MNI US OPEN - Equity Backdrop Constructive to Start 2026

EXECUTIVE SUMMARY

- TRUMP SAYS US WILL ‘RESCUE’ PROTESTERS IN IRAN IF ATTACKED

- TRUMP & TAKAICHI TO HOLD CALL TODAY, KYODO REPORT

- BYD HITS SALES GOAL, SET TO TOPPLE TESLA AS BIGGEST EV MAKER

- SURPRISING FALL IN SPANISH MANUF PMI OFFSET BY RISE IN FUTURE CONFIDENCE

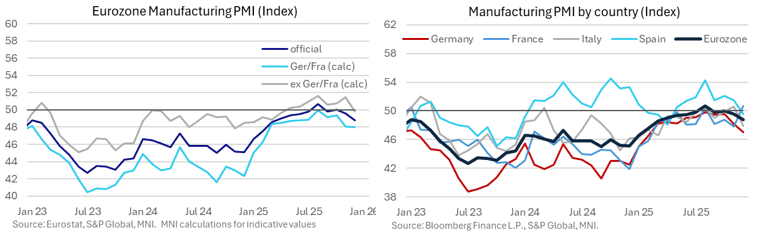

Figure 1: Downward Revision to Eurozone-Wide Manufacturing PMI for December

NEWS

US/IRAN (MNI): Pezeshkian Offers Economic Reforms Amid Escalating Protest Movement

Earlier today, US President Donald Trump threatened the Iranian gov't with the prospect of military action, saying that the US would come to the rescue of protesters in the country if Iranian forces continue to fire upon them. This marks a further escalation in Trump's rhetoric regarding Iran, after saying last week that the US could participate in airstrikes alongside Israel if Tehran resumes its nuclear and ballistic missile programmes. Secretary of the Supreme National Security Council Ali Larijani posts on X: "With the stances taken by Israeli officials and Trump, the behind-the-scenes of the matter has become clear. We consider the positions of the protesting merchants separate from those of the destructive elements, and Trump should know that American interference in this internal issue is equivalent to chaos across the entire region and the destruction of American interests. [...]"

US/JAPAN (MNI): Kyodo-Trump & Takaichi to Hold Call Today

Kyodo News reports that US President Donald Trump and Japanese PM Sanae Takaichi are expected to hold a telephone call today. According to gov't sources, the leaders may discuss potential dates for Takaichi's first visit to the US, which is expected to take place by March. The Japanese PM is looking to meet with Trump ahead of the US president's expected visit to China in April, given the deterioration in relations between Tokyo and Beijing in recent months amid heightened regional security tensions. As Nikkei Asia reports,"If U.S.-China ties warm, Japan risks being sidelined. Tokyo aims to leverage its strong relationship with Washington while also seeking a path to ease tensions with Beijing."

US (BBG): Mamdani Digs In on Progressive Agenda at NYC Mayor Inauguration

Zohran Mamdani unapologetically promised to lead New York City as a democratic socialist during a frigid inauguration ceremony on the steps of City Hall, a warning to those who believed he might moderate his positions after taking office. The nearly two-hour long event Thursday featured speeches by two of the US’s most liberal members of Congress, Representative Alexandria Ocasio-Cortez and Senator Bernie Sanders. New York Attorney General Letitia James, a frequent target of President Donald Trump, also had a speaking role. The ceremony served as a not-so-subtle statement of resistance to White House policies from the nation’s largest city.

CHINA (BBG): BYD Hits Sales Goal, Set to Topple Tesla as Biggest EV Maker

BYD Co. met its full-year sales target and likely surpassed Tesla Inc. to become the world’s largest electric-vehicle maker in 2025 — a milestone overshadowed by a challenging outlook for the Chinese auto market in the year ahead. The Chinese EV giant’s Hong Kong-listed shares rose on the first day of trading for the new year, gaining as much as 2.3%. The Shenzhen-based carmaker delivered 4.6 million vehicles last year, up 7.7% from 2024. That’s in line with a lowered full-year goal the company gave in September. Among the mix, it sold almost as many fully-electric vehicles — 2.3 million — as it did plug-in hybrids.

