EQUITIES: Fresh Cycle Highs for E-Mini S&P Reinforces Bullish Theme

The trend set-up in Eurostoxx 50 futures is bullish and the pullback from the Aug 22 high appears corrective - for now. Support to watch lies at 5376.70, the 50-day EMA. A clear break of this average would strengthen a short-term bearish threat and signal scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. Resistance to watch is 5522.00, the Aug 22 high. Clearance of this hurdle would resume the uptrend. S&P E-Minis bulls remain in the driver’s seat and the contract traded to a fresh cycle high yesterday. The maintains the bullish price sequence of higher highs and higher lows. Moving average studies are in a bull-mode position too, highlighting a clear uptrend and positive market sentiment. Attention is on 6543.75, a Fibonacci projection. Support to watch lies at 6326.74, the 50-day EMA.

- Japan's NIKKEI closed lower by 110.32 pts or -0.26% at 42718.47 and the TOPIX ended 14.6 pts lower or -0.47% at 3075.18.

- Elsewhere, in China the SHANGHAI closed higher by 14.33 pts or +0.37% at 3857.927 and the HANG SENG ended 78.8 pts higher or +0.32% at 25077.62.

- Across Europe, Germany's DAX trades lower by 139.96 pts or -0.58% at 23899.83, FTSE 100 lower by 29.92 pts or -0.32% at 9186.92, CAC 40 down 54.28 pts or -0.7% at 7708.32 and Euro Stoxx 50 down 39.15 pts or -0.73% at 5357.58.

- Dow Jones mini down 154 pts or -0.34% at 45552, S&P 500 mini down 19.75 pts or -0.3% at 6497.5, NASDAQ mini down 106.75 pts or -0.45% at 23662.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: EU Bank Call Spread

SX7E (20/03/26) 230/240cs, bought for 2.95 in 6k (ref 215.35).

EURIBOR OPTIONS: ERZ5 98.12/98.06/98.00 Put Fly Lifted

ERZ5 98.12/98.06/98.00 put fly paper paid 0.5 (vs. 98.13) on 5K.

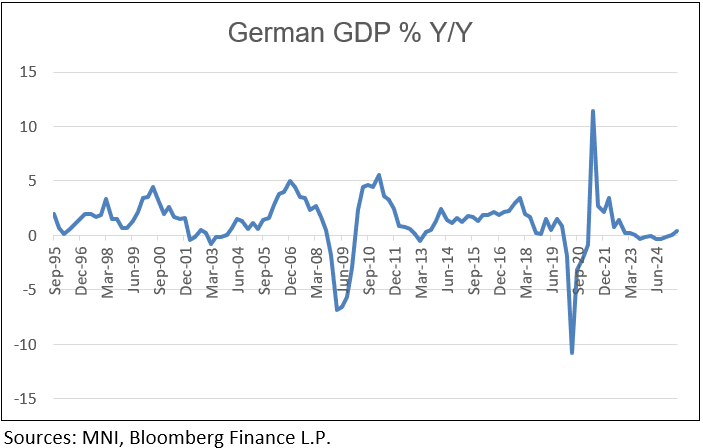

GERMAN DATA: Q2 Flash GDP As Weak As Expected, Negative Investment Contribution

German Q2 flash GDP came in as expected, at -0.1% Q/Q (-0.1% consensus, +0.3% Q1 downwardly revised by 0.1pp).

- "Investment in equipment and construction in the second quarter of 2025 was lower than in the previous quarter, according to preliminary findings. Private and government consumption expenditure, on the other hand, rose after adjustment for price, seasonal and calendar effects", Destatis notes.

- Low equipment investment was arguably the most worrying part of German GDP over the past two years. Continued weak figures here would not bode well for productivity gains ahead. A recent private sector initiative, on balance, should be seen as a marginal net positive looking ahead.

- Today's flash release contains no commentary on the external sector, which saw elevated volatility amid global trade tensions in Q2. Final data will give more indication on contributions here.

- Destatis also highlights some partially material revisions to the GDP series - ranging from -0.6 to +0.5 percentage points since 2021 for the Q/Q readings on a seasonally adjusted basis. Q1 was 0.1pp weaker than previously seen (now 0.3% Q/Q), while Q4'24 was upwardly revised by 0.4pp to 0.2% Q/Q. More commentary here will follow with the final Q2 data (scheduled for August 22), Destatis mention.

- The Y/Y GDP comparison, at +0.4% when working day adjusted, was the highest reading since Q3'22 amid base effects (at least ahead of today's revisions).

- Expectations are for German growth to pick up in the quarters ahead. MNI's collation of sellside analysts sees headline GDP negative again in Q3 (-0.1% Y/Y), but accelerating then amid the government's fiscal push, to 0.3% in Q4 and 1.0% next year.

- Note that as part of this release the GDP series back to 2008 has been re-estimated.