MNI US OPEN - Fed Chair Interviews to Start Friday

EXECUTIVE SUMMARY

- BESSENT TO START FED CHAIR INTERVIEWS ON FRIDAY: WSJ

- REEVES CLAIMS “UK ECONOMY IS NOT BROKEN” AS 26 NOV BUDGET CONFIRMED

- GERMAN REVISION PULLS FINAL EUROZONE SERVICES PMI DOWN

- AUSTRALIA GDP GROWS 0.6% IN Q2

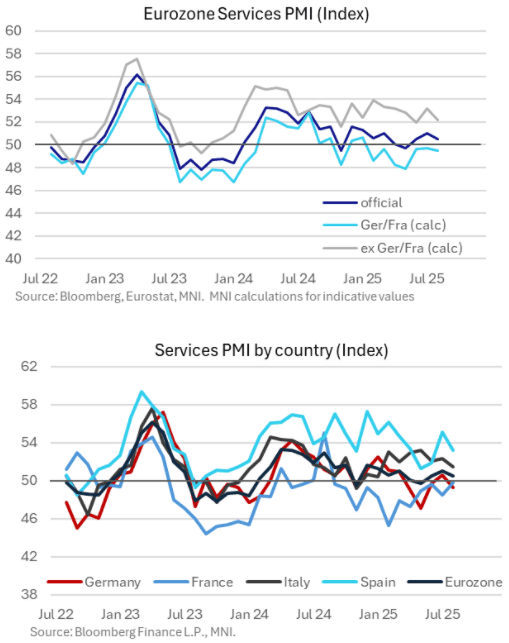

Figure 1: Eurozone final services PMI revised lower in August

NEWS

FED (WSJ): Bessent to Start Fed Chair Interviews on Friday

Treasury Secretary Scott Bessent is planning to start a blitz of interviews on Friday in search of a candidate to be the next chair of the Federal Reserve, according to people familiar with the matter. The interview process would continue next week, the people said, adding that Bessent would talk to candidates either in person or by video conference.

US/RUSSIA/CHINA/N.KOREA (BBG): Trump Accuses Xi of ‘Conspiring Against US’ With Putin, Kim

President Donald Trump took aim at Chinese leader Xi Jinping as he hosted foreign leaders at a major military parade in Beijing, a reminder of the lingering tensions between the two sides over trade, tech and other issues. “Please give my warmest regards to Vladimir Putin, and Kim Jong Un, as you conspire against The United States of America,” Trump said on his Truth Social site, referring to the leaders of Russia and North Korea, without elaborating.

US/JAPAN (BBG): Japan Trade Negotiator Akazawa to Visit US This Week: TV Tokyo

Japan’s top trade negotiator Ryosei Akazawa is arranging to visit the US as soon as this week, TV Tokyo reports, citing an unidentified official. Plans to meet Commerce Secretary Howard Lutnick by Monday and sign an agreement related to Japan’s investment in the US. Also aims for an executive order lowering auto tariffs to 15% to be issued.

UK (MNI): Reeves Claims “UK Economy Is Not Broken” as 26 Nov Budget Confirmed

In a video clip posted to X announcing the date of the budget (26 Nov), Chancellor of the Exchequer Rachel Reeves claims "Britain's economy isn't broken, but I do know that it's not working well enough for working people. Bills are too high and you feel that you're putting in but you're getting less out." Reeves: "...But there are still challenges. The cost of living pressures I know are still very real. We need to bring inflation and borrowing costs down. We do that by keeping a tight grip on day-to-day spending and by enforcing my non-negotiatble fiscal rules."

BOE (MNI): Four MPC Members to Testify Ahead of TSC This Afternoon

Four BOE MPC members will testify ahead of the Treasury Select Committee with regards to the August MPR on Wednesday. We will hear from Governor Bailey, Deputy Governor Lombardelli as well as external members Greene and Taylor. The main focus will be on Governor Bailey's remarks. We think that he is the key swing voter and his vote is likely a necessity if we are to see a November or December cut (which at the time of writing only had 5bp and 10bp cumulatively priced). Therefore any comments he makes on his views of the economy, the need for an imminent cut or the rationale for skipping a quarterly cut would be hugely important for the market.

