MNI US OPEN - China Says Still No Trade Talks With US

EXECUTIVE SUMMARY

- US OFFICIALS MULL EASING TARIFFS TARGETING THE AUTO INDUSTRY

- US & CHINA HAVE NOT HELD TARIFF CONSULTATIONS

- FED’S HAMMACK SAYS NOT A TIME TO BE PREEMPTIVE

- ECB MUST BE AGILE AND SHOULDN’T RULE OUT LARGER CUT, REHN SAYS

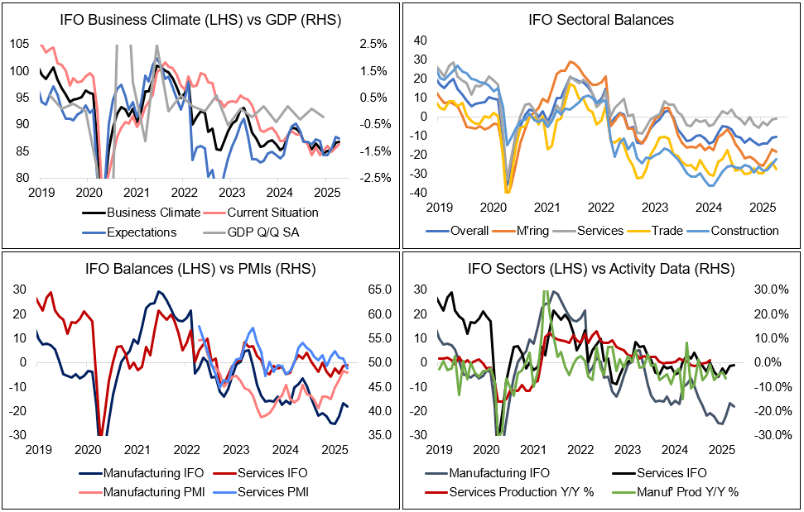

Figure 1: German IFO unexpectedly rises in April on services uptick

NEWS

US (BBG): US Officials Mull Easing Tariffs Targeting the Auto Industry

The Trump administration is considering whether to reduce certain tariffs targeting the auto industry that carmaker executives have warned would deal a severe blow to profits and jobs. One measure would spare automobiles and parts already subject to tariffs from facing additional duties from levies on steel and aluminum imports, according to people familiar with the matter. That would eliminate so-called “stacking” of levies.

US/CHINA (MNI): US & China Have Not Held Tariff Consultations - China FM Spox

MNI (London) Chinese Foreign Ministry spox Guo Jiakun speaking in a daily press conference says that China and the US "have not held consultations and negotiations on tariffs", adds that "respect is [a] condition for any talks to happen", and "[China] will fight [a] tariff war if we must." Says that the US "needs to stop threats if it wants talks". Claims that the "US 'tariff tsunami' breaks WTO rules." The comments come after US President Donald Trump implied on 23 April that talks may be underway, or close to underway.

US/JAPAN (BBG): Japan’s Kato Wants to Base US Talks on Existing FX Pacts

Japan’s Finance Minister said that he wants to base upcoming talks with US Treasury Secretary Scott Bessent on existing agreements on currencies, after Bessent said that the US won’t be seeking any specific currency targets with Japan. “Currencies should be determined by the market, and excessive or disorderly moves can have negative impacts on economies and financial stability,” Katsunobu Kato told reporters in Washington late Wednesday. “This is a basic principle that’s shared among the Group of Seven including the US, and I want to hold talks based on this basic understanding.”

FED (MNI): Not a Time to Be Preemptive - Fed’s Hammack

The economic outlook is too uncertain for the Federal Reserve to make any near-term shifts in monetary policy, Cleveland Fed President Beth Hammack said Wednesday. “This is not a good time to be preemptive,” Hammack said. “This is a good time to sit and wait and watch and see how the data is coming in so we get better clarity on what the right course of action is. I would rather be slow and move in the right direction than be fast and move in the wrong direction.”

