STIR: Fed Rate Path Back To Unchanged Since NFPs, Waller In Spotlight Today

Dec-17 11:38

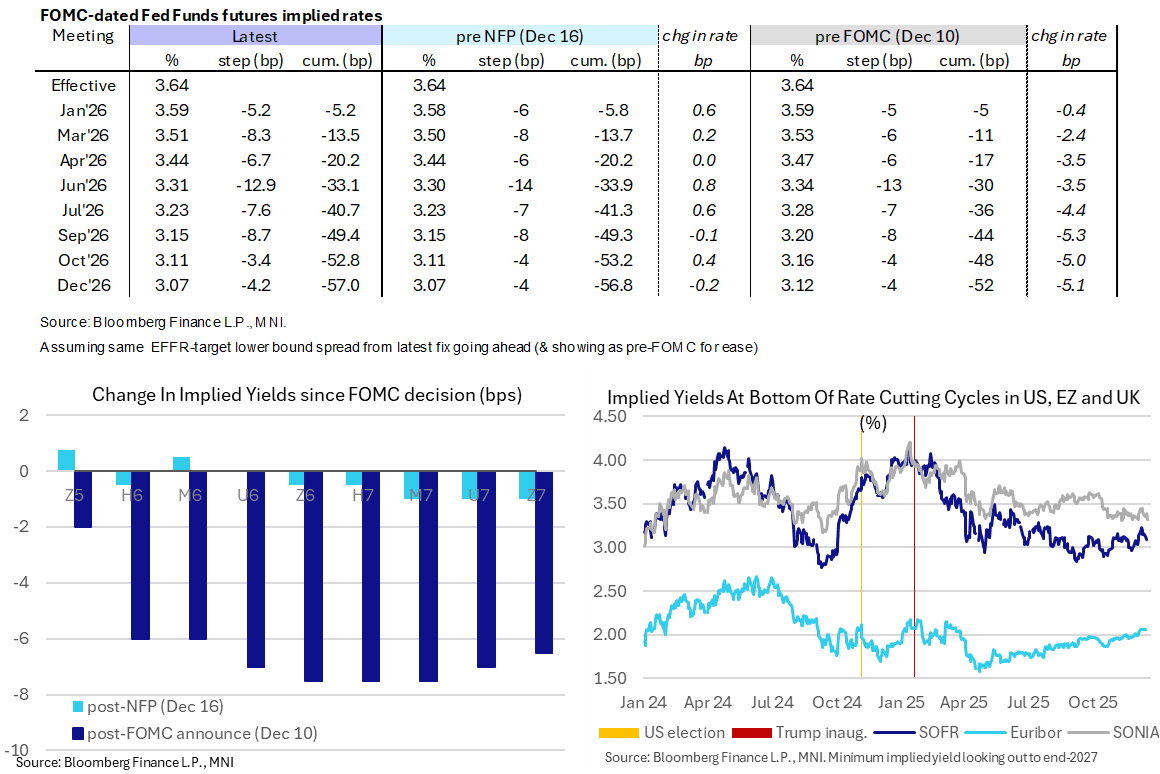

- Fed Funds implied rates are 0.5-1.5bp higher for meetings out to end-2026, having now fully reversed a modest dovish reaction to yesterday’s NFP report with its multiple caveats.

- Cumulative cuts from 3.64% effective: 5bp Jan, 13.5bp Mar, 20bp Apr, 33bp Jun, 49.5bp Sep and 57bp Dec.

- SOFR futures are up to 4 ticks lower out to end-2027, with the implied terminal yield of 3.125% (Z6) 4bps higher but still within recent ranges.

- CPI looms large tomorrow but in the interim today’s docket is likely headlined by Fed Governor Waller’s appearance for his take on the payrolls report. He has seen some renewed interest in betting markets for next Fed chair although at 16% still lags Warsh (24%) and particularly Hassett (56%) – all from Polymarket. Hassett’s odds have seen little adverse impact from Politico yesterday citing three Trump officials raising doubts about Hassett for the role, with some pushback already noted elsewhere.

- 0815ET – Gov. Waller (voter) speaks on the economic outlook (no text). He has for a while now been one of the more dovish FOMC members, calling for cuts to get ahead of labor market weakness. It will be interesting to hear his views ahead of the January meeting, one that he last month described as “tricky” with a flood of incoming data and the need for a meeting-by-meeting approach.

- 0905ET – NY Fed Williams (voter) opening remarks (no text). Whilst having a notable impact after last month’s payrolls report with his unusual guidance in favor of a Dec cut, the opening remarks with no text at a FX market structure conference could limit mon pol discussions.

- 1230ET – Bostic (non-voter, retiring Feb) in moderated discussion (no text). He yesterday said he would have preferred to have held rates unchanged this month and didn’t pencil in any cuts for 2026, indicating he is one of just three participants who saw rates unchanged vs pre-December cut levels (of note from a composition basis with him shortly stepping down).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for Nov17 NY cut 1000ET (Source DTCC)

Nov-17 11:37

- EUR/USD: $1.2100(E1.4bln)

- GBP/USD: $1.3100(Gbp541mln)

- EUR/GBP: Gbp0.8830(E513mln)

- USD/JPY: Y155.00($1.1bln)

- USD/CAD: C$1.4000($510mln)

LOOK AHEAD: Monday Data Calendar: Empire Mfg, Const Spend, Fed Speak, Tsy Bills

Nov-17 11:34

- US Data/Speaker Calendar (prior, estimate)

- 11/17 0830 Empire Manufacturing (10.7, 5.8)

- 11/17 0900 NY Fed Williams welcome remarks (no Q&A)

- 11/17 0930 Fed VC Jefferson moderated discussion outlook/policy (text, Q&A)

- 11/17 1000 Construction Spending (-0.1%, -0.1%)

- 11/17 1130 US Tsy $86B 13W & $77B 26W bill auctions

- 11/17 1300 MN Fed Kashkari moderates discussion

- 11/17 1535 Fed Gov Waller economic outlook, SPE annual dinner

- Source: Bloomberg Finance L.P. / MNI

ECB: Makhlouf Realigns With Median Governing Council Member

Nov-17 11:34

Headlines crossing from Irish Central Bank Governor Makhlouf via Bloomberg:

- "*MAKHLOUF: EXAGGERATION TO SAY HE’S WORRIED ON PRICE TRAJECTORY"

- "*ECB IS IN A GOOD PLACE AT THE MOMENT, MAKHLOUF SAYS"

- "*ECB'S MAKHLOUF: NO NEED TO GET `TOO OBSESSED' WITH ETS2 DELAY"

Note that on October 15, Makhlouf somewhat surprisingly said that he was "more worried that we’re going to be over than under 2%.” Comments today suggest he is more aligned with the median Governing Council member view than those mid-October remarks implied.