Thursday meeting with Chinese counterpart Xi Jinping, even if the outcome falls short of the sweeping deal he’s teased on issues at the heart of the rivalry between the world’s two largest economies. Ahead of the sit-down, the US president said he wants to extend a pause on higher tariffs on Chinese goods in exchange for Xi resuming American soybean purchases, cracking down on fentanyl and backing off restrictions on rare-earth exports — all while maintaining some trade barriers he sees as essential.

MNI US CPI Preview Update: The Year’s Last ‘Reliable’ CPI Read: https://enews.marketnews.com/ct/x/pjJsdlCJluUI6aw2JBtwGQ~k1zZ8KXr-kA8x66XW5etptQM3-9HJw

- The delayed September CPI report is due for release on Friday Oct 24 at 0830ET, with the BLS making an exception on social security payments grounds during the government shutdown.

- It’s possibly the last report that won’t be adversely impacted by the shutdown until the new year, although quality concerns were already elevated with high reliance on imputed values back in August.

- We see a median unrounded analyst estimate at 0.41% M/M for headline and 0.32% M/M for core CPI.

- This would mark a marginal sequential acceleration for headline as energy strength offsets a slight moderation in core after a stronger than expected 0.35% M/M in August.

US (WSJ): U.S. Sends B-1 Bombers Near Venezuela, Ramping Up Military Pressure

The U.S. flew Air Force B-1 bombers near Venezuela on Thursday, stepping up pressure on President Nicolás Maduro only days after other American warplanes carried out an “attack demonstration” near the South American country.

EU/CHINA (MNI): Beijing, EU Hope For Deal - Advisors

Beijing still hopes to resolve trade frictions with the European Union, and to separate its dealings with the bloc from its disputes with the U.S., Chinese policy advisors told MNI, while an official in Brussels said the EU is optimistic that it will obtain an agreement to loosen restrictions on rare earth exports.

EU/CHINA (BBG): Macron Tells EU to Weigh Using Strongest Trade Tool on China

French President Emmanuel Macron told European Union leaders to consider using the bloc’s most powerful trade tool against China if they aren’t able to find a resolution to Beijing’s planned export controls on critical raw materials. Macron said they need to weigh using all options available against China, including the EU’s so-called anti-coercion instrument, according to people familiar with the matter.

US/CHINA (MNI): China U.S. Trade Relations Need Dialogue - Wang

Dialogue and communication remains the correct choice for China and the U.S. to handle trade relations, Minister of Commerce Wang Wentao told reporters on Friday in Beijing. Wang said the four rounds of trade talks between the two countries proves solutions can be found on the basis of mutual respect.

US/CANADA (MNI): Trump Cancelling Trade Talks Puts Carney In Tough Position

Following US President Donald Trump's announcement on Truth Social that he is terminating all trade talks with Canada, Prime Minister Mark Carney faces a

binary choice. Either seek to repair ties with the White House, or follow in Ontario Premier Doug Ford's footsteps and pursue a more aggressive line with

the US regarding trade.

JAPAN (BBG): Japan’s Takaichi Pledges Boost to Inflation Response, Defense

Japan’s Sanae Takaichi pledged to prioritize tackling a cost-of-living crunch and bolstering defense ahead of a visit by US President Donald Trump next week, in her first address to parliament as prime minister. With the speech, Takaichi sought to show that she will respond quickly to the issues irking voters frustrated by rising prices, while underlining her intent to project a tougher line on security. By honing in on new defense spending pledges she also appeared to be trying to make her mark on the premiership.

UK (The Guardian): Reeves considers breaking manifesto pledge with income tax rise to fill £30bn gap

The chancellor is in active discussions over breaking one of her party’s main manifesto pledges as she looks for ways to clear an estimated shortfall of more than £30bn, according to three sources close to the budget process. Some advisers in the Treasury and No 10 believe that raising income tax may be the only way to make sure she raises enough money never to have to come back for tax rises again in this parliament.

UK (The Guardian): Caerphilly byelection result live: Plaid Cymru beats challenge from Reform UK to win pivotal Welsh parliament vote

Plaid Cymru has won the Caerphilly byelection in south Wales, a dramatic result signalling a sharp realignment in Welsh politics with repercussions for the whole of Britain. Rhun ap Iorwerth’s party, which wants Wales to become independent, seized the Senedd (Welsh parliament) constituency from Labour and resisted a fierce challenge from Reform UK.

UKRAINE (The Guardian): Zelenskyy to meet Starmer and ‘coalition of the willing’ to discuss further military support

Ukrainian president Volodmyr Zelenskyy will travel to London on Friday for a meeting of the “coalition of the willing” hosted by prime minister Kier Starmer. Starmer intends to make the case for using frozen assets to fund Ukraine’s defences.