FED (MNI): High Bar for Market Intervention - Fed’s Hammack

The Federal Reserve must keep a very high bar for any possible market intervention in times of turmoil that is reserved for a full-on breakdown in market functioning of the kind seen in 2008 or 2020, Cleveland Fed President Beth Hammack said Wednesday. “There has to be an incredibly high bar for the Fed to step in and say, things aren’t working, we need to be there to support it. I personally don’t think we’ve seen anything like that at this point in time,” Hammack told investors at an event in New York.

UKRAINE (MNI): Zelenskyy to Curtail South Africa State Visit After Kyiv Missile Attack

Ukrainian President Volodymyr Zelenskyy has confirmed that he will be curtailing his visit to South Africa following a massive Russian missile attack overnight, centred on Kyiv, that has killed at least nine. In a post on X, Zelenskyy says "I am canceling [sic] part of the program for this visit and will return to Ukraine immediately after the meeting with the President of South Africa." Following the hardline comments aimed at the Zelenskyy administration from both US President Donald Trump and VP JD Vance on 23 April, Kyiv appears to be in the position of either taking the 'Trump peace plan' offer, resulting in the ceding of significant portions of land in the east and south, or looking to fight on but potentially only with the military and financial support of its European allies.

ECB (BBG): ECB Must Be Agile and Shouldn’t Rule Out Larger Cut, Rehn Says

The European Central Bank will probably have to lower interest rates further and shouldn’t exclude a larger reduction, according to Governing Council member Olli Rehn. While “pervasive uncertainty” stemming from geopolitics and trade requires officials to keep an open mind on next steps, Rehn warned that financing conditions have tightened recently and risks to economic growth have begun to be realized. “It’s really important that we maintain full freedom of action, implying that we don’t define certain thresholds because of an assumed neutral rate, and we don’t a priori rule out a certain size of rate cut either,” he said. “This is a time for agile and active monetary policy.”

UK (BBG): Bailey Warns of Tariffs Hit to UK Ahead of BOE Forecasts

Bank of England Governor Andrew Bailey warned that the US-led trade war would harm the UK economy despite preferential treatment on tariffs, after a gauge of private sector activity showed a steep drop due to President Donald Trump’s global levies. Speaking at an Institute of International Finance event in Washington little more than two weeks before the bank unveils its latest economic forecasts, Bailey accepted that the UK had so far fared better than others on tariff levels. But he said that being an open economy exposed it to the global effects of a trade war.

UK/EU (FT): UK and EU to Finalise Plans for Defence Pact

Sir Keir Starmer and Ursula von der Leyen will on Thursday finalise plans for a new UK/EU defence pact and an agreement on the sensitive area of fishing rights, paving the way for negotiations on a broader economic deal. The British prime minister and European Commission president are expected to announce a defence and security pact and a rollover of current fishing arrangements at a summit on May 19.

CHINA (MNI): China to Open Up, Support Free Trade - PBOC's Pan

MNI (Beijing) China will continue to open up its economy and to support free trade rules and the multilateral trading system, said People’s Bank of China Governor Pan Gongsheng, PBOC-run newspaper Financial News reported Thursday. China will promote inclusive economic globalisation and maintain global financial stability, Pan said during the G20 Finance Ministers and Central Bank Governors Meeting in Washington, calling for efforts to prevent the global economy from sliding onto a track of “high friction and low trust”.

CHINA (BBG): Chinese Firms Rush to Announce Buybacks as Tariff War Deepens

Buyback plans announced in China this month have reached the most since a stock rout in February 2024, a sign that companies are putting in concerted effort to offset the market impact from US tariffs. Share repurchases pledged by 139 companies in Shanghai and Shenzhen amounted to 44.1 billion yuan ($6 billion) as of Thursday, according to exchange data compiled by Bloomberg. Such proposals, along with exchange-traded fund purchases by state funds, have helped soothe investor sentiment.

