MNI US MARKETS ANALYSIS - USD Softer for 5th Session

Highlights:

- Government shutdown enters second day with no sign of conclusion

- USD softer for fifth session, supporting bonds

- No weekly jobless claims data expected, leaving focus on Fed appearances

US TSYS: Bonds Firmer, Curves Flatter, Challenger Job Cuts Released Early

- Day two of US Government closure. Senate rejected a House Republican funding bill for the third time yesterday, ensuring the US government will remain shut until at least Friday. OMB Director Russell Vought stated late Wednesday that RIFs (reduction in Force) will begin "in a day or two" after Congressional Budget Office estimated 750,000 federal employees to be furloughed.

- Most of today's data will be delayed/suspended due to the shutdown. MNI shutdown guide to US data releases: LINK

- The Challenger Job Cuts was out prior to it's scheduled 0700ET release: "U.S.-based employers announced 54,064 job cuts in September, a 37% drop from the 85,979 cuts announced in August", LINK

- Treasuries are trading steady (TUZ5) to modestly higher: Dec'25 10Y contract (TYZ5) currently trades at 112-29 (+2) on average cumulative volumes of 260k, 10Y yield at 4.0923% (-.0058). Curves flatter: 2s10s -1.198 at 54.743, 5s30s -.900 at 102.720.

- Treasuries bounced Wednesday and the contract is holding on to its latest gains. Attention is on support at the 50-day EMA, currently at 112-11. A clear break of this average would undermine a bull theme and signal scope for a deeper retracement. This would open 111-13+, the Aug 18 low and the next key support. On the upside, initial firm resistance to watch is unchanged, at 113-00, the Sep 24 high. A break would be bullish.

- Treasury Auctions: $105B 4W & $90B 8W bill auctions at 1130ET.

- Fedspeak: Dallas Fed President Logan (alternate voter) moderated discussion at energy & policy conference (1030ET), Chicago Fed President Goolsbee on Fox Business (1430ET).

- Politics: Nothing publicly scheduled for President Trump today, receives his Intelligence briefing at 1100ET (closed press). Expect to see social media posts from President Trump, however. Trump expected to visit Japan on Oct 27.

SOFR: Net Long Setting Dominated In Futures On Wednesday

OI data points to a mix of net long setting and short cover as SOFR futures ticked higher on Wednesday, with the former comfortably more prominent through the blues.

| 01-Oct-25 | 30-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,416,043 | 1,424,624 | -8,581 | Whites | +41,037 |

SFRZ5 | 1,493,411 | 1,477,018 | +16,393 | Reds | +20,400 |

SFRH6 | 1,196,380 | 1,177,102 | +19,278 | Greens | +5,861 |

SFRM6 | 1,036,112 | 1,022,165 | +13,947 | Blues | +5,071 |

SFRU6 | 940,514 | 940,778 | -264 |

|

|

SFRZ6 | 1,034,198 | 1,023,176 | +11,022 |

|

|

SFRH7 | 777,463 | 777,210 | +253 |

|

|

SFRM7 | 791,164 | 781,775 | +9,389 |

|

|

SFRU7 | 681,964 | 679,305 | +2,659 |

|

|

SFRZ7 | 731,477 | 734,582 | -3,105 |

|

|

SFRH8 | 416,493 | 414,198 | +2,295 |

|

|

SFRM8 | 358,964 | 354,952 | +4,012 |

|

|

SFRU8 | 287,775 | 284,319 | +3,456 |

|

|

SFRZ8 | 303,301 | 299,666 | +3,635 |

|

|

SFRH9 | 187,152 | 189,417 | -2,265 |

|

|

SFRM9 | 172,374 | 172,129 | +245 |

|

|

US TSY FUTURES: Long Setting Seen Across The Curve On Wednesday

OI data points to net long setting across all contracts as Tsy futures rallied on Wednesday.

- The most meaningful positioning swings came in FV & US futures.

