OPTIONS: Expiries for Oct02 NY cut 1000ET (Source DTCC)

Oct-02 08:08

- EUR/USD: $1.1580(E1.0bln), $1.1615-30(E1.6bln), $1.1675-80(E950mln), $1.1695-00(E1.6bln), $1.1720-25(E964mln), $1.1750(E1.2bln), $1.1785-90(E2.9bln), $1.1850(E760mln), $1.1900(E950mln)

- USD/JPY: Y147.95-00($1.6bln), Y149.50($1.0bln)

- AUD/USD: $0.6600(A$1.9bln)

- USD/CAD: C$1.3900($777mln)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB SYNDICATION: 7/30-year BTP: Spreads set

Sep-02 08:08

7yr Tranche (New Nov-32 BTP)

- Spread Set at 3.25% Jul-32 BTP + 8.0bp (guidance was +10bps area)

- Orderbooks in excess of E85bln (incl. E7.5bln JLM interest)

- Size: Benchmark (MNI expects E5-10bln with risks skewed to E7-8bln)

- Maturity: 15 November 2032

- Coupon: Short first

30yr Tranche (New Oct-55 BTP)

- Spread Set at 4.30% Oct-54 BTP + 6.0bp (guidance was +9bps area)

- Orderbooks in excess of E75bln (incl. E4.25bln JLM interest)

- Size previously set at E5bln (WNG)

- Maturity: 1 October 2055

- Coupon: Short first

For both:

- Global books to close at 09:45am UKT / 10:45 CET

- Bookrunners: BBVA / Citi/ Deutsche Bank (B&D/DM) / J.P. Morgan SE / Morgan Stanley / Nomura

- Timing: Books to close at 9:45BST / 10:45CET

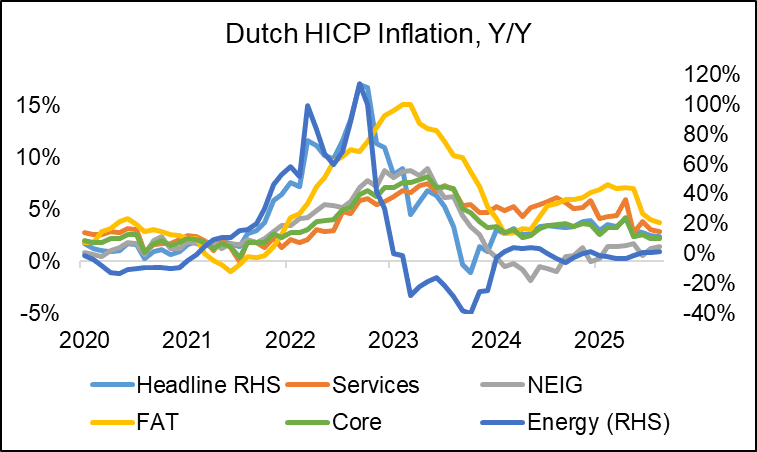

EUROPEAN INFLATION: Netherlands HICP Misses With Softest Core Since Oct-21

Sep-02 08:04

Dutch flash HICP inflation fell below expectations in preliminary August data, to 2.42% (cons 2.5%) after 2.50% in July, for the lowest rate since December 2023. The miss was mirrored by the 0.29% M/M vs cons of 0.4. National CPI inflation meanwhile was as expected at 2.8% Y/Y, also easing a tenth.

- Core HICP was behind the deceleration with its second consecutive downtick, at 2.16% Y/Y (2.23% July), the lowest rate since October 2021.

- Services fell more substantially in August, to 2.87% Y/Y (3.11% July). The category saw some volatility in Q2 but appears to consolidate clearly below 2024 levels (see chart).

- Non-energy industrial goods (core goods) meanwhile rose its second consecutive time, to 1.42% Y/Y (1.25% July).

- Looking at the non-core items, FAT (food/alcohol/tobacco) came in at 3.71% (4.07% July). Contrary to the wider Eurozone, the category has seen a clear downtrend this year (it was above 7% until May). Energy inflation accelerated meanwhile to 1.57% (0.90% July). This is a similar dynamic to what will be expected for the EZ-wide print out later today, with base effects at play looking at the -0.39% M/M sequential print in the category.

- The national CPI was as expected however, at 2.8% in August (2.8% cons, 2.9% July).

- For reference, Netherlands represents around 6% of the overall 2025 Eurozone HICP basket.

GILT SYNDICATION: 4.75% Oct-35 gilt: Update

Sep-02 08:01

- Guidance: 4.50% Mar-35 Gilt +8.25/+8.75bps (unchanged from books opening)

- Size: GBP Benchmark (MNI expects GBP8-12bln)

- Cooks in excess of GBP110bln (inc JLM interest of GBP10.2bln)

- Maturity: 22 October 2035

- Expected Settlement: 3 September 2025 (T+1)

- Coupon: 4.750% SA, ACT/ACT, long 1st to 22 April 2026

- Benchmark: 4.50% Mar-35 Gilt (ISIN: GB00BT7J0027)

- ISIN: GB00BTXS1K06

- Bookrunners: HSBC / J.P. Morgan (DM/B&D) / Lloyds / Morgan Stanley / NatWest / UBS

Details per market source and MNI colour