JAPAN (BBG): Japan’s Biggest Life Insurer to Reduce Its Yen-Bond Holdings

Japan’s largest life insurer plans to reduce its holdings of the nation’s sovereign bonds, even as higher yields have attracted more domestic buyers and overseas investors to the haven asset. Nippon Life Insurance Co. said that after making purchases at a brisk pace earlier this month, buying will now steady and that on a book value basis, its holdings of the debt will drop this fiscal year for the first time since the 12 months ended March 2017.

SOUTH AFRICA (MNI): Treasury Ditches VAT Hike, Seeks Alternative Revenue Sources

The National Treasury backed down after weeks of infighting that took the ruling coalition to the brink of collapse and declared last night that it would table a bill scrapping the proposed 0.5pp VAT hike that was supposed to take effect from May 1. It said in a statement that 'the decision to forgo the increase follows extensive consultations with political parties, and careful consideration of the recommendations of the parliamentary committees.' As recently as a few days ago, Finance Minister Enoch Godongwana insisted that there were no alternatives to the measure and that it could not be reversed in time. At the same time, the Democratic Alliance (DA) said that the Treasury asked it to drop its lawsuit seeking to indict the implementation of the VAT increase.

DATA

GERMAN DATA (MNI): IFO Unexpected Uptick on Services/Current Situation

- GERMANY APR IFO BUSINESS CLIMATE INDEX 86.9

Germany's IFO Business Climate Index unexpectedly rose in April, to 86.9 (from 86.7 Mar), stronger than consensus (85.2) despite firmer US tariff policies which were expected to drive the index downwards. The print also surprises in terms of the services sector, where sentiment improved - contrary to yesterday's Services flash PMI release. The current assessment reading was the upside driver this month, at 86.4 (vs 85.4 cons; 85.7 prior); expectations deteriorated to 87.4 but remained above expectations (85.0 cons; 87.7 prior). Across sectors, in manufacturing, more pessimistic expectations filtered through to a weaker overall reading - this appears sensical amid the US tariff developments in April. Uncertainty is particularly elevated in the sector, IFO comments.

FRANCE APR CONSUMER SENTIMENT 92 (MNI)

JAPAN DATA (MNI): March Services PPI Rises 3.1% vs. Feb 3.2%

- JAPAN MARCH SERVICES PPI +3.1% Y/Y; FEB REV +3.2%

- JAPAN MARCH SERVICES PPI +0.7% M/M: FEB REV +0.1%

Japan’s services producer price index rose 3.1% y/y in March, decelerating from February’s revised 3.2%, showing that corporate pass-through of cost increases remained solid, preliminary data released by the Bank of Japan on Thursday showed. The March index was lowered by leasing and rental (+2.4% vs. +3.3%) and transportation and postal services (+3.1% vs. +3.3%), although advertising services rose 2.7% vs. +1.6%. The SPPI rose 0.7% m/m in March after rising 0.1% in February.

FOREX: Greenback Edges Lower as China Dismisses Talks Progress

- Risk sentiment is trading on a softer footing Thursday amid headlines from China dismissing any progress on trade talks with the US. The messaging goes against the most recent optimism surrounding potential de-escalation of the tariff war, and have placed the US dollar under pressure through the European morning. Greenback losses have been broad based in the G10 space, with the dollar only higher against CNH.

- These dynamics have boosted EURUSD by 0.55% with 1.13 providing solid support so far and the move down from Monday’s cycle high considered corrective. Moving average studies are in a bull-mode position which continues to signal a continued dominant uptrend. Most recent comments from ECB’s Rehn highlighting “there are few good arguments” to pause rate cuts lean dovish but have had little effect on the Euro. 1.1573/1.1181 remain the short-term technical parameters of note.

- Despite the upticks for both AUDUSD (+0.35%) and NZDUSD (+0.56%), the pairs remain notably below the 0.6400 and 0.6000 marks respectively. For AUDUSD specifically, the inability to consolidate gains above key resistance at 0.6409 is significant, and evident of the how fragile the pair remains to the broader risk backdrop.