- Over $10mln DV01 equivalent of fresh net positioning was added across the curve.

| 01-Oct-25 | 30-Sep-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,590,368 | 4,568,493 | +21,875 | +740,858 |

FV | 6,721,710 | 6,641,414 | +80,296 | +3,521,329 |

TY | 5,467,159 | 5,457,806 | +9,353 | +609,264 |

UXY | 2,459,391 | 2,449,310 | +10,081 | +880,823 |

US | 1,858,674 | 1,837,813 | +20,861 | +2,947,947 |

WN | 2,058,492 | 2,050,149 | +8,343 | +1,548,087 |

|

| Total | +150,809 | +10,248,309 |

FOREX: USD Index Lower Again, But Lack of Data Could Contain Vol

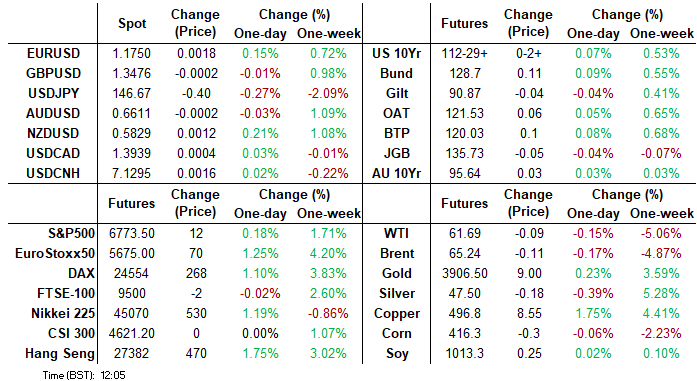

- Into the second day of a US government shutdown, and the USD is weaker again, pressuring the USD Index to trade lower for a fifth consecutive session. Yesterday's 97.462 low is in tact for now, largely as USD/JPY is yet to make another convincing move lower, after yesterday's downside bias has failed to spill over into Thursday trade. That said, support into 146.59 is well within reach, but the lack of US data may contain intraday vol in the interim, and prevent any furher breakout here.

- Global equities trade well, helping underpin a climb for EURUSD to 1.1757. $6.86bn of option notional expire today between 1.1695/1.1800 - these sizeable strikes could further contain spot into the NY cut. The trend condition in the pair is bullish, and a clear resumption of gains would open 1.1923, a Fibonacci projection. Support to watch lies at 1.1686. the 50-day EMA.

- NZD outperforms in a partial reversal of recent AUDNZD price action. Profit taking may be at play as the AU-NZ 2yr swap spread holds firm, just off recent highs. This has been the strong driver of the cross, evident in the EMAs pointing north, with key resistance and the 2022 high standing at 1.1491. The 20-day EMA meanwhile sits at 1.1259.

- With a lack of US data, central bank speakers are in focus. Today sees ECB's Makhlouf, Kazaks, Villeroy & de Guindos as well as Fed's Logan & Goolsbee.

FOREX: Options Show Markets Won't be Caught Offside on Budget Risk Again

Ahead of last year's Autumn Budget, markets underestimated the market-moving potential of Reeves' first fiscal event. While vols indicated a ~30 pip swing in EUR/GBP, price went on to rally near 150 pips in the next two sessions and even with two months until the event, shifts in option vol suggest markets won't be caught offside again.

- The front-end of the GBP vol curve provide a further signal for market concern over the Autumn Budget. The flatter front-end of the curve and the building premium for 2m implied vols shows markets building a risk premium into the event. 2m vols have posted the sharpest gains over the past week as they begin to capture the event on November 26th.

- This effect is particularly evident in EUR/GBP, for which markets continue to favour as a GBP weakness play given the unpredictability of the USD into year-end. This is despite sell-side pushing out expectations of BoE rate cuts this year (see Deutsche Bank, HSBC earlier this month) - an extension of which could work against the consensus view of EURGBP higher.