ECB (BBG): ECB’s Next Move Could Be to Cut or Hike Rates, Dolenc Says

European Central Bank interest rates are firmly on hold for now and the next step could be a cut or hike, according to Primoz Dolenc, acting governor of Slovenia’s central bank. With Europe’s economy resilient and inflation stabilizing near 2%, Dolenc said he doesn’t see “major shifts in any direction” to justify changing borrowing costs this month.

EU (BBG): EU Pushes Ahead to Ratify Trade Deal With South American Nations

The European Union will publish the final text of its free-trade agreement with the South American economies of the Mercosur bloc Wednesday as it races to seal trade deals with like-minded partners in the face of renewed tensions with the US. The European Commission, which handles trade matters for the EU, will add additional safeguard measures to the deal which was provisionally agreed in December to appease critics, according to people familiar with the process.

FRANCE (BBG): Bayrou Open to Alternative Budget Plan If Deficit Target Remains

French Prime Minister Francois Bayrou said he remains open to alternative budget proposals as long as the overall deficit-reduction target remains in place. Bayrou has called a parliamentary vote of confidence for Monday and opposition parties holding a combined majority of seats in the National assembly have said that they plan to vote against the motion, which would force Bayrou to resign. “I am open to finding an approach that allows us to achieve the same goals without the drawbacks,” Bayrou, who only took office in December, said Wednesday in an interview with BFM TV.

HONG KONG (MNI EXCLUSIVE): HKD to Hold Firm on Mainland Equity Flows

MNI discusses the outlook for the Hong Kong dollar. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

JAPAN (BBG): Japan’s Ishiba Meets With Ueda to Discuss Economy, Markets

Japanese Prime Minister Shigeru Ishiba met with Bank of Japan Governor Kazuo Ueda to exchange views on the economy and financial markets including currencies, after the yen weakened amid rising pressure for Ishiba to resign. “As in the past, we exchanged general views on the state of the economy, prices and markets,” Ueda told reporters in Tokyo Wednesday, after meeting with Ishiba at the prime minister’s office. In response to reporters’ questions, Ueda added that the BOJ will raise rates if there are improvements in growth and prices in line with the central bank’s outlook, repeating his existing stance.

RBA (BBG): RBA Staff ‘Feeling the Weight’ of AI, Tech Shift, Governor Says

Reserve Bank of Australia staff are “feeling the weight” of its technological transformation agenda, Governor Michele Bullock said, adding that the use of big data and artificial intelligence has the potential to transform policy making. “We are exploring how technologies can enhance our understanding of economic conditions, improve forecasting and support more informed decision-making,” Bullock said in a lecture in Perth on Wednesday.

THAILAND (MNI): BJT Asks Speaker to Schedule PM Vote, PTP Seeks Parliament Dissolution

The Bhumjaithai Party (BJT) submitted a petition to House Speaker Wan Muhammad Noor Matha requesting an urgent meeting of parliament to elect a new Prime Minister after its leader Anutin Charnvirakul edged ahead in the race for the top job. Earlier in the day, Anutin signed an unprecedented confidence-and-supply pact with the People's Party (PPLA), which said it resolved to support his candidature under previously agreed conditions without joining his Cabinet. The Pheu Thai Party (PTP) promptly announced that caretaker Prime Minister Phumtham Wechayachai had sought royal approval of a dissolution of parliament.

OIL (RTRS): OPEC+ to Consider Further Oil Output Hike on Sunday, Sources Say

OPEC+ will consider further raising oil production at a meeting on Sunday, two sources familiar with the discussions said, as the group seeks to regain market share. Another boost would mean that OPEC+, which pumps about half of the world's oil, would be starting to unwind a second layer of output cuts of about 1.65 million barrels per day, or 1.6% of world demand, more than a year ahead of schedule.

DATA

EUROZONE DATA (MNI): German Revision Pulls Final Eurozone Services PMI Down

- EUROZONE AUG SERV PMI 50.5 (50.7 FLASH, 51.0 JUL)

- GERMANY AUG SERV PMI 49.3 (50.1 FLASH, 50.6 JUL)

- FRANCE AUG SERV PMI 49.8 (49.7 FLASH, 48.5 JUL)

The Eurozone final August services PMI was revised down a touch to 50.5 (vs 50.7 cons, 51.0 prior). This was mostly driven by Germany, which saw its services reading revised down to 49.3 (vs 50.1 flash). The composite reading was essentially unchanged from the flash at 51.0 (vs 51.1 flash, 50.9 prior) - a one-year high.

UK AUG SERV PMI 54.2 (53.6 FLASH, 51.8 JUL) (MNI)

SPAIN DATA (MNI): Services/Composite PMIs Weaker Than Exp, But Still Solid

- SPAIN AUG SERV PMI 53.2 (54.5 FCAST, 55.1 JUL)

The Spanish services PMI was weaker-than-expected at 53.2 (vs 54.5 cons, 55.1 prior), somewhat disappointing after a stronger-than-expected manufacturing reading on Monday. That left the composite PMI at 53.7 (vs 54.9 cons, 54.7 prior). The composite PMI has nonetheless been above 50 for 24 consecutive months now, underscoring Spain's position as the Eurozone growth outperformer post Covid.

ITALY DATA (MNI): August PMIs Still Expansionary But Momentum Slows

In a similar fashion to Spain, the Italian August services PMI was somewhat weaker-than-expected, but still expansionary, at 51.5 (vs 52.1 cons, 52,3 prior). The composite reading was above 50 for the seventh consecutive month at 51.7 (vs 51.6 cons, 51.5 prior). The details of the report point to weakening momentum amongst services producers in August, with growth still supported by domestic markets. Despite a rise in input costs, the report noted limited passthrough into output charges.

GERMANY DATA (MNI): July VDMA Machinery Orders Improve

Orders in German mechanical and plant engineering rose 4% Y/Y in July according to VDMA data. The print represents an improvement from June's -1%, a month which also has seen a 2.8% industrial production decrease and a 1.0% factory orders decline which contributed to the 0.2pp German Q2 GDP downward revision to -0.3% Q/Q. Note that July's truck toll index also pointed towards some recovery in industrial activity in the month, at +2.3% M/M (-0.8% June).

NORWAY DATA (MNI): Fall In Q2 Vacancy Rate But No Labour Demand Alarm Bells

The Norwegian vacancy rate fell to 2.7% in Q2, down from 3.0% in Q1 and 2.8% in Q4. It's the lowest rate since Q1 2021, though remains above the 2010-2019 average rate of 2.3%. As such, while there are some signs of softening labour demand, it's not yet a smoking gun for Norges Bank to deliver another rate cut in September. There's much more focus on next week's inflation and Regional Network Survey data.

SWEDEN DATA (MNI): Rebound in Services PMI Suggests July Was an Outlier

There was a solid rebound in the Swedish services PMI in August, rising to 53.4 after 49.0 in July and 54.6 in June. This suggests the July print was an outlier. The services reading follows an increase in the manufacturing PMI on Monday, and joins a broader set of improving Swedish activity indicators/signals from the past few weeks. That said, a Riksbank September cut remains on the cards if tomorrow's August flash CPIF print surprises to the downside.

AUSTRALIA DATA (MNI): Aussie Q2 GDP Grows 0.6%

- AUSTRALIA Q2 GDP +1.8% Y/Y

- AUSTRALIA Q2 GDP +0.6% Q/Q

Australia’s economy grew 0.6% q/q in Q2, 10 basis points above expectations and up from 0.3% in Q1, while unit labour costs rose 0.7%, according to National Accounts data released Wednesday by the Australian Bureau of Statistics. GDP per hour worked, a measure of productivity, increased 0.3% q/q and 0.2% y/y. “Economic growth rebounded in the June quarter following subdued growth in the March quarter, which was heavily impacted by weather events,” said Tom Lay, head of national accounts at the ABS.

TURKEY DATA (MNI): Annual Inflation Eases in August, Monthly Price Growth Remains Above 2%

- TURKEY AUG CPI +2.04% M/M

Annual inflation eased to +32.95% y/y in August from +33.52% in July, a touch above expectations of +32.59%. Monthly inflation was +2.04%, down marginally from +2.06% the previous month but above expectations of +1.75%. Food and non-alcoholic beverages prices rose 3% m/m, while alcoholic beverages and tobacco prices rose 6% m/m. Core CPI was broadly in-line with expectations at +33% y/y.

FOREX: JPY Underperforms for Second Session

- JPY is the poorest performer in G10 - as was the case ahead of the US open yesterday - as yawning yield spreads against the US and further stress in longer-end global yields favours USD/JPY. The pair crossed the 200-dma overnight at 148.86 - pierced for the first time since early August.

- GBP trades poorly again Wednesday, as the UK government confirmed the date of the Autumn Budget - November 26th - which should shift focus to potential policy leaks and trial balloons from the Chancellor as she looks to gauge market response to future plans to plug the hole in public finances, likely via further tax revenue raising measures (likely targeting property), although further speculation that the government could ditch their manifesto pledge of not raising national insurance, income tax or VAT rather than raising indirect taxes.

- The growing negative correlation between longer-end yields and GBP extending this morning. The recent drop in spot and renewed fiscal concerns are supporting a bid in vols: 3m implied has been marked higher to 8 points this morning, erasing the summer lull and returning above the YTD average of 7.8 points. This raises the risk of GBP/USD downside in the coming months, isolating 1.3144/42 as key support - the 38.2% retracement for the YTD upleg, as well as the August 1st low.

- Speaking in the Q&A following her speech on AI, tech and the Australian economy, RBA's Bullock states that the bank are starting to see the private sector show "a bit" more growth, and that spending has been a little stronger than the RBA thought. She adds that if this keeps going, the RBA might not need as many rate cuts - but don't know what wil happen at this stage.

- AUD edges to new session high on those comments - 0.6531 printed, but still well short of yesterday's best levels at 0.6559. Intraday resistance at 0.6530 pierced on the move. OIS markets continue to fully price a further rate cut by year-end, with 28bps of cuts priced for the December 9th RBA.

- US JOLTs data is the market focus for the US session - and as was the case for the ISM data yesterday, markets will be looking to gauge labour market strength into this Friday's payrolls report. Fed's Musalem is set to speak on the economy and policy ahead of the later release of the Beige Book, while BoE MPC members appear in front of the Treasury Select Committee at 1415BST/0915ET.

EGBS: 2.80% Handle in 10-year Bund Yield Holds Once Again

The 2.80% handle in the 10-year Bund yield has held once again, leaving yields -0.5bps at 2.78%. Today’s E5bln 10-year Bund supply was digested smoothly, with similar demand metrics to August’s auction.

- German yields are up to 1bp lower across the curve, with the 5-year lightly outperforming and recent bear steepening taking a breather. The broader steepening trend since 2023 remains intact though, with 5s30s currently up almost 70bps this year to 109.5bps.

- Bund futures are +12 ticks at 128.93, but remain shy of initial resistance at 129.42 (20-day EMA). That keeps risk tilted to the downside for now.

- 10-year peripheral EGB spreads to Bunds are up to 1.5bps tighter today, led by BTPs. OAT spreads are little changed, with ongoing French political uncertainty limiting any narrowing episodes.

- Lithuania is also holding at 10/20-year dual tranche syndication today.

- Eurozone final August services PMI’s weren’t major market movers, with the composite reading reaching a one-year high of 51.0 (vs 51.1 flash, 50.9 prior).

GILTS: Recovering From Lows

Gilts sold off on the open, with ongoing fiscal worry and some questions surrounding the future of Chancellor Reeves continuing to add weight.

- That was before a recovery in wider core global FI markets (note that U.S. 30s failed to break above 5.00%) provided support.

- Futures broke yesterday’s low (89.60) and Fibonacci support (89.46), basing at 89.36 before recovering to unchanged levels (~89.75). Bears remain in technical control, initial support and resistance of note now 89.22 & 90.16.

- Yields flat to 2bp lower on the day.

- 10s trade above 4.80%. January highs (4.921%) present the next upside target.

- 30-Year yields hit the highest level since the late ‘90s (5.748%) before the pullback. The 1.236 Fibonacci projection of the Jun 13-Jul 18-Aug 5 price swing (5.74%) was pierced. The next upside projection lies at 5.79%.

- Note that the Treasury has confirmed that the Budget will be released on 26 November, with Chancellor Reeves stressing that she doesn’t think the UK economy is broken.

- Final UK services PMI data was revised upwards.

- BoE-dated OIS shows ~9bp of cuts through Dec, little changed on the day. We continue to believe that the November meeting is much more “live” than the ~4bp priced into the market at present.

- SONIA futures flat to +1.0.

- BoE’s Bailey, Lombardelli, Taylor & Greene will appear in front of the Treasury Select Committee this afternoon.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Sep-25 | 3.973 | +0.6 |

Nov-25 | 3.923 | -4.3 |

Dec-25 | 3.879 | -8.8 |

Feb-26 | 3.785 | -18.2 |

Mar-26 | 3.750 | -21.7 |

Apr-26 | 3.685 | -28.2 |

EQUITIES: Tuesday's Pullback for E-Mini S&P Considered Corrective

The primary trend set-up in Eurostoxx 50 futures is bullish and the pullback from the Aug 22 high appears corrective. However, the contract has breached 5372.85, the 50-day EMA. The clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, initial resistance to watch is 5392.75, the 20-day EMA. A bull cycle in S&P E-Minis remains intact and the latest pullback is - for now - considered corrective. Price has traded through the 20-day EMA. The key support to watch lies at the 50-day EMA, at 6336.02. A clear break of this EMA is required to signal scope for a deeper retracement. This would open 6239.50, the Aug 1 low and a key support. Moving average studies still highlight a dominant uptrend. The bull trigger is 6523.00, the Aug 28 high.

- Japan's NIKKEI closed lower by 371.6 pts or -0.88% at 41938.89 and the TOPIX ended 32.99 pts lower or -1.07% at 3048.89.

- Elsewhere, in China the SHANGHAI closed lower by 44.576 pts or -1.16% at 3813.557 and the HANG SENG ended 153.12 pts lower or -0.6% at 25343.43.

- Across Europe, Germany's DAX trades higher by 131.7 pts or +0.56% at 23619.2, FTSE 100 higher by 34.78 pts or +0.38% at 9151.14, CAC 40 up 76.31 pts or +1% at 7730.4 and Euro Stoxx 50 up 45.24 pts or +0.86% at 5336.02.

- Dow Jones mini down 21 pts or -0.05% at 45330, S&P 500 mini up 24 pts or +0.37% at 6449.5, NASDAQ mini up 133.25 pts or +0.57% at 23408.25.

Time: 10:00 BST

COMMODITIES: Gold Remains in a Clear Bull Cycle

A bear cycle in WTI futures remains intact and the latest bull phase appears to be a correction. This short-term corrective cycle remains in play and Tuesday’s rally reinforces this theme. Initial resistance to watch is $66.56, the Aug 4 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. A resumption of weakness would pave the way for a move towards $57.71, the May 30 low. Gold remains in a clear bull cycle. This week’s gains have resulted in a breach of key resistance at $3500.1, the Apr 22 high, and delivered a fresh all-time high in the yellow metal. The break confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is the $3600.00 handle. Initial firm support to watch lies at $3396.2, the 20-day EMA.

- WTI Crude down $0.15 or -0.23% at $65.43

- Natural Gas down $0.03 or -1.1% at $2.976

- Gold spot up $7.24 or +0.2% at $3540.08

- Copper down $0 or 0% at $464.05

- Silver down $0.07 or -0.17% at $40.7962

- Platinum down $14.54 or -1.03% at $1396.04

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 03/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 03/09/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/09/2025 | 1300/0900 | St. Louis Fed's Alberto Musalem | ||

| 03/09/2025 | 1315/1415 | BOE testify at TSC: Bailey, Greene, Lombardelli, Taylor | ||

| 03/09/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/09/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 03/09/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 03/09/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/09/2025 | 1730/1330 | Minneapolis Fed's Neel Kashkari | ||

| 03/09/2025 | 1800/1400 | Fed Beige Book | ||

| 04/09/2025 | 0130/1130 | ** | Trade Balance | |

| 04/09/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 04/09/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 04/09/2025 | 0630/0830 | *** | CPI | |

| 04/09/2025 | 0700/0900 | ** | Unemployment | |

| 04/09/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/09/2025 | 0830/0930 | Decision Maker Panel data | ||

| 04/09/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/09/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 04/09/2025 | 0900/1100 | ** | EZ Retail Sales | |

| 04/09/2025 | 0930/1130 | ECB Cipollone Speaks at Digital Euro Hearing, European Parliament | ||

| 04/09/2025 | 1215/0815 | *** | ADP Employment Report | |

| 04/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 04/09/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 04/09/2025 | 1230/0830 | ** | Trade Balance | |

| 04/09/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 04/09/2025 | 1230/0830 | ** | Trade Balance | |

| 04/09/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 04/09/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 04/09/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 04/09/2025 | 1400/1000 | Fed nominee Stephen Miran | ||

| 04/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 04/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 04/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 04/09/2025 | 1600/1200 | ** | DOE Weekly Crude Oil Stocks | |

| 04/09/2025 | 1600/1200 | ** | US DOE Petroleum Supply | |

| 04/09/2025 | 1605/1205 | New York Fed's John Williams |