MNI US MARKETS ANALYSIS - Waller Speech in Focus

Highlights:

- Waller speech a session highlight, still among frontrunners for Fed Chair

- USD Index bouncing, but front-end of yield curve remains under pressure

- UK CPI softer-than-forecast, raises pricing of BoE cuts across 2026

US TSYS: Extending Losses With US Filtering In, Waller and 20Y Ahead

Treasuries have reversed their rally on yesterday’s payrolls report, underperforming EGBs in the process, with moves extending as US desks filter in amidst a backdrop of solid gains for WTI futures (2.1%) following Trump ordering a blockade on Venezuela oil. Today’s front-end focus will be on Waller, although impact is likely limited by US CPI coming tomorrow, before the long-end sees a 20Y auction. Long after the close, Trump addresses the nation at 9pm ET – we could hear more on the Venezuela blockade whilst WH Press Sec Leavitt yesterday said it will include his historic accomplishments with a potential tease of 2026 policy.

- Cash yields are 2.1-3.6bp higher, with increases led by 20s/30s where today’s 20Y supply might be weighing at the margin.

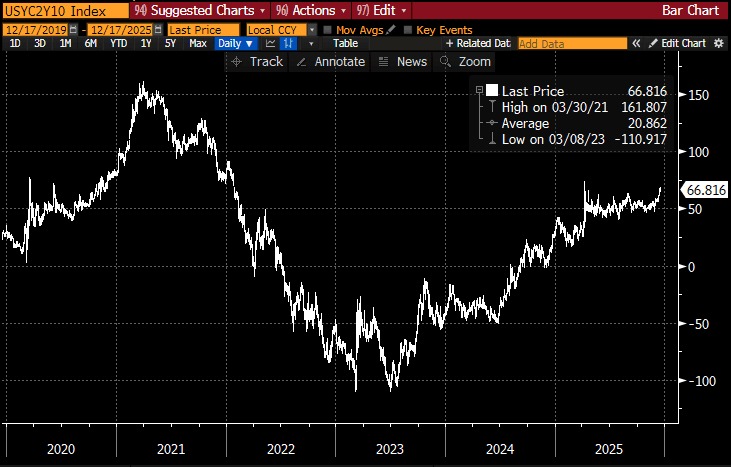

- Curves consolidate yesterday’s modest pullback off fresh recent highs for 2s10s, currently at 66.8bps off yesterday’s 69.1bp. It came within sight of April’s 73.8bp for highs since early 2022.

- TYH6 trades at 112-09+ (-07) close to recent session lows but having remained within yesterday’s range throughout, amidst light cumulative volumes of 250k.

- The technical set-up points to a bearish outlook with support at the bear trigger of 111-29 (Dec 10 low) before 111-19 (Fibo projection). Resistance meanwhile is seen at 112-22+ (Dec 16 snap high on payrolls which also met the 50-day EMA) and 112-23 (Dec 11 high).

- Data: Weekly MBA data (0700ET), Chicago Fed CARTS indicator (0830ET), Manheim used vehicle prices mid-Dec update (0900ET)

- Fedspeak: Waller (0815ET), Williams (0905ET), Bostic (1230ET) – see STIR bullet

- Coupon issuance: US Tsy $13B 20Y Bond re-open - 912810UQ9 (1300ET). Last month’s 20Y saw surprisingly little reaction to it tailing by 0.4bps and a sizeable decline in bid-to-cover from 2.73 to 2.41. Last week’s 30Y at least saw some improved demand, with the bid-to-cover firming from 2.29 to 2.36 whilst it came in nearly in-line with a 0.1bp stop through.

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump address the nation (2100ET)