- USDCHF highs of 0.8311 overnight fell around 20 pips shy of the prior breakdown point at 0.8333, the 2023 low. With bearish conditions prevailing, spot has reverted back towards 0.8260. We noted yesterday that Danske have updated their 12-month forecast for USDCHF to 0.7500. It is worth noting that EURCHF has edged back above 0.9400 as the cross edges further away from key medium-term support in the low 0.92s.

- US jobless claims, durable goods and existing home sales data highlight the economic calendar today. ECB’s Nagel will speak at 1300BST, and ECB’s Lane participates in a panel. Fed’s Kashkari is also scheduled.

EGBS: Dovish Interpretation of Rehn Remarks Supports Bunds

Bund futures have rallied through the course of the morning, finding support from Chinese pushback against reports of Sino-US tariff negotiations and a dovish interpretation of comments from ECB’s Rehn.

- Futures are +43 ticks at 131.69 narrowing the gap to initial resistance and the bull trigger at 132.03. Clearance of this level would confirm a resumption of the uptrend and open 132.56, the Feb 28 high.

- Initial support is the 20-day EMA at 130.40.

- While the headlines from Rehn around the scope for a "larger" ECB rate cut screen dovish, it's unclear just how much of a change in tone it actually is.

- Germany's IFO Business Climate Index unexpectedly rose in April, to 86.9 (from 86.7 Mar), stronger than consensus (85.2)

- The German curve has bull steepened, with dovish short-term EUR rate repricing (67bps of cuts priced into OIS through year-end vs 62bps at yesterday’s close) dragging Schatz yields 5bps lower.

- The 10-year BTP/Bund spread has tightened 2bps to 111bps. This morning’s 2.55% Feb-27 BTP Short Term supply was digested smoothly.

- ECB Chief Economist Lane participates in a panel alongside the BOE’s Lombardelli and Riksbank’s Seim at 1400BST, with Simkus and Rehn (again) also scheduled this afternoon.

GILTS: A Little Firmer as Trade Questions Linger, 20s See Decent Demand

Gilt futures have ticked higher but remain comfortably within yesterday’s range, mimicking moves in wider core global FI markets.

- Initial support and resistance defined at the 20-day EMA (92.02) & April 23 high (93.32), respectively.

- Yields 1.5-2.5bp lower, 5s outperform after aggressive twist flattening on Wednesday.

- 10s failed to hold the break below 4.50% yesterday, leaving the long-term uptrend (which intersects at 4.393% today) and the April low (4.363%) unchallenged.

- 10-Year spread to Bunds is essentially unchanged, consolidating most of yesterday’s ~5bp narrowing, last 206bp. A reminder that 200bp was not tested during yesterday’s spread tightening.

- China’s pushback against the idea of Sino-U.S. trade talks being underway has removed some of the optimism that followed comments and source reports out of the U.S. over the last 36 hours.

- 20-Year gilt supply was met by decent demand, probably aided by yesterday’s reduction in the long bucket allocation within the DMOs revised gilt remit.

- BoE-dated OIS prices 88bp of cuts through year-end, ~2.3bp of additional cuts vs. yesterday’s closing levels. A reminder that recent dovish extremes showed ~97bp of cuts over that horizon.

- SONIA futures 0.5-5.5 firmer.

- Looking ahead, BoE MPC member Lombardelli will appear on a panel this afternoon (14:00 BST).

EQUITIES: Wednesday's Gains for Eurostoxx Futures Highlight a Corrective Cycle

Eurostoxx 50 futures have recovered from Tuesday’s low. Recent gains highlight a corrective cycle and the rally marks an unwinding of a recent oversold trend condition. The 20-day EMA has been cleared. The next key resistance to watch is 5102.45, the 50-day EMA. Key support and the bear trigger has been defined at 4444.00, the Apr 7 low. A break of this level would confirm a resumption of the downtrend. The bull cycle in S&P E-Minis that started on Apr 7 is considered corrective. The trend condition has been oversold following recent weakness and gains have allowed this to unwind. Price has traded above the 20-day EMA, at 5423.30. This exposes 5528.75, the Apr 10 high. Note that resistance at the 50-day EMA - a key level too - is at 5630.01. For bears, a resumption of weakness would refocus attention on 4832.00, the Apr 7 low and bear trigger.

- Japan's NIKKEI closed higher by 170.52 pts or +0.49% at 35039.15 and the TOPIX ended 8.24 pts higher or +0.32% at 2592.56.

- Elsewhere, in China the SHANGHAI closed higher by 0.933 pts or +0.03% at 3297.288 and the HANG SENG ended 162.86 pts lower or -0.74% at 21909.76.

- Across Europe, Germany's DAX trades lower by 204.67 pts or -0.93% at 21757.42, FTSE 100 lower by 25.18 pts or -0.3% at 8377.94, CAC 40 down 59 pts or -0.79% at 7423.36 and Euro Stoxx 50 down 47.33 pts or -0.93% at 5051.41.

- Dow Jones mini down 340 pts or -0.85% at 39437, S&P 500 mini down 41.25 pts or -0.76% at 5360.25, NASDAQ mini down 187.25 pts or -1% at 18615.5.

Time: 09:55 BST

COMMODITIES: Recent Move Lower for Gold Allowing Overbought Trend to Unwind

A bearish theme in WTI futures remains intact and the recovery since Apr 9 is - for now - considered corrective. The move higher is allowing an oversold trend condition to unwind. Recent weakness has resulted in the breach of a number of important support levels, reinforcing a bearish threat. A resumption of the bear cycle would open $53.72, a Fibonacci projection. Resistance to watch is 65.96, the 50-day EMA. The trend needle in Gold continues to point north and this week’s fresh cycle high reinforces bullish conditions. The latest move down appears corrective and is allowing an overbought trend condition to unwind. Moving average studies are unchanged, they remain in a bull-mode position highlighting a dominant uptrend. The next objective is $3547.9, a Fibonacci projection. Initial firm support to watch lies at 3194.1, the 20-day EMA.

- WTI Crude up $0.4 or +0.64% at $62.69

- Natural Gas down $0.05 or -1.69% at $2.971

- Gold spot up $50.02 or +1.52% at $3337.83

- Copper up $1.05 or +0.21% at $490.5

- Silver down $0.2 or -0.59% at $33.3715

- Platinum up $0.54 or +0.06% at $975.94

Time: 09:55 BST

| Date | GMT/Local | Impact | Country | Event |

| 24/04/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 24/04/2025 | 1230/0830 | *** | Jobless Claims | |

| 24/04/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 24/04/2025 | 1230/0830 | * | Payroll employment | |

| 24/04/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 24/04/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/04/2025 | 1300/1500 | ECB's Lane at Peterson Institute Webcast on Monetary Policy Strategy | ||

| 24/04/2025 | 1325/1425 | BOE's Lombardelli on Monetary Policy Strategy | ||

| 24/04/2025 | 1400/1000 | *** | NAR existing home sales | |

| 24/04/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 24/04/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 24/04/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 24/04/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 24/04/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 24/04/2025 | 2100/1700 | Minneapolis Fed's Neel Kashkari | ||

| 25/04/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 25/04/2025 | 2330/0830 | ** | Tokyo CPI | |

| 25/04/2025 | 0600/0700 | *** | Retail Sales | |

| 25/04/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 25/04/2025 | 1230/0830 | ** | Retail Trade | |

| 25/04/2025 | 1230/0830 | ** | Retail Trade | |

| 25/04/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 25/04/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 25/04/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 25/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 25/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 25/04/2025 | 1915/2015 | BOE's Greene on Inflation, growth and moentary policy | ||

| 25/04/2025 | 2000/1600 | Kevin Warsh |