TURKEY (BBG): Turkish Court Dismisses Case Against Opposition in Markets Boost

A Turkish court dismissed a case that could topple the leader of the country’s main opposition party, offering temporary relief to investors concerned about renewed political instability. The court case was looking into allegations of irregularities during 2023 internal elections at Turkey’s secular Republican People’s Party, known by its Turkish initials CHP. Ozgur Ozel was named the CHP chief at that party congress and has since energized the opposition after years of losses and dealt a shock defeat to President Recep Tayyip Erdogan’s ruling party in last year’s municipal elections.

DATA

UK retail sales by volume are estimated to have risen by 0.5% m/m and 2.3% y/y in September, the Office for National Statistics said Friday, with ONS senior statistician Hannah Finselbach noting quarterly sales "were at their highest level since summer 2022.

UK consumer confidence edged higher in October, helped in part by an early round of autumn sales, a leading survey showed. The GFK Consumer Confidence Index rose two points to -17 in October, helped by the Major Purchase Index rising four points at -12, a nine-point improvement over this time last year. However, the forecast for personal finances over the next 12 months -- closely watched as an internal indicator by GFK staff – fell one point to +3.

JAPAN (MNI): Japan Sept Core CPI Rises 2.9% Vs. Aug 2.7%

Japan’s core consumer inflation accelerated to 2.9% y/y in September from August’s 2.7%, in line with market estimates, as higher energy prices offset a slowdown in food prices excluding perishables, data released Friday by the Ministry of Internal Affairs and Communications showed. The index remained above the Bank of Japan’s 2% target for the 42nd consecutive month but stayed below 3% for a second straight month.

BONDS: 10-year Gilt/Bund Spread Unable To Sustain A Move Below 180bps

The 10-year Gilt/Bund spread has been unable to sustain a move below the 180bp figure, with the stronger-than-expected UK October flash PMI placing modest upward pressure on Gilt yields over the past hour. A break of 180bps would expose the 2025 low at 177.5bps.

- The Gilt curve has twist flattened this morning, with 2- and 5-year yields up just over 1bp, 10-year yields up 0.5bps and 30-year yields down 0.5bps.

- Short-end weakness comes after today’s retail sales, inflation expectations and PMI reports were all hawkish on net. However, the majority of Wednesday’s CPI-inspired rally has held. Meanwhile, long-end yields are marginally lower amid reports the Chancellor is considering raising income tax at next month’s budget.

- The stronger-than-expected aggregate Eurozone flash PMIs (driven particularly by German services) have promoted a bear flattening in the German curve. 10-year Bund yields are up 3bps at typing, but have been unable to consolidate above resistance at ~2.62% (200-day EMA) for now.

- In futures, Bunds are -37 ticks at 129.60, while Gilts are -13 ticks at 93.42.

- 10-year EGB spreads to Bunds are up to 1bp wider, with OATs underperforming after the flash PMIs signalled continued weakness in the domestic growth outlook.

- Global focus turns to today’s US CPI report at 1330BST.

STIR: Only A Modest Hawkish Reaction To October Flash PMIs

GBP STIRs still hold onto the majority of the dovish reaction to Wednesday’s softer-than-expected UK inflation report, with the October flash PMI having a fairly contained impact on pricing for now. There remains just over a 60% implied probability of a Q4 BOE cut.

- SFIZ5 and H6 futures have fallen 1.5-2.0 ticks since the PMI was released.

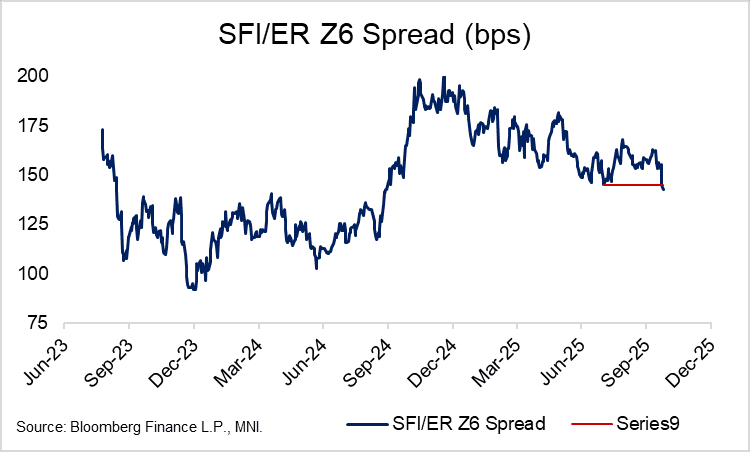

- However, note that the SFI/ER Z6 spread is still 1 tick tighter on the session at 142.5bps, following the stronger-than-expected Eurozone flash PMIs earlier. The August 1 low has now been breached in this spread.

- There will be two more labour market and inflation reports released before the BOE’s December 18 decision, alongside fallout from the November budget.