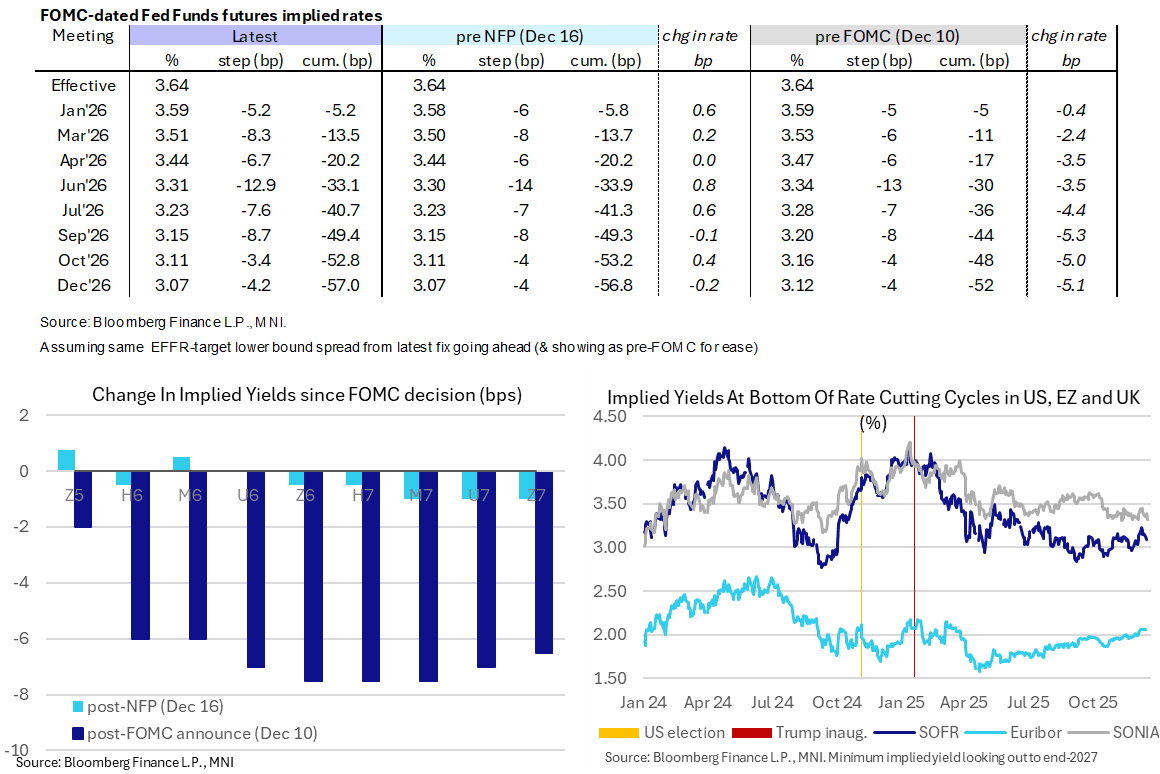

STIR: Fed Rate Path Back To Unchanged Since NFPs, Waller In Spotlight Today

- Fed Funds implied rates are 0.5-1.5bp higher for meetings out to end-2026, having now fully reversed a modest dovish reaction to yesterday’s NFP report with its multiple caveats.

- Cumulative cuts from 3.64% effective: 5bp Jan, 13.5bp Mar, 20bp Apr, 33bp Jun, 49.5bp Sep and 57bp Dec.

- SOFR futures are up to 4 ticks lower out to end-2027, with the implied terminal yield of 3.125% (Z6) 4bps higher but still within recent ranges.

- CPI looms large tomorrow but in the interim today’s docket is likely headlined by Fed Governor Waller’s appearance for his take on the payrolls report. He has seen some renewed interest in betting markets for next Fed chair although at 16% still lags Warsh (24%) and particularly Hassett (56%) – all from Polymarket. Hassett’s odds have seen little adverse impact from Politico yesterday citing three Trump officials raising doubts about Hassett for the role, with some pushback already noted elsewhere.

- 0815ET – Gov. Waller (voter) speaks on the economic outlook (no text). He has for a while now been one of the more dovish FOMC members, calling for cuts to get ahead of labor market weakness. It will be interesting to hear his views ahead of the January meeting, one that he last month described as “tricky” with a flood of incoming data and the need for a meeting-by-meeting approach.

- 0905ET – NY Fed Williams (voter) opening remarks (no text). Whilst having a notable impact after last month’s payrolls report with his unusual guidance in favor of a Dec cut, the opening remarks with no text at a FX market structure conference could limit mon pol discussions.

- 1230ET – Bostic (non-voter, retiring Feb) in moderated discussion (no text). He yesterday said he would have preferred to have held rates unchanged this month and didn’t pencil in any cuts for 2026, indicating he is one of just three participants who saw rates unchanged vs pre-December cut levels (of note from a composition basis with him shortly stepping down).

MNI PREVIEWS

MNI US CPI PREVIEW: Handle With Care

The latest delayed CPI update from the Bureau of Labor Statistics threatens to be messy in several regards, muddying the signal for markets and for monetary policy. The government shutdown precluded October data collection, meaning overall CPI aggregates will not be available for the month, and the inflation recorded for November is on a 2-month change basis from Sept. While the M/M data will never be officially available, MNI's usual aggregation of sell-side analyst expectations points to expectations of an average of 0.24% M/M core CPI monthly across October and November.