CHINA (BBG): DeepSeek Touts New Training Method as China Pushes AI Efficiency

DeepSeek published a paper outlining a more efficient approach to developing AI, illustrating the Chinese artificial intelligence industry’s effort to compete with the likes of OpenAI despite a lack of free access to Nvidia Corp. chips. The document, co-authored by founder Liang Wenfeng, introduces a framework it called Manifold-Constrained Hyper-Connections. It’s designed to improve scalability while reducing the computational and energy demands of training advanced AI systems, according to the authors.

S.KOREA (BBG): BOK’s Rhee Sees ‘Misaligned’ Won, Vows to Guard FX Stability

Bank of Korea Governor Rhee Chang Yong said the recent won weakness doesn’t reflect the real strength of the country’s economy, and he vowed to oppose any US investment decisions that could threaten the stability of the foreign-exchange market. “While it is difficult to identify a precise appropriate exchange rate level, the recent rise into the upper 1,400s appears to be substantially misaligned with our economic fundamentals,” Rhee said in a New Year’s speech on Friday.

MIDEAST (MNI): Saudi-Backed Forces Launch Strikes in Yemen Amid Rift w/UAE

The ongoing conflict in Yemen, which has significantly strained relations between Saudi Arabia and the UAE in recent weeks, continues to escalate. The Southern Transition Council (STC), supposedly backed by the UAE, has confirmed that one of its camps in southern Yemen has been targeted by Saudi airstrikes. Comes amid the Governor of Hadramout governorate, Salem Ahmed Saeed al-Khunbashi, being given powers by the Saudi-backed Presidential Leadership Council (PLC) to take back military sites in the region that have been taken by the STC in a recent military campaign. The PLC said the instructions did not amount to a 'declaration of war'.

DATA

EUROZONE DATA (MNI): Unsurprising Downward Revision to Dec Manuf PMI; Two Way Risks In

- EUROZONE DEC FINAL MANUF PMI 48.8 (49.2 FLASH, 49.6 NOV)

- GERMANY DEC FINAL MANUF PMI 47.0 (47.7 FLASH, 48.2 NOV)

- FRANCE DEC FINAL MANUF PMI 50.7 (50.6 FLASH, 47.8 NOV)

The downward revision to the Eurozone December manufacturing PMI doesn't come as a surprise after this morning's country-level readings. We estimate the Germany/France manufacturing PMI was revised down to 48.0 (vs 48.5 flash, 48.1 prior), driven by the German reading. Meanwhile, the ex-Germany/France reading saw a smaller downward revision to 49.8 (vs 50.1 cons, 51.5 prior). The Eurozone manufacturing industry faces two-way risks this year. On the positive side, increases in German spending and an anticipated broader recovery in regional consumption may support industrial demand. However, continued Chinese import penetration (exacerbated by the competitive level of the yuan) and the impact of higher US tariffs present ongoing headwinds. Progress on the Russia/Ukraine peace deal also remains an area of high uncertainty.

SPAIN DATA (MNI): Surprising Fall in Dec Manuf PMI Offset by Rise in Future Confidence

- SPAIN DEC MANUF PMI 49.6 (51.2 FCAST, 51.5 NOV)

The Spanish manufacturing PMI surprisingly fell into contractionary territory in December (49.6 vs 51.2 cons, 51.5 prior). This was the lowest (and first sub-50) reading since April. Although the details point to weak demand trends in December, the uptick in year-ahead confidence provides some offset. Spain has been the Eurozone economic outperformer across the last two years, and current Bloomberg consensus looks for that to continue in 2026 - albeit by a smaller margin than in 2025.

ITALY DATA (MNI): Dec Manuf PMI Sees Similar Themes to Spain; Weak Growth a Concern in '26

- ITALY DEC MANUF PMI 47.9 (50.1 FCAST, 50.6 NOV)

The Italian December manufacturing PMI was very similar to Spain. The headline index surprisingly retreated into contractionary territory (47.9 vs 50.1 cons, 50.6 prior), but year-ahead confidence ticked up. Italian growth is expected to increase only slightly to 0.7% Y/Y in 2026, versus an expected 0.6% in 2025. We've previously written that while continued fiscal consolidation is positive for Italy's own macroeconomic balances and the relative performance of BTPs, the country's weak growth outlook presents an ongoing headwind.

UK DATA (MNI): Downward Revision to Dec Manuf PMI, Continued Job Losses Noted

- UK DEC FINAL MANUF PMI 50.6 (51.2 FLASH, 50.2 NOV)

Downward revision to the UK December manufacturing PMI to 50.6 vs 51.2 flash, albeit still above November's 50.2. While there were increases in both production and new orders in December, it's not signalling a meaningful increase in demand. Meanwhile, employment levels are still falling, even if the rate of decline has eased.

SWEDEN DATA (MNI): Manufacturing PMI Remains Solid

The Swedish manufacturing PMI remains solid, printing at an expansionary 55.3 in December (vs 54.7 prior). In recent months, the Economic Tendency Indicator's manufacturing sentiment series has begun catching up to the PMI, the latter of which has been above 50 since mid-2024. PMI details show increases in new orders to 57.0 (vs 56.7 prior) and production to 58.5 (vs 57.6 prior). Inventories fell to 47.6 (vs 49.9 prior), which is a positive forward-looking signal when taken alongside the new orders rise.

ASIA DATA (MNI): South Korea, Taiwan PMIs Above 50.0, Supporting Broader Trade Outlook

EM Asia PMIs for Dec mostly ticked up relative to Nov outcomes, per the S&P global measures. Notably the South Korean measure rose to 50.1 from 49.4 in Nov, while Taiwan's rose to 50.9 from 48.8 prior. For both economies this is short of 2025 highs, but well up on earlier lows. The improvement in the PMI readings bodes well for the

broader global trade outlook, although trade growth didn't slow materially as 2025 unfolded (despite negative sentiment via these surveys readings). Elsewhere in the region, Indonesia's PMI ticked down to 51.2 from 53.3 in Nov, so weaker but still remaining above the expansion/contraction line. The Philippines rose to 50.2 from 47.4, a positive sign after weaker H2 growth in 2025 as conditions were weighed by the mid year corruption scandal. Malaysia's PMI was unchanged at 50.1.

FOREX: AUDUSD Rises Back to 0.6700 Amid Equity Strength

- A solid rally for the major equity benchmarks to start the year has propelled AUD to the top of the G10 FX leaderboard this morning, with AUDUSD rising ~0.4%. With the notable bounce, spot has returned to pre-Christmas levels around the 0.6700 handle, maintaining the supportive tone that was on display throughout December. Recent clearance of a key resistance point at 0.6707 (Sep 17 high) confirms a resumption of the medium-term uptrend that started Apr 9. This signals scope for an extension towards 0.6759 next, the Apr 11 2024 high.

- The Euro is the main underperformer in G10 this morning following downward revisions in the Eurozone December Manufacturing PMI. Attempts above the 1.1800 handle across December have proved short-lived, with the pair tracking back towards 1.17 at typing. The breach of the 20-day EMA at 1.1724, will be monitored as a clear break would signal scope for a deeper retracement, allowing an overbought condition to unwind.

- Over the holiday period, USDJPY has unsurprisingly traded in a more contained manner, broadly respecting a 156.00-157.00 range. Topside momentum stalled at 157.00 this morning for a second time this week, however, spot continues to hover close to recent highs. Moving average studies highlight a dominant uptrend, with attention remaining on 157.89, the Nov 20 high and the bull trigger.

- Today's data calendar is light, with the final December US Manufacturing PMI not expected to move the needle, but Fed's Paulson and Kashkari scheduled to speak over the weekend. Both of them are under elevated scrutiny as they newly come into rotation of FOMC voters with the start of the new year.

BONDS: Bunds Move Away From Session Lows Alongside USTs, Gilts Underperform

Bund futures have climbed off session lows alongside UST counterparts, currently -11 ticks at 127.46 (vs lows of 127.08) on solid volumes of over 300k today. The overall technical setup in the contract remains bearish, with initial firm resistance at 127.86, the 20-day EMA. A break of this average would signal the start of a stronger correction.

- Headline flow has been relatively light, save for US President Trump issuing a warning to Iran on the treatment of peaceful protestors.

- Recent cross asset moves have seen European equity futures move away from highs and crude futures bounce a little from session lows.

- The Eurozone December manufacturing PMI was revised down to 48.8 (vs 49.2 flash), following a downward revision in Germany and weaker-than-expected readings in Spain and Italy.

- BTPs underperform EGB peers, with the spread to Bunds up 2bps to ~71.5bps.

- Slovenia has issued a mandate for a new 10-year SLOREP transaction, likely to be held early next week.

- Gilt futures are -22 ticks at 91.15. First support is 90.50, with resistance located at 91.78.

- The 10-year Gilt/Bund spread is 1.5bps wider at ~163bps, with 10-year Gilt yields up 1.5bps and Bund yields little changed. Both the German and UK curves have steepened, alongside Treasuries.

- The UK manufacturing PMI was revised down to 50.6 (vs 51.2 flash).

- The remainder of today's calendar is light, with US manufacturing PMIs due this afternoon.

EQUITIES: Bull Cycle in Eurostoxx Futures Intact, Contract Close to Cycle Highs

A bull cycle in Eurostoxx 50 futures remains intact. The first key support to watch lies at 5691.88, the 50-day EMA. A clear break of the EMA would highlight a potential short-term reversal. This would open 5622.00, the Nov 26 low. For bulls, sights are on key resistance at 5847.00, the Nov 13 high. The price pattern on Dec 18 is a bullish engulfing candle - a reversal signal. Short-term weakness in S&P E-Minis appears corrective. A key short-term support has been defined at 6771.50, the Dec 18 low. A break of this level is required to signal scope for a deeper retracement and would highlight a possible short-term reversal. For bulls, sights are on key resistance at 7014.00, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the primary uptrend.

- Across Europe, Germany's DAX trades higher by 121.47 pts or +0.5% at 24611.34, FTSE 100 higher by 61.57 pts or +0.62% at 9992.51, CAC 40 up 44.71 pts or +0.55% at 8195.05 and Euro Stoxx 50 up 45.71 pts or +0.79% at 5838.03.

- Dow Jones mini up 182 pts or +0.38% at 48518, S&P 500 mini up 44.5 pts or +0.65% at 6937, NASDAQ mini up 276 pts or +1.08% at 25731.75.

Time: 10:00 GMT

COMMODITIES: Trend Condition in WTI Futures Remains Bearish

The trend condition in WTI futures remains bearish and gains are considered corrective - for now. MA studies are in a bear-mode position, highlighting a dominant downtrend. A key support and the bear trigger at $56.11, the Oct 17 low, has recently been breached. The break highlights a continuation of the downtrend and opens $53.77, a Fibonacci projection. Key S/T resistance is $61.25, the Oct 24 high. First resistance is at $58.56, the 50- day EMA. The trend structure in Gold is unchanged, it remains bullish and the sharp sell-off earlier this week appears corrective - for now. The trend is overbought and a deeper retracement would allow this condition to unwind. First support at $4324.8, the 20-day EMA, has been pierced. A clear break of the average would expose the 50-day EMA at $4183.5. For bulls, a resumption of gains would open $4578.3, a Fibonacci projection.

- WTI Crude down $0.23 or -0.4% at $57.17

- Natural Gas down $0.08 or -2.09% at $3.609

- Gold spot up $68.16 or +1.58% at $4388.51

- Copper up $4.75 or +0.84% at $572.95

- Silver up $2.8 or +3.91% at $74.5023

- Platinum up $68.89 or +3.34% at $2130.63

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 02/01/2026 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 03/01/2026 | 1930/1430 | Philly Fed's Anna Paulson | ||

| 04/01/2026 | 1730/1230 | Minneapolis Fed's Neel Kashkari |