GERMAN DATA: IFO Unexpected Uptick on Services / Current Situation

Apr-24 08:25

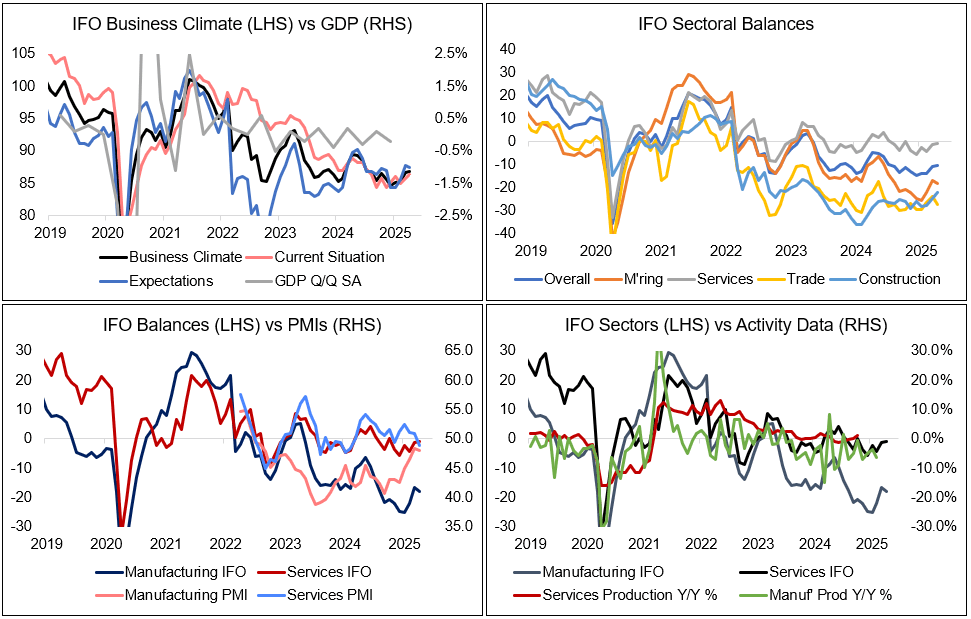

Germany's IFO Business Climate Index unexpectedly rose in April, to 86.9 (from 86.7 Mar), stronger than consensus (85.2) despite firmer US tariff policies which were expected to drive the index downwards. The print also surprises in terms of the services sector, where sentiment improved - contrary to yesterday's Services flash PMI release.

- The current assessment reading was the upside driver this month, at 86.4 (vs 85.4 cons; 85.7 prior); expectations deteriorated to 87.4 but remained above expectations (85.0 cons; 87.7 prior).

- Across sectors, in manufacturing, more pessimistic expectations filtered through to a weaker overall reading - this appears sensical amid the US tariff developments in April. Uncertainty is particularly elevated in the sector, IFO comments.

- In services, the overall reading brightened on the back of a stronger current assessment - expectations "remain slightly cautious", IFO comments. Specifically in hospitality, sentiment rose - this might have been underpinned by a restaurants VAT reduction planned according to the CDU/CSU/SPD coalition agreement.

- Trade sentiment deteriorated, driven by wholesale in particular.

- Construction sentiment rose to the highest since May 2023 as expectations in the sector improved - that would be consistent recent moves towards a more dovish ECB outlook.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: Call spread buyer

Mar-25 08:23

ERM5 98.00/98.12cs, bought for 1.25 in 4k.

DUTCH AUCTION PREVIEW: 2.50% Jul-35 DSL On Tap Today

Mar-25 08:23

This morning, the Netherlands will hold a DSL auction to issue E1.5-2.0bln of the 2.50% Jul-35 DSL (ISIN: NL0015002F72).

- This DSL was launched via syndication on March 4, where it saw books in excess of E29bln for the E6bln issued. Rabobank note that “it is relatively unusual for the first DSL tap to take place post a DDA to consist of the bond that was launched at that DDA”.

- They write that “in this instance the choice of the DSL 2035 may have reflected the very low allocation at the ‘cut-off’ of the DDA”…“this in turn suggests that the tap will be meeting unsatisfied demand and so should be well received”.

- Rabo conclude that “we think that, in the wake of Germany’s spending announcement, there are logical reasons to use this auction to go long versus EUR swap, France or Belgium”.

- Last week, we noted that Germany’s recent fiscal plans will likely further isolate the Netherlands as a fiscal outlier in the Eurozone. See here for more.

- Timing: Results will be available shortly after the bidding window closes at 0900GMT/1000CET.

GILTS: Tracking Wider Weakness At Open, Supply Eyed Today

Mar-25 08:20

Gilts look to weakness in peers (details outlined in our pre-gilt open STIR post) early today.

- Futures break yesterday’s low, trading as soft as 91.08, before a recovery to ~91.25.

- Support at the Mar 13 low (91.07) remains intact, with the bearish technical trend still in place.

- Yields ~2bp higher across the curve.

- 2s10s and 5s30s continue to hold below 50bp and 100bp, respectively.

- 10s little changed vs. Bunds at 194bp after some mechanical widening due to benchmark rolls last week.

- An FT story provided the latest fiscal colour ahead of tomorrow’s Spring Statement, essentially confirming the erosion of the fiscal headroom outlined in the Autumn Budget, while pointing to more than GBP5bln of further spending cuts.

- The piece also suggested that the OBR forecast for UK economic growth in ’25 will be halved to ~1%.

- On the supply front, the DMO will come to market with GBP2bln of the 4.75% Oct-43 line this morning.

- Little else of note on the domestic calendar until tomorrow’s CPI & Spring Statement.