MNI ECB PREVIEW: Relative Resilience Confirms in a Good Place

The ECB is again fully expected to leave its three key rates on hold on Thursday, including a 2% deposit rate nicely within the 1.75-2.25% neutral rate range estimated by ECB staff. This time though the meeting comes against a backdrop of a very mild hiking bias to end-2026, helped by recent rhetoric from Schnabel, which despite having been pared fairly notably in recent days is still a change from a modest easing bias ahead of recent meetings.

MNI BOJ PREVIEW: Hike Fully Priced

The BOJ is widely expected to raise the policy rate by 25bp to 0.75% at the December 18–19 meeting, with Governor Ueda’s recent remarks signalling increased confidence in the outlook for growth, inflation and wage momentum. Ueda has indicated the BOJ will assess the “pros and cons of raising the policy interest rate,” while Policy Board members say conditions for a hike are “gradually falling into place,” though confirmation of spring wage momentum remains key.

MNI NORGES BANK PREVIEW: Dovish Revisions, No Commitment

Norges Bank is unanimously expected to hold the policy rate at 4% on Thursday, in a quarterly decision which includes an updated MPR and rate path projection. The rate path will be the primary focus for markets, and we expect a downward revision relative to September. The downward revision we anticipate may shift the balance of risks in favour of 2x25bp cuts next year, versus the single cut embedded in the September rate path.

MNI RIKSBANK PREVIEW: No Policy Pivot Yet

The Riksbank is expected to hold the policy rate at 1.75% on Thursday, in a quarterly decision which includes an updated MPR and rate path projection. We expect the policy statement to re-iterate that the policy rate will be kept at 1.75% for “some time”. The main focus should be on the first three quarters of the updated rate path. This is the part of the curve that is “owned” by the Executive Board, and therefore constitutes a policy signal (beyond that is a staff forecast).

MNI BANXICO PREVIEW: Cut Seen, Hawkish Risks Prevalent

Banxico is expected to deliver another 25bp rate cut to 7.0% on Thursday as it continues to respond to weak activity data, which revealed a contraction of the economy in the third quarter. However, recent stronger-than-expected CPI inflation data have significantly increased the risk of a pause in the easing cycle, if not this week, then more likely early in the new year, keeping focus on the forward guidance.

MNI CNB PREVIEW: Repo Rate to End 2025 at 3.50%

The Czech National Bank will almost certainly deliver a well-telegraphed unanimous decision to keep the two-week reference rate unchanged at 3.50% at the final meeting of this year as concerns about familiar inflationary risks continue to linger. Although headline inflation moderated to +2.1% Y/Y in November, the property market is running hot, wages are still growing at pace, and there is considerable uncertainty about the fiscal outlook under the new government.

US TSY FUTURES: Net Long Setting In UXY & US Dominated On Tuesday

OI data points to a mix of net long setting (TU, FV, UXY & US) and short cover (TY & WN) as Tsy futures ticked higher on Tuesday. Net long setting across UXY & US futures provided the only real net positioning swings of note and accounted for almost all of the net DV01 swing on the day.

| 16-Dec-25 | 15-Dec-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,502,427 | 4,502,056 | +371 | +14,726 |

FV | 6,666,243 | 6,645,718 | +20,525 | +908,200 |

TY | 5,419,053 | 5,425,920 | -6,867 | -461,191 |

UXY | 2,516,405 | 2,504,545 | +11,860 | +1,072,478 |

US | 1,858,809 | 1,834,961 | +23,848 | +3,300,708 |

WN | 2,080,065 | 2,081,956 | -1,891 | -341,451 |

|

| Total | +47,846 | +4,493,469 |

SOFR: Mix of Net Long Setting & Short Cover in Futures on Tuesday

OI data points to net long setting dominating in SOFR futures as most contracts settled higher on Tuesday. Instances of net short cover were limited in scale.

| 16-Dec-25 | 15-Dec-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,307,651 | 1,299,410 | +8,241 | Whites | +59,981 |

SFRZ5 | 1,572,341 | 1,568,810 | +3,531 | Reds | +20,336 |

SFRH6 | 1,385,349 | 1,376,296 | +9,053 | Greens | +4,734 |

SFRM6 | 1,154,210 | 1,115,054 | +39,156 | Blues | +28,980 |

SFRU6 | 1,201,807 | 1,177,910 | +23,897 |

|

|

SFRZ6 | 1,135,640 | 1,140,470 | -4,830 |

|

|

SFRH7 | 872,290 | 869,580 | +2,710 |

|

|

SFRM7 | 765,102 | 766,543 | -1,441 |

|

|

SFRU7 | 829,714 | 822,139 | +7,575 |

|

|

SFRZ7 | 842,026 | 841,487 | +539 |

|

|

SFRH8 | 475,302 | 478,724 | -3,422 |

|

|

SFRM8 | 416,723 | 416,681 | +42 |

|

|

SFRU8 | 383,848 | 384,551 | -703 |

|

|

SFRZ8 | 336,817 | 321,077 | +15,740 |

|

|

SFRH9 | 207,348 | 196,101 | +11,247 |

|

|

SFRM9 | 210,336 | 207,640 | +2,696 |

|

|

EUROPE ISSUANCE UPDATE

Portugal buyback results:

- E365mln of the 2.875% Jul-26 OT (ISIN: PTOTETOE0012) at 100.51

- E566mln of the 4.125% Apr-27 OT (ISIN: PTOTEUOE0019) at 102.665

- E115mln of the 0.70% Oct-27 OT (ISIN: PTOTEMOE0035) at 97.53

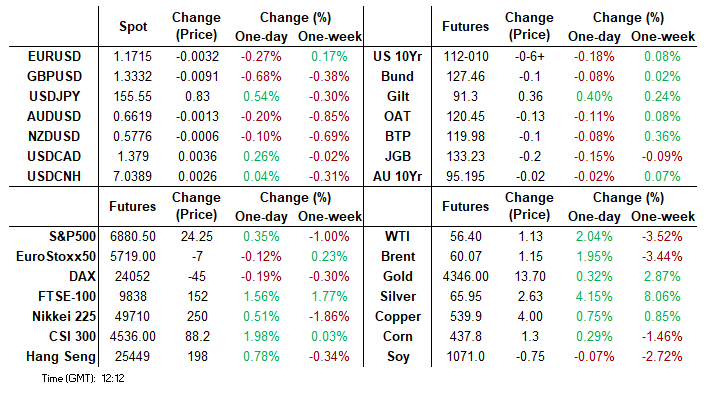

FOREX: Further GBP Downside Could Stem From Vote Split, Comms at Thurs BoE

It’s not pricing for this week’s BoE decision that’s shifting spot markets here, but policy differentials further down the curve. SFIZ6 SONIA futures, capturing year-end 2026 policy expectations, hit a new year-to-date high, providing further contrast with the hawkish shifts in EUR curves since the beginning of the month.

- What next for GBP? With tomorrow’s rate cut baked in, the vote split will be in focus. Today’s inflation print could potentially tilt a vote split to 6-3 – a dovish signal that could usher in easier pricing still for next year as the committee would look more proactive on downside inflation surprises.

- GBPUSD remains pinned toward today’s new weekly lows of 1.3312, while EURGBP is narrowing in on December highs of 0.8802 on this morning’s CPI print.

- For GBPUSD, support sits at 1.3290, the 50-day EMA. A breach of this EMA would highlight a bearish development and signal a possible reversal. To the upside, attention is on 1.3452 (pierced), a Fibonacci retracement. In EURGBP, 0.8802-10 could provide intraday resistance, but a close above this mark today would open gains toward November’s 0.8865.

FOREX: UK CPI Pressures GBP Ahead of BOE Decision, DXY Extends Bounce

- The US dollar trades with a much more constructive tone on Wednesday, prompting a near 0.8% recovery for the DXY from the post-NFP lows. It appears the limited market shift in rates expectations has frustrated the weakening dollar trend into the release, with short-term positions potentially getting squeezed ahead of tomorrow’s US CPI release.

- Lower-than-expected UK CPI has weighed on GBP, pressuring cable down to 1.1312 session lows. It’s not pricing for tomorrow's BoE decision that’s shifting spot markets, but policy differentials further down the curve. With tomorrow’s BOE rate cut well priced, the vote split will be in focus. Today’s inflation print could potentially tilt that to 6-3 – a dovish signal that could usher in easier pricing still for next year as the committee would look more proactive on downside inflation surprises.

- For GBPUSD, support sits at 1.3290, the 50-day EMA. A breach of this EMA would highlight a bearish development and signal a possible reversal. To the upside, attention is on 1.3452 (pierced), a Fibonacci retracement. In EURGBP, 0.8802-10 could provide intraday resistance, but a close above this mark today would open gains toward November’s 0.8865 high.

- USDJPY stands a notable 110 pips above yesterday’s lows at 155.50. Spot traded to within 5 pips of the Dec 05 lows of 154.35 yesterday, bolstering the significance of this area of support ahead of the US data and the BOJ on Friday. Furthermore, the 50-day EMA has also held, intersecting just above the 154.00 handle. A clear breach of this average is required to undermine the bull theme and signal scope for a deeper corrective pullback.

- Weekly MBA mortgage applications and September housing starts highlight the US data calendar before focus turns to tomorrow's central banks, with the Riksbank, Norges Bank, BOE and ECB decisions all due.

OPTIONS: Expiries for Dec17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700(E1.3bln), $1.1750(E1.5bln), $1.1800(E1.6bln), $1.1850(E624mln)

- USD/JPY: Y154.75($594mln)

- AUD/USD: $0.6590(A$680mln), $0.6650-60(A$875mln)

EQUITIES: Latest Pullback for E-Mini S&P Corrective, 50-Day EMA Support Holds

- A bull cycle in Eurostoxx 50 futures remains intact. Price is trading above the 20- and 50-day EMAs, and has recently cleared 5742.40, 76.4% of the Nov 13 - 21 bear leg. The breach of this latter price point paves the way for an extension towards 5825.00, the Nov 13 high and the bull trigger. First key support to watch lies at 5649.07, the 50-day EMA. A clear break of the EMA would highlight a potential short-term reversal.

- A bull cycle in S&P E-Minis remains intact and the latest pullback - for now - is considered corrective. Initial support to watch is 6831.93, the 50-day EMA. It has been pierced, a clear break of this average would signal scope for a deeper retracement. Note that the key support and reversal trigger lies at 6583.00, the Nov 21 low. For bulls, a resumption of gains would refocus attention on the key resistance and bull trigger at 7014.00, the Oct 30 high.

COMMODITIES: WTI Futures Bounce Well Off Tuesday's Lows

- A bearish theme in WTI futures remains intact. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. A key support and the bear trigger at $55.99, the Oct 20 low has been breached. Clearance of this level resumes the downtrend and opens $53.53. Key short-term resistance to watch is $61.84, the Oct 24 high. First resistance is at $59.27, the 50- day EMA.

- A bullish theme in Gold remains intact. The bear phase between Oct 20 - 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch is the 50-day EMA, at $4087.6. Clearance of this EMA would signal scope for a deeper retracement. Attention is on key resistance and the bull trigger at $4381.5, the Oct 20 high.

| Date | GMT/Local | Impact | Country | Event |

| 17/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 17/12/2025 | 1315/0815 | Fed Governor Christopher Waller | ||

| 17/12/2025 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/12/2025 | 1405/0905 | New York Fed's John Williams | ||

| 17/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 17/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 17/12/2025 | 1730/1230 | Atlanta Fed's Raphael Bostic | ||

| 17/12/2025 | 1800/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 18/12/2025 | 2145/1045 | *** | GDP | |

| 18/12/2025 | 0745/0845 | ** | Manufacturing Sentiment | |

| 18/12/2025 | 0830/0930 | *** | Riksbank Interest Rate Decison | |

| 18/12/2025 | 0900/1000 | *** | Norges Bank Rate Decision | |

| 18/12/2025 | 1000/1100 | ** | EZ Construction Output | |

| 18/12/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Deposit Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Main Refi Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Marginal Lending Rate | |

| 18/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 18/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 18/12/2025 | 1330/0830 | * | Payroll employment | |

| 18/12/2025 | 1330/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1345/1445 | ECB Press Conference | ||

| 18/12/2025 | 1445/1545 | ECB Staff Macroeconomic Projections | ||

| 18/12/2025 | 1515/1615 | ECB Lagarde Presents Rate Decision on ECB Podcast | ||

| 18/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 18/12/2025 | 1600/1100 | ** | Kansas City Fed Manufacturing Index | |

| 18/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 18/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 18/12/2025 | 1800/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 18/12/2025 | 1900/1400 | *** | Mexico Interest Rate | |

| 18/12/2025 | 2100/1600 | ** | TICS | |

| 19/12/2025 | 2330/0830 | *** | CPI |