STIR: Only A Modest Hawkish Reaction To October Flash PMIs

Oct-24 09:12

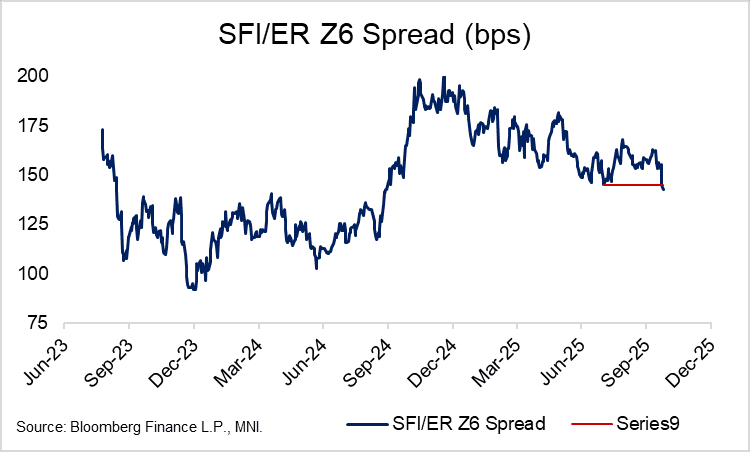

GBP STIRs still hold onto the majority of the dovish reaction to Wednesday’s softer-than-expected UK inflation report, with the October flash PMI having a fairly contained impact on pricing for now. There remains just over a 60% implied probability of a Q4 BOE cut.

- SFIZ5 and H6 futures have fallen 1.5-2.0 ticks since the PMI was released.

- However, note that the SFI/ER Z6 spread is still 1 tick tighter on the session at 142.5bps, following the stronger-than-expected Eurozone flash PMIs earlier. The August 1 low has now been breached in this spread.

- There will be two more labour market and inflation reports released before the BOE’s December 18 decision, alongside fallout from the November budget.

- Today’s retail sales, inflation expectations and PMI have all been hawkish on net, but the market is likely most focused on reports that the Chancellor may raise income tax next month.

| Meeting Date | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Nov-25 | 3.911 | -5.9 |

| Dec-25 | 3.819 | -15.0 |

| Feb-26 | 3.663 | -30.6 |

| Mar-26 | 3.607 | -36.2 |

| Apr-26 | 3.499 | -47.0 |

| Jun-26 | 3.467 | -50.2 |

| Jul-26 | 3.413 | -55.6 |

| Sep-26 | 3.396 | -57.3 |

| Source: MNI/Bloomberg Finance L.P |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ITALY AUCTION RESULTS: BTP Short Term / BTPei Results

Sep-24 09:08

| 2.10% Aug-27 BTP Short Term | 1.10% Aug-31 BTPei | 2.40% May-39 BTPei | |

| ISIN | IT0005657330 | IT0005657348 | IT0005547812 |

| Amount | E2.5bln | E1.25bln | E1.25bln |

| Previous | E3bln | E1.5bln | E1.25bln |

| Avg yield | 2.23% | 1.17% | 2.13% |

| Previous | 2.20% | 1.13% | 1.97% |

| Bid-to-cover | 1.57x | 1.67x | 1.67x |

| Previous | 1.56x | 1.51x | 1.45x |

| Avg Price | 99.78 | 99.60 | 103.33 |

| Pre-auction mid | 99.753 | 99.514 | 103.199 |

| Prev avg price | 99.82 | 99.83 | 105.52 |

| Prev mid-price | 99.801 | 99.739 | 105.447 |

| Previous date | 26-Aug-25 | 24-Jul-25 | 25-Sep-24 |

GERMAN AUCTION PREVIEW: 2.50% Nov-32 Bund

Sep-24 09:07

This morning, Germany will reopen its on-the-run 7-year 2.50% Nov-32 Bund (ISIN: DE000BU27014) for E4bln.

- The launch auction of the line on August 27 was very soft with only E3.170bln of bids received for the intended E4.0bln transaction. Today’s auction will be for the same E4bln size but we note that in Q4 there will only be one auction with a smaller E3bln size, on October 21. If there was more flexibility in the DFA’s funding programme we expect today’s auction would have been downsized after the first was held, too.

- Specifically, the August opening saw a bid-to-cover of 1.19x and a bid-to-offer of 0.79x after desks pointing to the potential for softer demand ahead of the auction, with the 7-year area falling between the demand sweet spots of 5-year and 10-year, making for fewer natural buyers in this area of the curve. The 0.79x bid-to-offer was the joint lowest seen in the German 7-year segment since August 2022.

- Domestically in Germany, Chancellor Merz headlined earlier today, saying his government will make concrete proposals for a pension system reform this year. While not a new theme, it is worth watching the evolution of the German pension system given the potential knock on impact for flows / holdings. On data, today's IFO Business Climate index saw some broad-based underperformance.

- The next German auction will be E5bln of the 10-year 2.60% Aug-35 Bund (ISIN: DE000BU2Z056) on October 1.

- Timing: Results will be available shortly after the bidding window closes at 10:30BST / 11:30CEST.

FOREX: USD Outperforming, AUDNZD Surges to Fresh Cycle High Above 1.13

Sep-24 09:05

- Over the course of the European morning, the US Dollar is trading with a supportive tone. Despite most major pairs remaining well within the post-Fed ranges, the likes of EUR and GBP have extended session declines to just shy of 0.4% in recent trade. For EURUSD, the solid amount of option expiries between 1.1750/1.18 appears to have capped the overnight price action, with the pair slowly edging back below 1.1775 as we approach the NY crossover.

- GBPUSD has traded through the 50-day EMA and this leaves support at 1.3458 exposed, a trendline drawn from the Aug 1 low. Clearance of this line would strengthen a bearish threat.

- Firmer-than-expected monthly CPI data in Australia is prompting some Aussie outperformance, with AUDUSD currently up 0.15% and bucking the stronger dollar theme. Market participants have been more focussed on AUDNZD, which has extended its impressive rally on Wednesday to trade to a fresh cycle high of 1.1317. Resistance remains scant on the chart until 1.1491, the 2022 high. It is also worth noting that the NZ government has appointed Riksbank First Deputy Governor Anna Breman to be the new RBNZ governor.

- The low yielders have been under pressure this morning, with USDJPY notably rising to within 10 pips of the post Fed highs at 148.38. Uncertainty regarding Japanese politics and the upcoming LDP leadership election may be playing its part here, while moving average studies continue to highlight a dominant uptrend. Furthermore, the impressive grind higher for the likes of EURJPY and CHFJPY bolster the bearish yen theme.

- US new home sales is the main data point later today, before Thursday’s SNB decision and US jobless claims data.