- We see sustainability of this week's GBP bounce as resting on the fiscal policy mix ahead. The Gilt curve and, in particular, the longer-end has regained a sense of stability after being marked sharply higher at the beginning of September. How valid and long-lasting this proves to be should determine GBP/USD's ability to hold above 1.3525 (50% mid-Sept downleg) and make meaningful headway toward the bull trigger of the July 1st high at 1.3789.

OPTIONS: Expiries for Oct02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1580(E1.0bln), $1.1615-30(E1.6bln), $1.1675-80(E950mln), $1.1695-00(E1.6bln), $1.1720-25(E964mln), $1.1750(E1.2bln), $1.1785-90(E2.9bln), $1.1850(E760mln), $1.1900(E950mln)

- USD/JPY: Y147.95-00($1.6bln), Y149.50($1.0bln)

- AUD/USD: $0.6600(A$1.9bln)

- USD/CAD: C$1.3900($777mln)

EQUITIES: Bull Cycle in E-Mini S&P Intact as Contract Trades to Fresh Cycle High

- Eurostoxx 50 futures maintain a bullish theme. This week’s gains have resulted in a breach of key resistance at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend. The impulsive climb opens 5646.00 next, a Fibonacci projection, with potential for a test of the 5700.00 handle further out. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. Initial firm support is 5525.00, the Aug 22 high.

- A bull cycle in S&P E-Minis remains intact. The contract has again traded to a fresh cycle high to confirm a resumption of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6787.63, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6666.25. It has recently been pierced, a clear break of it would signal scope for a deeper pullback, potentially towards the 50-day EMA, at 6550.28.

COMMODITIES: Recent Pullback for WTI Futures Reinforces Bearish Theme

- WTI futures have pulled back from their recent highs. This reinforces a bearish theme and suggests S/T gains are corrective. Initial firm resistance has been defined at $66.42, the Sep 29 high. The key resistance is at $68.43, the Jul 30 high, where a break is required to signal scope for a stronger recovery. The clear reversal lower refocuses attention on key support at $60.85, the Aug 13 low. A break of this level would reinstate the downtrend.

- A bull cycle in Gold remains in play. The yellow metal has traded to a fresh cycle high this week, confirming a resumption of the primary uptrend. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on $3909.4, a Fibonacci projection. On the downside, support to watch lies at $3700.1, the 20-day EMA. A pullback would be considered corrective.

| Date | GMT/Local | Impact | Country | Event |

| 02/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 02/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 02/10/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/10/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 02/10/2025 | 1430/1030 | Dallas Fed's Lorie Logan | ||

| 02/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 02/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 02/10/2025 | 1700/1900 | ECB de Guindos Fireside Chat at ESADE Madrid | ||

| 02/10/2025 | 1725/1325 | BOC Deputy Mendes speaks at Western University | ||

| 03/10/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 03/10/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 03/10/2025 | 2330/0830 | * | Labor Force Survey | |

| 03/10/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 03/10/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 03/10/2025 | 0645/0845 | * | Industrial Production | |

| 03/10/2025 | 0700/0300 | * | Turkey CPI | |

| 03/10/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0800/1000 | * | Retail Sales | |

| 03/10/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/10/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/10/2025 | 0900/1100 | ** | EZ PPI | |

| 03/10/2025 | 0940/1140 | ECB Lagarde Speech At Knot Farewell Symposium | ||

| 03/10/2025 | 1000/0600 | NY Fed's John Williams | ||

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1320/1420 | BOE Bailey Keynote At Knot Farewell Symposium | ||

| 03/10/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 03/10/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 03/10/2025 | 1350/1550 | ECB Schnabel In Panel At Knot Farewell Symposium | ||

| 03/10/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 03/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 03/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 03/10/2025 | 1740/1340 | Fed Vice Chair Philip Jefferson | ||

| 03/10/2025 | 2200/1800 | NY Fed's John Williams |