- Today’s retail sales, inflation expectations and PMI have all been hawkish on net, but the market is likely most focused on reports that the Chancellor may raise income tax next month.

| Meeting Date | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Nov-25 | 3.911 | -5.9 |

| Dec-25 | 3.819 | -15.0 |

| Feb-26 | 3.663 | -30.6 |

| Mar-26 | 3.607 | -36.2 |

| Apr-26 | 3.499 | -47.0 |

| Jun-26 | 3.467 | -50.2 |

| Jul-26 | 3.413 | -55.6 |

| Sep-26 | 3.396 | -57.3 |

| Source: MNI/Bloomberg Finance L.P |

FOREX: Trump Trade Headlines Weigh on CAD, JPY Downswing Extends

- The US administration's termination of trade talks with Canada brought overnight losses for the Canadian dollar, with Prime Minister Mark Carney facing a binary choice - either seek to repair ties with the White House, or pursue a more aggressive line with the US. The latter would be politically popular domestically, but risk further escalation from the Trump administration.

- Although USDCAD spiked on the news, the 40 pip reaction has been moderate so far, reaching an intra-day high of 1.4028. The price action does strengthen bullish trend conditions, however, the imminent release of US CPI has likely dampened the immediate impact as well as these headlines having less of a market impact in recent weeks. Sights are 1.4080, the Oct 16 high and the bull trigger, before the April 10 high at 1.4111.

- The moderate extension higher for US yields has further underpinned the USDJPY rally, which briefly rose above the 153.00 handle. A positive session today would mean the sixth consecutive day of gains, with eyes firmly on 153.27, the technical bull trigger. Comments from Fiscal Policy Minister Kiuchi suggesting little concern around a weaker JPY as well as FinMin Katayama not ruling out further JGB issuance to fund the upcoming economic assistance package will have also assisted the overnight price action. A break of 153.27 would open up 153.82, a Fibonacci projection.

- Initial weak French PMI data was offset by a stronger-than-expected German services flash PMI, prompting two-way price action for the Euro. For Germany, in addition to the stronger growth signals, an uptick in output charge inflationary pressures added to the hawkish theme of the flash report. However, EURUSD sits modestly lower on the session, perhaps owing to the renewed weakness for gold this morning, providing a marginal boost to the dollar.

- EURGBP now stands roughly unchanged from yesterday's breakout to the upside at 0.8713. The Guardian reported overnight on the potential for an income tax increase in the Autumn Budget, which would be the best option when considering which of the manifesto pledged taxes to increase in our view. The underlying trend condition in EURGBP remains bullish. Key resistance and the bull trigger remains at 0.8769, the Jul 28 high.

- US CPI will highlight today's data calendar, possibly being the last report that won’t be adversely impacted by the shutdown until the new year.

EQUITIES: US Futures Stabilizing, Led by Tech Shares and NASDAQ

The trend condition in S&P E-Minis remains bullish and the contract is trading above the 50-day EMA. The average, currently at 6637.80, has been pierced but remains intact - for now. Note that the Oct 10 low of 6540.25 marks the key short-term support. The trend structure in Eurostoxx 50 futures remains bullish. The breach of 5689.00, the Oct 2 high and bull trigger, confirms a resumption of the uptrend. This maintains the price sequence of higher highs and higher lows.

- Japan's NIKKEI closed higher by 658.04 pts or +1.35% at 49299.65 and the TOPIX ended 15.67 pts higher or +0.48% at 3269.45.

- Elsewhere, in China the SHANGHAI closed higher by 27.902 pts or +0.71% at 3950.312 and the HANG SENG ended 192.17 pts higher or +0.74% at 26160.15.

- Across Europe, Germany's DAX trades lower by 49.88 pts or -0.21% at 24159.02, FTSE 100 lower by 2.21 pts or -0.02% at 9575.66, CAC 40 down 32.47 pts or -0.39% at 8193.31 and Euro Stoxx 50 down 4.7 pts or -0.08% at 5663.63.

- Dow Jones mini down 7 pts or -0.01% at 46916, S&P 500 mini up 12.5 pts or +0.18% at 6787.5, NASDAQ mini up 88.25 pts or +0.35% at 25341.25.

COMMODITIES: WTI Recovery Holding, Clears Notable Resistance

A sharp pullback in Gold this week appears corrective - for now. Note that the trend is overbought and a deeper retracement would allow this condition to unwind. Support at the 20-day EMA, at $4046.2, has been pierced. The latest recovery in WTI futures appears corrective for now, however, note that price has traded through resistance at the 50-day EMA, at $61.11. The breach of this average signals scope for a stronger recovery and exposes $62.34.

- WTI Crude up $0.14 or +0.23% at $62

- Natural Gas down $0.01 or -0.27% at $3.337

- Gold spot down $65.83 or -1.6% at $4062.82

- Copper up $0.5 or +0.1% at $511.25

- Silver down $0.95 or -1.94% at $47.9027

- Platinum down $20.45 or -1.25% at $1607.83

| Date | GMT/Local | Impact | Country | Event |

| 24/10/2025 | 1200/0800 | ** | Brazil Preliminary CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/10/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 24/10/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 24/10/2025 | 1400/1000 | *** | New Home Sales | |

| 24/10/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 24/10/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 24/10/2025 | 1400/1000 | *** | New Home Sales | |

| 24/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 24/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |