EUROZONE DATA: Dec Manuf PMI: Unsurprising Downward Revision; Two Way Risks In

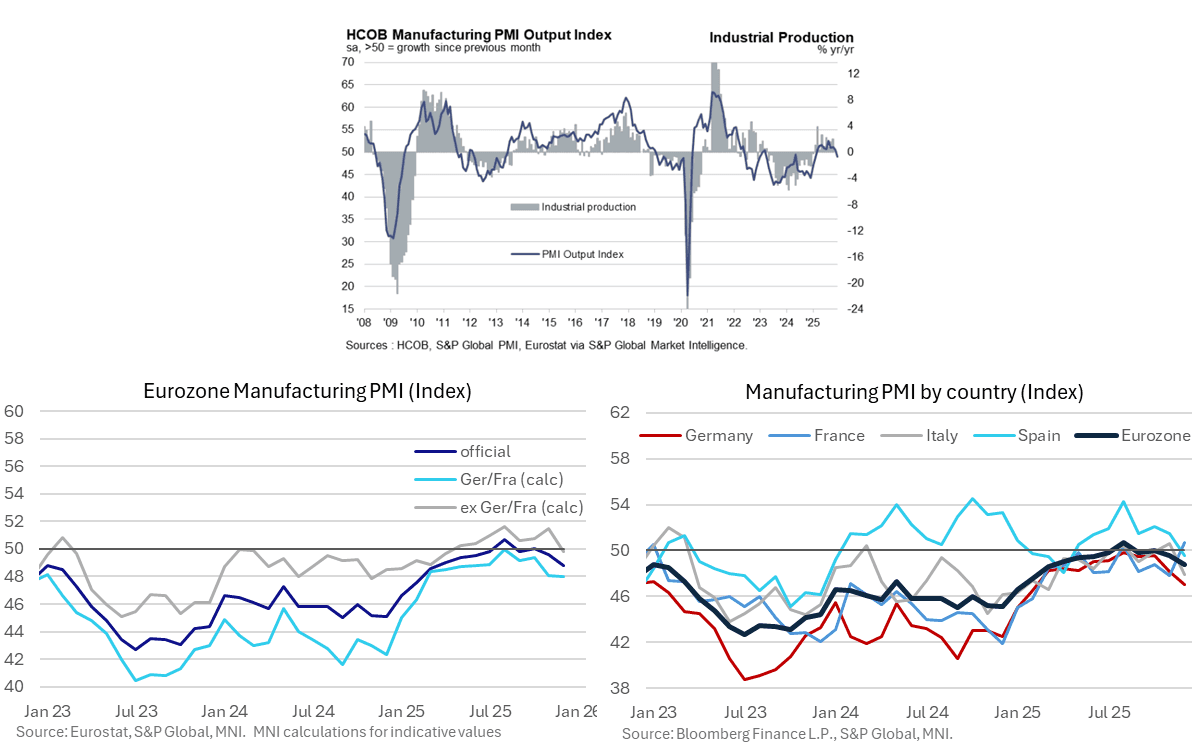

The downward revision to the Eurozone December manufacturing PMI doesn’t come as a surprise after this morning’s country-level readings.

- MNI: EUROZONE DEC FINAL MANUF PMI 48.8 (49.2 FLASH, 49.6 NOV)

We estimate the Germany/France manufacturing PMI was revised down to 48.0 (vs 48.5 flash, 48.1 prior), driven by the German reading. Meanwhile, the ex-Germany/France reading saw a smaller downward revision to 49.8 (vs 50.1 cons, 51.5 prior).

The Eurozone manufacturing industry faces two-way risks this year. On the positive side, increases in German spending and an anticipated broader recovery in regional consumption may support industrial demand. However, continued Chinese import penetration (exacerbated by the competitive level of the yuan) and the impact of higher US tariffs present ongoing headwinds. Progress on the Russia/Ukraine peace deal also remains an area of high uncertainty.

Notes from the Eurozone-wide release:

- “After nine successive months of growth, factory production volumes across the eurozone decreased in December. The decline was only mild overall, however. Pulling output lower was an accelerated fall in new order intakes. The latest deterioration in sales performances – the second in as many months – was also the sharpest since the beginning of 2025. Exports drove total new business volumes lower, sub-index data showed, with demand from international clients decreasing at the fastest rate in 11 months”

- “Notably, there was growing evidence of supply-chain pressure for eurozone manufacturers. Average lead times on items purchased from vendors lengthened to the greatest extent since October 2022”….”Stronger cost pressures did not dissuade eurozone factories from discounting their goods prices. Charges fell for the seventh time over the last eight months during December.”

- “As for employment, factory job losses were extended into the final month of 2025, stretching the current sequence of decrease to just over two-and-a-half years”

- “Lastly, manufacturers’ sentiment towards the year-ahead outlook for production improved in December.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

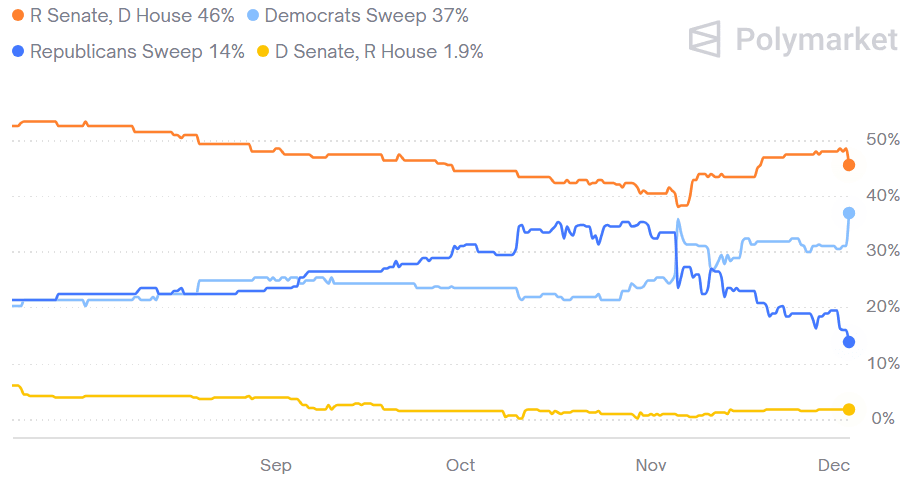

US: Tennessee Special Elections Adds To Democrats' Midterm Optimism

Republican Matt Van Epps won a special election in Tennessee’s 7th Congressional District. While the GOP avoided a shock loss - which appeared possible following a Democratic overperformance at off-year elections in November - the narrow margin of victory will increase Democratic optimism of flipping the House in 2026.

- Van Epps defeated Democratic state Rep. Aftyn Behn by a reported margin of 9 percentage points - considerably closer than the 20-plus percentage points margin of former Republican Rep. Mark Green and President Trump in 2024.

- Ahead of the election, we noted a Van Epps win within five percentage points would “increase GOP anxiety that the party is heading for a midterm wipeout”. See: US: Democrats Downplay Prospect Of Shock Win In Tennessee Special Election

- While that was avoided, the underperformance prompted Polymarket to upgrade the implied probability of Democrats sweeping Congress in 2026 to 37%. CNN notes, “Democrats appear to be performing better electorally than they did in 2017. And Democrats went on in 2018 to win back the US House in a “wave” election.”

- Data from NYT shows every single county in the district shifted towards Democrats, suggesting weakness across Trump’s base. The result is consistent with four other special elections this year, which Democrats have overperformed 2024 by an average of 16 points (and Kamala Harris by 18 points).

- Democratic optimism should be tempered by the imperfect predictive nature of special elections: Turnout tends to be low, putting a higher premium on voter enthusiasm, which appears to favour Democrats right now, especially with Trump off the ballot.

Figure 1: 2026 Balance of Power

Source: Polymarket

FOREX: FX OPTION EXPIRY

Of note:

EURUSD 1.87bn at 1.1600/1.1625.

USDJPY 1.27bn at 155.50.

EURUSD 2.18bn at 1.1600 (thu).

AUDUSD 1.11bn at 0.6500 (fri).

- EURUSD: 1.1600 (611mln), 1.1610 (310mln), 1.1625 (948mln).

- USDJPY: 155.00 (805mln), 155.50 (1.27bn), 156.25 (400mln).

- NZDUSD: 0.5730 (621mln).

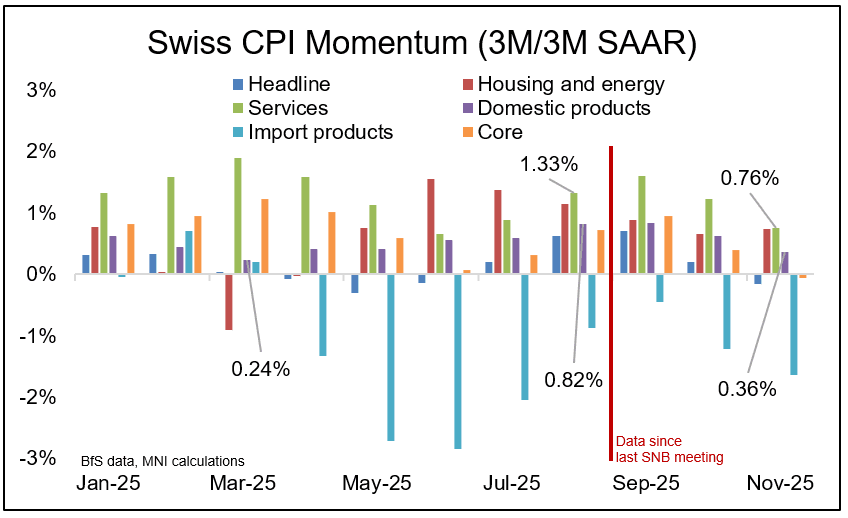

SWITZERLAND DATA: Seasonal Adjusted CPI Data Shows Services, Domestic Above Lows

A rough seasonal adjustment of Swiss CPI data shows momentum in much eyed services and domestic categories remaining above their respective cycle lows despite some downside since the last SNB meeting in September. This supports the narrative that there is some room for further inflation downside before the SNB felt pressured to cut into negative territory.

- We calculate momentum as a 3m/3m annualized rate. For services, this stands at 0.76% (vs 1.33% before the SNB September meeting), and 0.36% for domestic inflation (vs 0.82% before the Sep meeting).