MNI US OPEN - Germany CPI Projected at 2.1% Y/Y

EXECUTIVE SUMMARY

- WALLER SAYS DATA WILL DETERMINE FED CUT PACE

- TRUMP PICK MIRAN ON TRACK FOR CONFIRMATION BEFORE FED MEETS

- MNI PROJECTS 2.1% Y/Y GERMAN NATIONAL CPI, CORE 2.7-2.8%

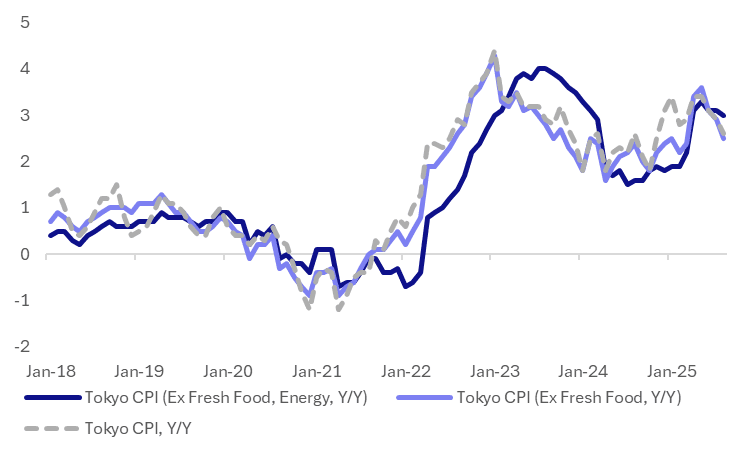

- TOKYO CORE CPI RISES 2.5% IN AUGUST VS. JULY 2.9%

Figure 1: Tokyo CPI Y/Y Trends, Core Still Elevated

Source: MNI/Bloomberg Finance L.P.

NEWS

FED (MNI): Waller Says Data Will Determine Fed Cut Pace

Federal Reserve Governor Christopher Waller said Thursday the pace of interest rate cuts will be determined by incoming economic data, but the direction lower to neutral is clear. "We know roughly where we're going towards neutral, but how fast we get there is gonna depend on the data that comes in," he said in Q&A at an event with the Economic Club of Miami.

US (BBG): Trump Pick Miran On Track for Confirmation Before Fed Meets

The Republican-led US Senate is likely to meet the ambitious target outlined by the Trump administration to fast-track Stephen Miran’s Federal Reserve confirmation before the central bank’s September rate-setting meeting, barring any procedural glitches or unexpected opposition. The Senate Banking Committee announced Thursday it would hold a hearing on Miran’s confirmation Sept. 4 at 10 a.m. Washington time. Democrats privately acknowledge they can’t block Miran’s ascension on their own, and under the rules they can only hold it up briefly in the committee, and for a few days on the Senate floor.

US/INDIA (BBG): India Steps Up US Crude Buying as Russian Flows Under Scrutiny

Indian refiners have stepped up their purchases of US crude after price drops, as Washington cracks down on the Asian nation for buying Russian barrels. This week, state and private oil processors including Reliance Industries Ltd., Indian Oil Corp. and Bharat Petroleum Corp. bought more US West Texas Intermediate crude than normal, according to traders who asked not to be identified as they’re not authorized to speak to the media. The main driver was more favorable prices for the grade, which have weakened relative to Middle East benchmarks, they said.

US/JAPAN (BBG): Japan’s Akazawa to Take Another US Trip Ahead of Executive Order

Japan’s top trade negotiator said he expects to visit the US at least once more before the Trump administration issues an executive order that would formally lower tariffs on goods imported from Japan. “At this point, I will likely visit the US at least once before the executive order is issued,” Ryosei Akazawa, minister for economic revitalization, said in a post-cabinet meeting press conference Friday. “After the administrative consultations are finalized, consultations among ministers will still be required, and there are consultations that must be completed before the agreement can be implemented.”

CHINA (WSJ): Alibaba Creates AI Chip to Help China Fill Nvidia Void

Chinese chip companies and artificial-intelligence developers are building up their arsenal of homegrown technology, backed by a government determined to win the AI race with the U.S. The latest example: China's biggest cloud-computing company, Alibaba, has developed a new chip that is more versatile than its older chips. Alibaba was long one of the biggest customers of American AI-chip leader Nvidia. Now it and other chip designers are filling the void left after Nvidia ran into regulatory barriers to selling its products in China.

EU/RUSSIA (BBG): EU’s Top Diplomat Touts Secondary Sanctions Against Russia

Secondary sanctions and measures aimed at Russia’s energy sector would be most effective in curbing Moscow’s ability to wage war against Ukraine, according to the European Union’s foreign policy chief, Kaja Kallas. Russia’s attack this week on Kyiv, which also damaged the EU’s representative offices in the capital, is yet another reason to increase pressure on Russia, Kallas told reporters in Copenhagen Friday ahead of an informal meeting of defense ministers.

UK (FT): City Fears Mount That Budget Will Target Banks to Help Fill £20bn Fiscal Hole

Fears are growing in the City of London that chancellor Rachel Reeves will target banks to help shore up the UK’s public finances, despite executives warning a tax raid on lenders would damage the government’s growth agenda. A surcharge on the sector’s profits or even a new bank levy is seen as a possible way to help fill a fiscal hole estimated by economists to be at least £20bn. “Politically it is an easy target,” said one senior banker. “No one likes banks, they are seen as a whipping boy for the government.”

RBA (BBG): RBA Warns of Financial Stability Risks From Private Market Boom

Australia’s central bank warned that a global shift of financing away from regulated banks and into private markets is making it harder for authorities to contain risks to the financial system, days after the nation’s corporate watchdog vowed to step up scrutiny of the sector. “Changes in the nature of financial intermediation internationally, where more financing is occurring outside of prudentially regulated entities, is limiting the ability of authorities to monitor and address potential financial stability risks,” the Reserve Bank said in its 2025/26 corporate plan published Friday.

JAPAN (BBG): Japan Asks Primary Dealers for Views on Long Bond Supply Cut

Japan’s Ministry of Finance has asked primary dealers for their views on further reducing issuance of longer-maturity government bonds, according to people familiar with the matter. The ministry on Wednesday sent a questionnaire about potentially cutting back on enhanced liquidity auctions, said the people, who declined to be identified because the matter is not public. The MOF action comes amid concerns that yields on long-dated bonds have risen rapidly to levels some consider excessive, and follows a plan announced in June to trim the volume of 20-, 30- and 40-year bonds sold at regular auctions.

THAILAND (MNI): Constitutional Court Deems PM Guilty, Removes Her From Office

The Constitutional Court deems Prime Minister Paetongtarn Shinawatra guilty of violating ethics standards and removes her from office, delivering a major blow to her Pheu Thai Party (PTP) and the Shinawatra clan. Despite initially saying that Paetongtarn has the required integrity and sought to protect the peace and well-being of the people, the top court resolves that her handling of the border dispute with Cambodia undermined national interest. Paetongtarn Shinawatra becomes the firth Thai Prime Minister removed through judicial intervention. Her ouster is set to throw Thailand into renewed political turmoil.

INDIA/JAPAN (BBG): Modi to Secure Japan Investment With Pledge to Deepen Ties

Indian Prime Minister Narendra Modi and Japanese Prime Minister Shigeru Ishiba pledged deeper economic ties ahead of a summit meeting later on Friday, as they partner up amid trade uncertainty brought on by soaring US tariffs. “Japan and India are strategic partners that share universal values including freedom, democracy, and the rule of law,” said Ishiba at a joint India-Japan economic forum held Friday afternoon, adding that the two economies are building a strong and stable supply chain.

PHILIPPINES (BBG): Philippines May Hold Key Rate for Rest of 2025, BSP Chief Says

The Philippine central bank may stand pat on its key interest rate for the remainder of the year if prices remain cool and domestic demand holds, according to Governor Eli Remolona. “I think we’ve reached our sweet spot for inflation as well as for output growth. If the numbers stay the way they are, then we won’t need another rate cut,” Remolona said Friday in an interview with Bloomberg Television’s Yvonne Man and Annabelle Droulers.

DATA

ECB DATA (MNI): Consumers See Firmer 3Y Inflation, Unchanged 1Y and 5Y

- ECB 1-YEAR CONSUMER INFLATION EXPECTATIONS 2.6%

- ECB 3-YEAR CONSUMER INFLATION EXPECTATIONS 2.5%

Perception of inflation over previous 12 months: 3.1%, unchanged for a sixth consecutive month. 1Y ahead: 2.6% (BBG cons 2.5), unchanged from the 2.6% in June having eased from a recent high of 3.1% in April. 3Y ahead: 2.5% (BBG cons 2.4), a tenth higher after 2.4% in June. It was 2.5% in Mar-Apr having last been higher in late 2023. 5Y ahead: 2.1%, unchanged for an eighth consecutive month. Uncertainty about inflation expectations over the next 12 months remained at the lowest since Jan 2022.

GERMANY DATA (MNI): MNI Projects 2.1% Y/Y German National CPI, Core 2.7-2.8%

From state-level data that equates to 89.1% weighting of the national July flash German CPI print (due at 13:00 GMT / 14:00 CET), MNI estimates that national CPI (non-HICP print) rose by around 2.1% Y/Y (2.0% prior) and rose around 0.0% M/M. See the tables below for full calculations. Analyst consensus stands at 2.0% Y/Y and 0.0% M/M, risks to consensus appear to be skewed to the upside. Current tracking of Core CPI (ex-energy and food, based on 50% of the national index) implies between 2.7-2.8% Y/Y (2.7% prior).

GERMANY AUG UE RATE (SA) 6.3% (FCST 6.3%); JUL 6.3% (MNI)

GERMANY AUG UE NET CHANGE (SA) -9K; JUL +2K (MNI)

FRANCE DATA (MNI): French Services Lead Softer CPI Inflation in August Flash

- FRANCE AUG HICP +0.5% M/M, +0.8% Y/Y

- FRANCE AUG CPI +0.4% M/M, +0.9% Y/Y

- FRANCE JUL PPI +0.4% M/M, +0.4% Y/Y (VS -0.1% M/M, +0.3%

France HICP inflation was marginally softer than expected in the preliminary August release although national CPI inflation was more clearly softer than expected, led by transportation services. HICP inflation eased to 0.83% Y/Y (BBG cons 0.9, MNI median of a narrower pool of analysts 0.8) in the August preliminary release after 0.94% Y/Y in July. The 0.48% M/M matched with Bloomberg consensus of 0.5% after 0.28% M/M in July. CPI inflation was more clearly softer than expected at 0.88% Y/Y (cons 1.0) in the Aug prelim after 1.00% Y/Y in July.

FRANCE GDP Q2 FINAL +0.3% Q/Q (VS +0.1% Q1) (MNI)

FRANCE GDP Q2 FINAL +0.8% Y/Y (VS +0.6% Q1) (MNI)

SPAIN DATA (MNI): Spanish HICP/CPI Undershoot But Core CPI Firmer

- SPAIN AUG FLASH HICP +0% M/M, +2.7% Y/Y

- SPAIN AUG FLASH CPI +0% M/M, +2.7% Y/Y

- SPAIN AUG FLASH CORE CPI +2.4% Y/Y

Spain HICP and CPI inflation both undershot expectations in preliminary August data as they held steady in Y/Y terms. However, core CPI is estimated to have accelerated a tenth to 2.4% Y/Y, back to April rates. HICP inflation is estimated to have held steady at 2.7% Y/Y (Bloomberg cons 2.8%) in the preliminary August release. Core HICP inflation is estimated at 2.4% Y/Y. CPI inflation is also estimated to have held steady at 2.7% Y/Y (Bloomberg cons 2.8) in the Aug prelim.

GERMANY JUL RETAIL SALES -1.5% M/M, +1.9% Y/Y (MNI)

GERMANY JUL EXPORT PRICES +0.6% Y/Y (MNI)

GERMANY JUL IMPORT PRICES -1.4% Y/Y (MNI)

ITALY AUG FLASH HICP 1.7% Y/Y (1.8% FCAST, 1.7% JUL) (MNI)

ITALY Q2 GDP -0.1% Q/Q (-0.1% FLASH, 0.3% Q1) (MNI)

SWEDEN DATA (MNI): Q2 GDP a Tenth Above Consensus; 4 Tenths Below Riksbank Forecast

- SWEDEN FINAL Q2 GDP +1.4% Y/Y

Swedish Q2 GDP is a tenth higher than consensus at 0.5%Q/Q (0.4% expected, albeit there was a range of estimates from 0.1-0.8% in the Bloomberg survey. This is, however, below the Riksbank's 0.9% projection. Again flash was a poor indicator of this print, coming in at 0.1%Q/Q.

SWEDEN FINAL Q2 GDP +1.4% Y/Y (MNI)

JAPAN DATA (MNI): Aug Tokyo Core CPI Rises 2.5% vs. July 2.9%

- JAPAN AUG TOKYO CORE CPI +2.5% Y/Y; JULY +2.9%

- JAPAN AUG TOKYO CORE-CORE CPI +3.0% Y/Y; JULY +3.1%

- JAPAN AUG SERVICES PRICES +2.0% Y/Y; JULY JULY +2.1%

Tokyo’s core inflation slowed to 2.5% y/y in August from 2.9% in July but remained above 2% for the 10th straight month, data from the Ministry of Internal Affairs and Communications showed Friday. The slowdown was driven by energy prices (-5.3% vs -0.8%), while food excluding perishables stayed firm (+7.4% vs +7.4%). Core-core CPI, which strips out both fresh food and energy and is closely watched as a gauge of underlying inflation, rose 3.0% y/y in August, easing from 3.1% but marking a sixth straight month above 2%.

