FOREX: USD Index Erases Early Strength, EURGBP Extends Bounce

Aug-29 09:06

- Over the course of the European morning, the US Dollar has been edging lower, erasing the modest strength from overnight and briefly slipping into negative territory on the day. This has been most notable for USDJPY, falling around 30 pips from the 147.20 highs, placing the focus back on yesterday’s low of 146.66 and last Friday’s post Powell low at 146.58.

- EURUSD has traded in similar vein, grinding higher as the plethora of Eurozone inflation releases have failed to garner any bearish momentum. This keeps a more constructive tone present as we approach the important July PCE data out of the US, the MNI Chicago PMI and month end. Primary trend conditions remain bullish, however key resistance and the bull trigger remain further out at 1.1829, the Jul 1 high.

- In contrast, sterling weakness is standing out early Friday, helping EURGBP extend its recovery this week. A break above 0.8674 would signal a stronger reversal, placing the cross at its highest levels in three weeks.

- Although moves remain broadly contained, the Kiwi dollar sits atop the G10 leaderboard as NZDUSD extends its bounce from firm pivot support at 0.5800 to around a big figure. Bearish conditions overall for NZDUSD might suggest that good supply is seen into 50-day EMA resistance around 0.5930. The dovish RBNZ has seen the AUDNZD surge higher breaking back above 1.1000 convincingly. There have been some primary signs overnight of momentum stalling above 1.1100, however, look for dips back towards 1.1000/1.1030 to be supported.

- Elsewhere, USDCHF has once again dipped its toe back below the 0.8000 mark after reaching fresh one-month lows yesterday. Supportive but grinding price action for the swissie has seen EURCHF consolidate back below the 0.94 to current sot levels of 0.9350, very familiar territory for the cross in recent months. Swiss CPI is set for release next week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT AUCTION RESULTS: 3.75% Jul-52 Gilt Tender

Jul-30 09:06

| 3.75% Jul-52 Gilt | |

| Amount | GBP0.30bln |

| Avg yield | 5.383% |

| Bid-to-cover | 4.62x |

| Tail | 0.3bp |

| Avg price | 76.907 |

| Low price | 76.877 |

| Pre-auction mid | 76.848 |

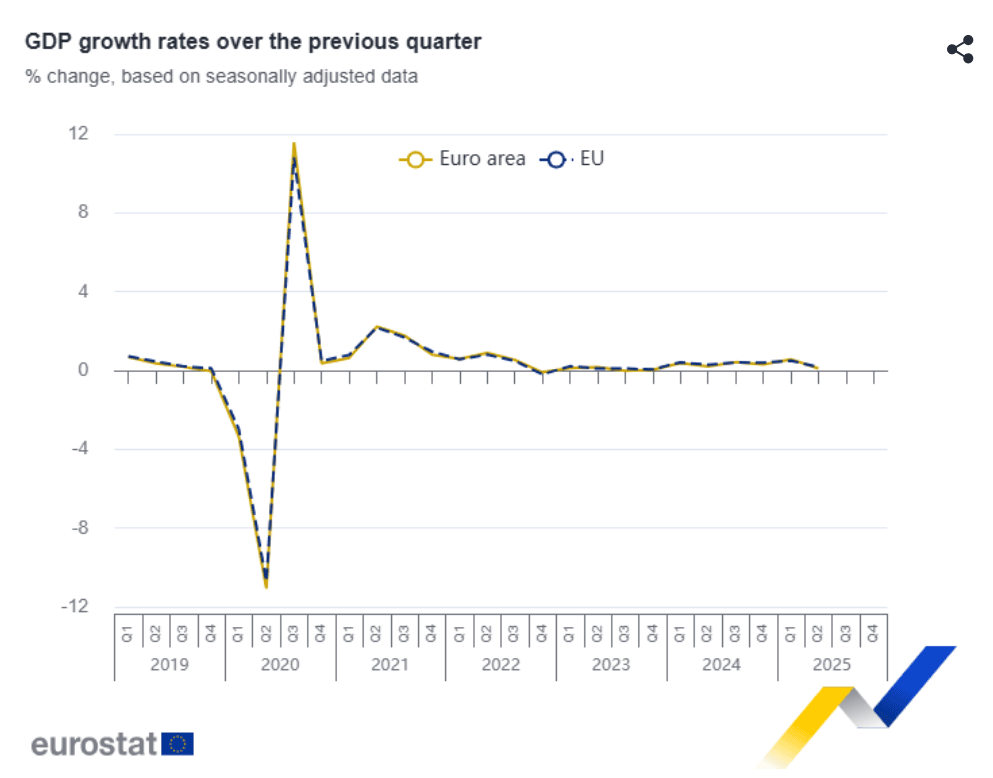

MNI: EUROZONE Q2 PRELIM FLASH GDP +0.1% Q/Q

Jul-30 09:00

- MNI: EUROZONE Q2 PRELIM FLASH GDP +0.1% Q/Q

- EUROZONE Q2 PRELIM FLASH GDP +1.4% Y/Y

EUROZONE DATA: Upside Risks To Q2 Eurozone GDP Materialize

Jul-30 09:00

Eurozone GDP printed 0.1% Q/Q in Q2, slightly stronger than consensus of 0.0% and slightly softer than the ECB's 0.2% staff projection. It was below Q1's outsized 0.6%.

- Ireland, which had a strong upward contribution in Q1, dragged the print lower this time at -1.0% Q/Q.

- Across the four major economies, detailed information on the Q1 data is lacking. Drivers across countries are mixed, with Germany mentioning stronger private and government consumption but weak investment, France seeing a material inventory contribution but weak domestic demand, while Italy and Spain both see positive domestic demand.

- Summarising the main quarterly GDP prints released yesterday/this morning:

- Eurozone: 0.1% Q/Q vs 0.0% cons, 0.6% prior.

- Germany: -0.1% Q/Q vs -0.1% cons, 0.3% prior.

- France: 0.3% Q/Q vs 0.1% cons, 0.1% prior.

- Italy: -0.1% Q/Q vs 0.1% cons, 0.3% prior.

- Spain: 0.7% Q/Q vs 0.6% cons, 0.6% prior.