US TSYS: Extending Losses With US Filtering In, Waller and 20Y Ahead

Treasuries have reversed their rally on yesterday’s payrolls report, underperforming EGBs in the process, with moves extending as US desks filter in amidst a backdrop of solid gains for WTI futures (2.1%) following Trump ordering a blockade on Venezuela oil. Today’s front-end focus will be on Waller, although impact is likely limited by US CPI coming tomorrow, before the long-end sees a 20Y auction. Long after the close, Trump addresses the nation at 9pm ET – we could hear more on the Venezuela blockade whilst WH Press Sec Leavitt yesterday said it will include his historic accomplishments with a potential tease of 2026 policy.

- Cash yields are 2.1-3.6bp higher, with increases led by 20s/30s where today’s 20Y supply might be weighing at the margin.

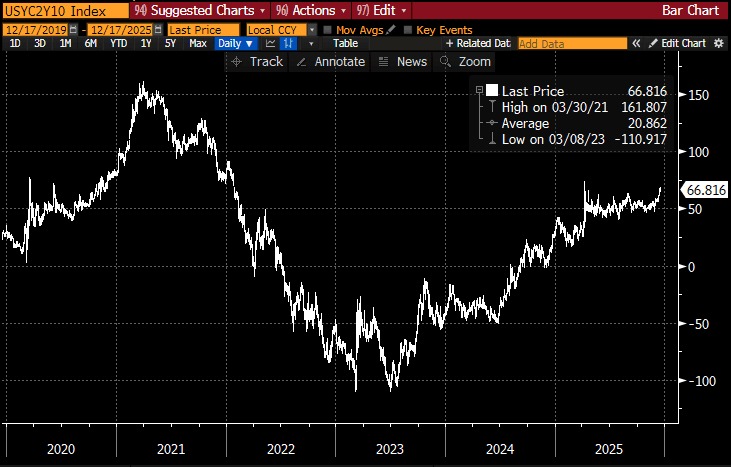

- Curves consolidate yesterday’s modest pullback off fresh recent highs for 2s10s, currently at 66.8bps off yesterday’s 69.1bp. It came within sight of April’s 73.8bp for highs since early 2022.

- TYH6 trades at 112-09+ (-07) close to recent session lows but having remained within yesterday’s range throughout, amidst light cumulative volumes of 250k.

- The technical set-up points to a bearish outlook with support at the bear trigger of 111-29 (Dec 10 low) before 111-19 (Fibo projection). Resistance meanwhile is seen at 112-22+ (Dec 16 snap high on payrolls which also met the 50-day EMA) and 112-23 (Dec 11 high).

- Data: Weekly MBA data (0700ET), Chicago Fed CARTS indicator (0830ET), Manheim used vehicle prices mid-Dec update (0900ET)

- Fedspeak: Waller (0815ET), Williams (0905ET), Bostic (1230ET) – see STIR bullet

- Coupon issuance: US Tsy $13B 20Y Bond re-open - 912810UQ9 (1300ET). Last month’s 20Y saw surprisingly little reaction to it tailing by 0.4bps and a sizeable decline in bid-to-cover from 2.73 to 2.41. Last week’s 30Y at least saw some improved demand, with the bid-to-cover firming from 2.29 to 2.36 whilst it came in nearly in-line with a 0.1bp stop through.

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump address the nation (2100ET)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY OPTIONS: Huge Commerzbank Option trade

CBK (18/12/26) 17p vs (18/06/27) 24p, trades 2.6 in 65k for the 2027.

US TSYS: Extending Highs

- Treasury futures extended the top end of the overnight range in the last 5 minutes, Dec'25 10Y tapped 112-24 before trading back to 112-23 (+6), 10y yield slips to 4.1173% low (-.0310).

- Treasuries last week challenged resistance at the 113-02 level, an area of congestion since Nov 5. This hurdle remains intact, however, a clear move above it would be a bullish signal and shift focus on resistance at 113-18+, the Oct 28 high. A break would also cancel a short-term bearish theme.

- The German 10Y Bund gained as well - but remains off overnight highs, Bbg US$ index firmer at 1217.70 (+1.42), stocks mildly higher (SPX eminis +19.75 at 6,775.00).

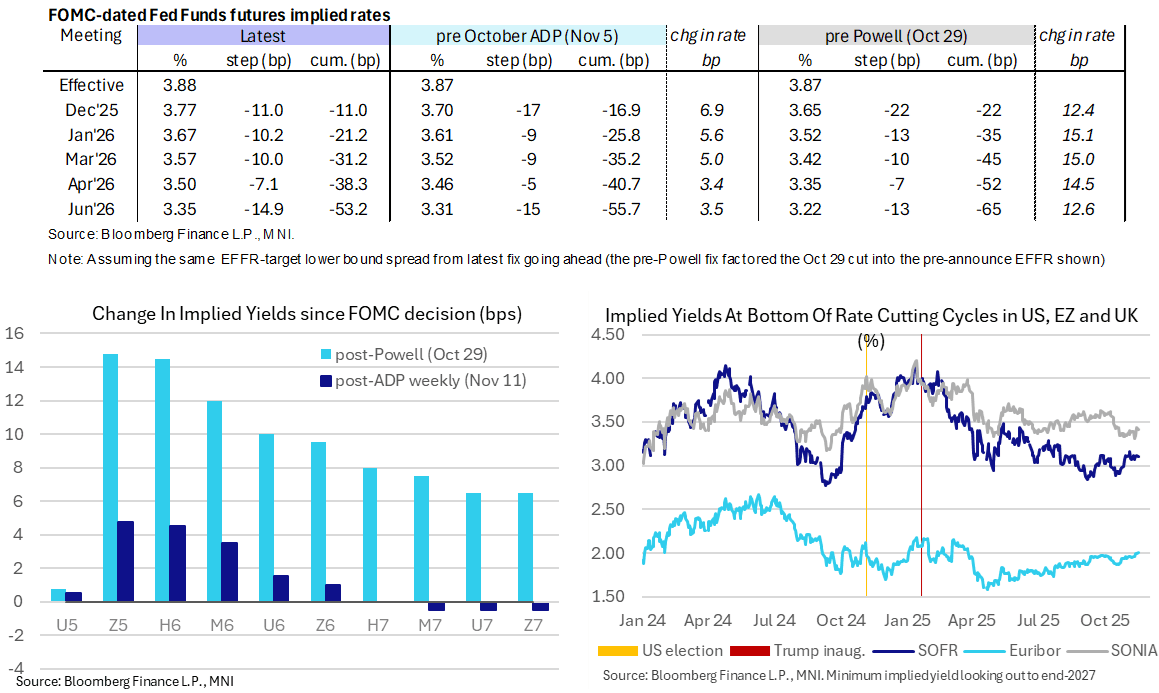

STIR: Fed December Pause Seen As ~50/50 Call As Official Data Resumes

- Fed Funds implied rates are unchanged from Friday’s close, holding last week’s push to a close call for December’s FOMC meeting between another 25bp cut or pausing.

- A pause is now seen as slightly more likely, supported by multiple Fed speakers with patient rhetoric.

- Cumulative cuts from an assumed 3.88% effective: 11bp Dec, 21bp Jan, 31bp Mar, 38.5bp Apr and 53bp Jun.

- SOFR futures are +0.005-0.025, with increases led by 2027 contracts.

- It sees the terminal implied yield remain within recent ranges, at 3.10% (SFRH7) between 3.06-3.16% that has been defined primarily by labor data and a strong ISM services report.

- Today’s data is light – Empire manufacturing for Nov and a delayed construction spending report for Aug – with some Fedspeak updates possibly more important (noted a little earlier). Nonfarm payrolls for September looms large on Thursday even if it is now two months old.