JAPAN DATA (MNI): July Factor Output Posts 1st Drop in 2 Months

- JAPAN JULY FACTORY OUTPUT -1.6% M/M; JUNE +2.1%

Japan’s industrial output fell 1.6% m/m in July, the first drop in two months, after rising 2.1% in June due to weaker auto production, data from the Ministry of Economy, Trade and Industry showed Friday. Automobile production declined 6.7%, the first fall in three months, reversing a 0.5% rise in June as front-loaded exports ahead of U.S. tariffs weighed. Output of electronic parts and devices rose 2.4%, extending June’s 8.8% gain.

JAPAN DATA (MNI): Japan Consumer Confidence Posts 1st Rose in 2 Mnths

Japan's consumer confidence index rose in August for the first time in two months, up 1.2 points to 34.9 from 33.7 in July, Cabinet Office data showed Friday. The government left its assessment unchanged. All sub-indexes, covering economic well-being, income conditions, the labour market and willingness to buy durable goods, posted gains. A separate sub-index on asset prices, not included in the main calculation, rose to 43.8 in August from 41.7.

JAPAN DATA (MNI): U/E Rate Down, but Divergences From Steady Job-To-Applicant Ratio

- JAPAN JULY JOBLESS RATE FALLS TO 2.3% FROM JUNE 2.5%

Japan's jobless rate surprised on the downside in July, printing at 2.3%, versus 2.5% forecast, which was also the June outcome. The job-to-applicant ratio ticked down a touch to 1.22, versus 1.23 forecast, while the June outcome was 1.22. The labour force participation rate eased to 63.9% from 64.2% in June, with the m/m change for those not in the labour force rising by 150k. The number of people employed fell by -10k, after a -50k dip in June. So, whilst the jobless rate suggests a tight labour market, other indicators are painting a less hawkish picture.

JAPAN JULY RETAIL SALES +0.3% Y/Y; JUNE +1.9% (MNI)

JAPAN JULY RETAIL SALES -1.6% M/M; JUNE +0.9% (MNI)

FOREX: USD Index Erases Early Strength, EURGBP Extends Bounce

- Over the course of the European morning, the US Dollar has been edging lower, erasing the modest strength from overnight and briefly slipping into negative territory on the day. This has been most notable for USDJPY, falling around 30 pips from the 147.20 highs, placing the focus back on yesterday’s low of 146.66 and last Friday’s post Powell low at 146.58.

- EURUSD has traded in similar vein, grinding higher as the plethora of Eurozone inflation releases have failed to garner any bearish momentum. This keeps a more constructive tone present as we approach the important July PCE data out of the US, the MNI Chicago PMI and month end. Primary trend conditions remain bullish, however key resistance and the bull trigger remain further out at 1.1829, the Jul 1 high.

- In contrast, sterling weakness is standing out early Friday, helping EURGBP extend its recovery this week. A break above 0.8674 would signal a stronger reversal, placing the cross at its highest levels in three weeks.

- Although moves remain broadly contained, the Kiwi dollar sits atop the G10 leaderboard as NZDUSD extends its bounce from firm pivot support at 0.5800 to around a big figure. Bearish conditions overall for NZDUSD might suggest that good supply is seen into 50-day EMA resistance around 0.5930. The dovish RBNZ has seen the AUDNZD surge higher breaking back above 1.1000 convincingly. There have been some primary signs overnight of momentum stalling above 1.1100, however, look for dips back towards 1.1000/1.1030 to be supported.

- Elsewhere, USDCHF has once again dipped its toe back below the 0.8000 mark after reaching fresh one-month lows yesterday. Supportive but grinding price action for the swissie has seen EURCHF consolidate back below the 0.94 to current spot levels of 0.9350, very familiar territory for the cross in recent months. Swiss CPI is set for release next week.

BONDS: EGBs & Gilts Bear Steepen, Recent Ranges Intact

Core global FI markets trade away from session highs, with both Bund and gilt futures sticking to ranges established during recent sessions, light bear steepening seen on both cash curves (Yields flat to +2.5bp).

