FOREX: JPY Underperforms For Second Session

Sep-03 09:26

- JPY is the poorest performer in G10 - as was the case ahead of the US open yesterday - as yawning yield spreads against the US and further stress in longer-end global yields favours USD/JPY. The pair crossed the 200-dma overnight at 148.86 - pierced for the first time since early August.

- GBP trades poorly again Wednesday, as the UK government confirmed the date of the Autumn Budget - November 26th - which should shift focus to potential policy leaks and trial balloons from the Chancellor as she looks to gauge market response to future plans to plug the hole in public finances, likely via further tax revenue raising measures (likely targeting property), although further speculation that the government could ditch their manifesto pledge of not raising national insurance, income tax or VAT rather than raising indirect taxes.

- The growing negative correlation between longer-end yields and GBP extending this morning. The recent drop in spot and renewed fiscal concerns are supporting a bid in vols: 3m implied has been marked higher to 8 points this morning, erasing the summer lull and returning above the YTD average of 7.8 points. This raises the risk of GBP/USD downside in the coming months, isolating 1.3144/42 as key support - the 38.2% retracement for the YTD upleg, as well as the August 1st low.

- US JOLTs data is the market focus for the US session - and as was the case for the ISM data yesterday, markets will be looking to gauge labour market strength into this Friday's payrolls report. Fed's Musalem is set to speak on the economy and policy ahead of the later release of the Beige Book, while BoE MPC members appear in front of the Treasury Select Committee at 1415BST/0915ET.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

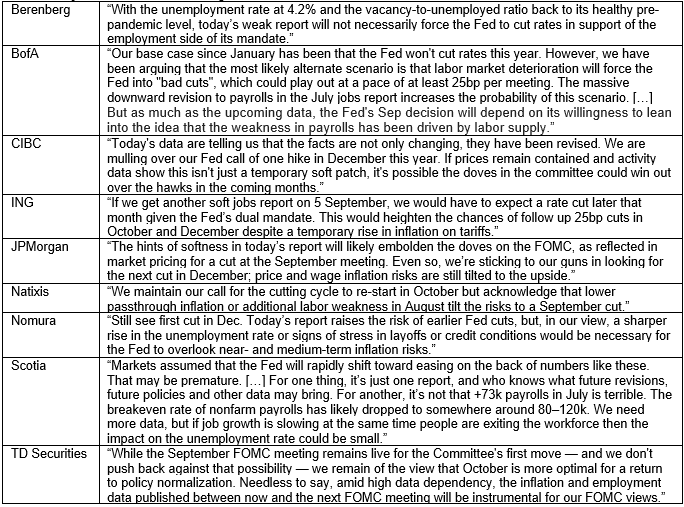

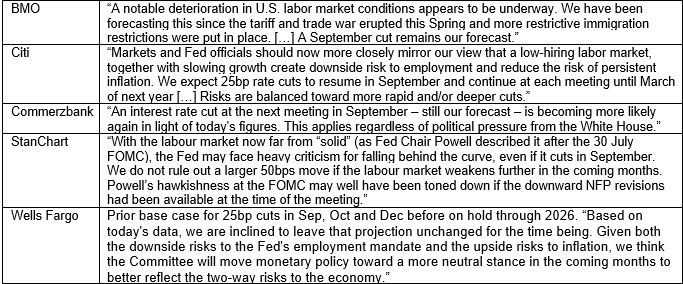

US OUTLOOK/OPINION: Analysts Less Convinced On Sept Cut Than Market [2/2]

Aug-04 09:17

Other Analyst Calls – Some Starting To Question More Hawkish Views

US OUTLOOK/OPINION: Analysts On Balance Less Convinced On Sept Cut [1/2]

Aug-04 09:17

- There has been a slight paring in expectations of cut at the next FOMC meeting on Sept 16-17 although there is still 21bp of easing priced vs 12bp before Friday's payrolls report.

- Analysts are less convinced at this stage, at least on balance. The five in the table below continue to expect a September cut (and we assume Goldman Sachs do as well but there wasn't reference in their data note) vs nine at least officially still looking for a later starting point for a resumption of cuts.

Analysts Calling For 25bp Cut In September – No View Changes But Standard Chartered Discuss 50bp

OIL: Lower, OPEC+ Production Questions Noted

Aug-04 09:06

Downside for crude this morning, with questions over the outlook for OPEC+ supply evident given the lack of firm guidance surrounding immediate future production plans after the latest output hike was ratified over the weekend (there is another round of production set to remain offline until late ’26).

- Both WTI and Brent are through Friday’s lows, with initial support located at the respective 50-day EMAs ($65.37 & $67.95).

- Our commodities team notes that excess supply fears have resurfaced but with focus also on the potential for Russian output disruption if restrictions are tightened (note Indian officials have shown little worry surrounding U.S. President Trump’s threats re: continued purchases of Russian oil).

- Background global growth worries and an uptick in the USD also apply weight this morning.

Trending Top

Jan-30 21:43

Jan-30 21:11