- Little reaction to a mixed bag for Eurozone inflation readings, with HICP generally undershooting but with some differing core readings. German CPI tracking from state-level releases points to a 0.1ppt acceleration to 2.1% Y/Y, as expected, and perhaps a similar acceleration for core.

- EGB spreads to Bunds little changed to 2bp wider, peripherals under the most pressure as equity benchmarks trade lower.

- OAT/Bunds remains below both this week’s high and 80bp, with ’24 & ’25 highs untested. French 5-Year CDS also remains below the ’24 & ’25 tops.

- Overall, this points to a slightly more sanguine market outlook on French creditworthiness when compared to other recent instances of political stress.

- We provided some reasoning as to why previous highs in French credit metrics have not been tested in a recent bullet.

- In the UK, the DMO’s FQ3 issuance plan was largely in line with our expectations.

- There has been some focus on a thinktank proposing a windfall tax on UK banks, with fiscal fragility remaining front and centre in the UK.

- A reminder that source reports have previously suggested that Labour is looking to widen national insurance contributions to include landlord rental income.

- STIR markets little changed to a touch more hawkish alongside the move in core global FI, but remain within recent ranges, pointing to 19bp of ECB easing through June ’26, while the GBP strip prices just under 10bp of BoE cuts through year-end.

EQUITIES: Fresh Cycle Highs for E-Mini S&P Reinforces Bullish Theme

The trend set-up in Eurostoxx 50 futures is bullish and the pullback from the Aug 22 high appears corrective - for now. Support to watch lies at 5376.70, the 50-day EMA. A clear break of this average would strengthen a short-term bearish threat and signal scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. Resistance to watch is 5522.00, the Aug 22 high. Clearance of this hurdle would resume the uptrend. S&P E-Minis bulls remain in the driver’s seat and the contract traded to a fresh cycle high yesterday. The maintains the bullish price sequence of higher highs and higher lows. Moving average studies are in a bull-mode position too, highlighting a clear uptrend and positive market sentiment. Attention is on 6543.75, a Fibonacci projection. Support to watch lies at 6326.74, the 50-day EMA.

- Japan's NIKKEI closed lower by 110.32 pts or -0.26% at 42718.47 and the TOPIX ended 14.6 pts lower or -0.47% at 3075.18.

- Elsewhere, in China the SHANGHAI closed higher by 14.33 pts or +0.37% at 3857.927 and the HANG SENG ended 78.8 pts higher or +0.32% at 25077.62.

- Across Europe, Germany's DAX trades lower by 139.96 pts or -0.58% at 23899.83, FTSE 100 lower by 29.92 pts or -0.32% at 9186.92, CAC 40 down 54.28 pts or -0.7% at 7708.32 and Euro Stoxx 50 down 39.15 pts or -0.73% at 5357.58.

- Dow Jones mini down 154 pts or -0.34% at 45552, S&P 500 mini down 19.75 pts or -0.3% at 6497.5, NASDAQ mini down 106.75 pts or -0.45% at 23662.

Time: 10:00 BST

COMMODITIES: Gold Approaching Resistance at $3439.0, the Aug 23 High

Despite recent gains, a bear cycle in WTI futures remains intact and the latest recovery appears corrective. A key support at $61.99, the Jun 30 low, has recently been breached, strengthening a bearish theme. A continuation lower would open $57.71, the May 30 low. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $66.56, the Aug 4 high. Gold traded higher on Thursday. The medium-term trend condition remains bullish - moving average studies are in a bull-mode position highlighting a dominant uptrend. Resistance to watch is $3439.0, the Aug 23 high. A break of this level would expose the key resistance and bull trigger at $3500.1, the Apr 22 low. On the downside, the first key support to watch is $3268.2, the Jul 30 low. A breach of it would highlight a bearish threat.

- WTI Crude down $0.43 or -0.67% at $64.17

- Natural Gas up $0.03 or +1.15% at $2.979

- Gold spot down $6.48 or -0.19% at $3410.49

- Copper up $3.15 or +0.69% at $457.15

- Silver down $0.07 or -0.18% at $38.9765

- Platinum down $16.92 or -1.24% at $1345.99

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 29/08/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 29/08/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 29/08/2025 | 1230/0830 | *** | GDP - Canadian Economic Accounts | |

| 29/08/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 29/08/2025 | 1230/0830 | *** | CA GDP by Industry and GDP Canadian Economic Accounts Combined | |

| 29/08/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 29/08/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/08/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 29/08/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 29/08/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 29/08/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 29/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 29/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 31/08/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/08/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI |