MNI US MARKETS ANALYSIS - Shutdown Day 3, No NFP Due

Highlights:

- Shutdown enters day 3, no NFP expected but many calling for it

- ISM services index could take on greater importance in dearth of releases

- French PM having hard time garnering budget support

US TSYS: All Ready with No Employment Data to Show

- Very unlikely the BLS September employment report is released this morning despite Sen Warren (Dem) telling CNN Thursday afternoon that the "labor data has been collected and is likely ready to be released". "Let’s be clear," Warren added, "the jobs data scheduled to come out this Friday has undoubtedly been collected and the President must release it."

- Still expected S&P Global US Services/Composite PMIs (0945ET) and ISM Services (1000ET), Bbg survey sees a small increase to 51.5 from 50.8 in a second monthly improvement after the 49.9 in May was its lowest since Jun 2024, with prices paid looking to remain elevated. MNI shutdown guide to US data releases: LINK

- Treasuries are trading mildly mixed on very light volumes: Dec'25 10Y contract (TYZ5) currently trades at 112-28.5 (-1) on cumulative volumes of 133k, 10Y yield at 4.0864% (+.0037). Curves flatter: 2s10s -.249 at 53.933, 5s30s -.544 at 101.107.

- Treasuries bounced Wednesday and the contract is holding on to its latest gains. Support at the 50-day EMA, currently at 112-12, has been pierced but remains intact. A clear break of this average would undermine a bull theme and signal scope for a deeper retracement. This would open 111-13+, the Aug 18 low and the next key support. On the upside, initial firm resistance to watch is unchanged, at 113-00, the Sep 24 high. A break would be bullish.

- Fedspeak: Expanding speaker list kicked off with NY Fed Pres Williams speaking in Amsterdam earlier ("BALANCE SHEET USE IS NOT UNCONVENTIONAL .. MONETARY POLICY TOOLS NOT LIMITED TO SHORT-TERM RATES" Bbg). Chicago Fed Goolsbee on CNBC (0830ET), Fed Gov Miran on Bbg TV (0935ET), Dallas Fed Logan moderated discussion Int Economics conf (1330ET), Fed VC Jefferson economic outlook (1340ET), Fed Gov Miran on Fox Business (1530ET).

- Politics: Limited schedule for President Trump today, participates in a Swearing-In Ceremony for the U.S. Ambassador to the Kingdom of Sweden at 1130ET (closed press). WH Press Sec Leavitt briefing at 1300ET. Expect to see social media posts from President Trump, however.

US TSY FUTURES: Light Bias Towards Cover On Thursday

OI data points to a mix of net long cover (TU), short cover (FV) and long setting (TY, UXY, US & WN), with the net curve-wide bias tilted towards cover as the curve twist flattened on Thursday.

- DV01 equivalent positioning adjustments were limited, with the only movement topping $1mln DV01 coning in FV futures.

| 02-Oct-25 | 01-Oct-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,582,098 | 4,590,342 | -8,244 | -325,386 |

FV | 6,685,276 | 6,720,618 | -35,342 | -1,550,150 |

TY | 5,478,885 | 5,466,706 | +12,179 | +825,764 |

UXY | 2,463,665 | 2,458,906 | +4,759 | +431,686 |

US | 1,859,021 | 1,858,677 | +344 | +49,053 |

WN | 2,058,795 | 2,058,341 | +454 | +85,186 |

|

| Total | -25,850 | -483,847 |

SOFR: Net Long Setting In SFRU6 Most Prominent In Futures On Thursday

OI data suggests that net long setting in SFRU6 provided the only real positioning swing of note in futures on Thursday, presumably aided by a 10K block buyer of the SFRZ5-U6 pack in the NY morning.

| 02-Oct-25 | 01-Oct-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,422,754 | 1,408,149 | +14,605 | Whites | -799 |

SFRZ5 | 1,479,296 | 1,485,310 | -6,014 | Reds | +43,221 |

SFRH6 | 1,170,713 | 1,186,221 | -15,508 | Greens | -2,524 |

SFRM6 | 1,034,072 | 1,027,954 | +6,118 | Blues | +2,297 |

SFRU6 | 979,121 | 939,796 | +39,325 |

|

|

SFRZ6 | 1,039,001 | 1,033,391 | +5,610 |

|

|

SFRH7 | 779,636 | 777,462 | +2,174 |

|

|

SFRM7 | 787,240 | 791,128 | -3,888 |

|

|

SFRU7 | 677,232 | 681,964 | -4,732 |

|

|

SFRZ7 | 729,623 | 731,577 | -1,954 |

|

|

SFRH8 | 423,536 | 416,492 | +7,044 |

|

|

SFRM8 | 356,082 | 358,964 | -2,882 |

|

|

SFRU8 | 285,771 | 287,775 | -2,004 |

|

|

SFRZ8 | 309,216 | 303,300 | +5,916 |

|

|

SFRH9 | 186,376 | 187,151 | -775 |

|

|

SFRM9 | 171,534 | 172,374 | -840 |

|

|

US: BLS Fully Furloughed, But Some Call for NFP Release Anyway

- Today's payrolls print is extremely unlikely to go ahead - the BLS are formally in furlough, with all their 2054 full-time employees not working - this leaves just the acting BLS head in the office as they're presidentially appointed, and don't fall under federal funding.

- That said, there have been calls for the labor market report to be released regardless - Senator Elizabeth Warren has pressed for a full release despite the shutdown, while a Senate Banking Aide has confirmed the data has been collected for September and is likely ready for release.

- How such a release could go ahead is the question: Last week, the BLS confirmed their plans that the data would be delayed in the event of shutdown, given the department has suspended their entire operation. This leaves the channels, release methods and infrastructure closed for now.

- Instead, alternative data is gaining attention - yesterday's Revelio Labs RPLS report drew some focus and indicated an in-line-with-expectations BLS release (we can't vouch for their data specifically) and it remains possible that proxies for initial jobless claims can be compiled using state-by-state data - but these will likely be patchy and come heavily caveated.

- ISM services index data today will go ahead as usual and could be a more market-moving event as a result. Our full guide to data releases during shutdown here: https://media.marketnews.com/Shutdown_Guide_Oct120252_ee7acddcc9.pdf

UK DATA: DMP Wage Expectation Corrected and Slightly More Concerning for MPC

- Yesterday the BOE issued a correction for its DMP data release with the wage growth expectations and CPI expected/realised growth were incorrect.

- The most notable thing for us from this was that the expected wage growth single month figure increased to 3.83%Y/Y - the highest since March 2025.

- This wasn't enough to change the 3-month average when rounded to 1dp (which still comes in at 3.6%).

- This is still lower than last year's September print of 4.1%, but this might be a concern for the more dovish members of the MPC who are hoping for wage settlements to be lower.

- For example Ramsden said this week that the Agents survey is "also then pointing to settlements being lower [than the 3.7% for this year], so closer to 3% further out into next year, which will be getting down to target consistent rates."

- If this uptick in wage expectations is matched in next month's DMP survey (which the BOE will see during its November deliberations but won't be published until 2 hours post-Bank Rate decision) and if this is matched by similar sentiment from the Agents this could be enough to make a cut very unlikely.

- Of course, markets are only pricing around 1bp for November and 5bp cumulatively for December - and this correction was published yesterday - so there won't be a near-term market impact from this. But if this is the start of a pickup to wage growth expectations going into year-end, this could be a concern for getting cuts back on track in 2026.

FRANCE: Lecornu Tax Proposal Insufficient: Socialist Leader

- "FRENCH SOCIALIST LEADER FAURE: LECORNU'S PROPOSAL ON TAXES IS VERY FAR FROM WHAT WE HAD SUGGESTED" - Reuters

- "FAURE: LECORNU'S PROPOSAL IS INSUFFICIENT" - Reuters

10-year OAT/Bund spread widens 1bp in quick succession on those headlines, now at 82bps.

Our political risk team has noted: If the pledge on a financial asset tax is not enough for the PS or other opposition parties, and Lecornu sticks to his commitment not to use Art. 49.3, it will leave the gov't with limited options.

- It could give in to the left's demands on repealing the pensions reform and protecting gov't spending, but this would risk a major blowback from markets.

- It could call the opposition's bluff and continue with its austerity budget plan. Either the opposition abstains and allows a budget through (unlikely) or the budget is defeated, bringing down Lecornu and raising the prospect again of an early legislative (and potentially even presidential) election.

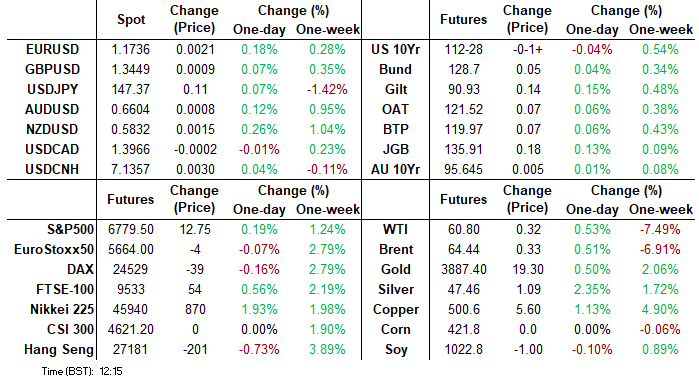

FOREX: USD/JPY Firms Off Support as Ueda Not Swayed on Hike Pressures

- The USD Index trades on the back foot early Friday, fading against all others in G10 outside of the JPY. The BoJ Chair Ueda pressured the currency by stopping short of endorsing an imminent rate hike in Japan, instead reiterating the bank's guidance from their most recent meeting, despite the solid Tankan manufacturing survey data from earlier this week. Instead, Ueda affirmed the Bank would be observing and monitoring incoming datapoints to assess the October decision, for which markets see a roughly 50/50 chance of a 25bps rate hike.

- USDJPY has recovered from Wednesday's low. Recent weakness resulted in a clear breach of the 50-day EMA. This continues to signal scope for a deeper retracement and exposes the key short-term pivot support at 145.49, the Sep 17 low.

- A bull cycle in USDCAD remains intact and yesterday's break above the late September's high, firms the bullish theme. This move higher also maintains the

bullish price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend.

Sights are on 1.4019, a Fibonacci retracement point. - Today's payrolls print is extremely unlikely to go ahead - the BLS are formally in furlough - leaving focus on alternative economic data and it remains possible that proxies for initial jobless claims can be compiled using state-by-state data - but these will likely be patchy and come heavily caveated. ISM services index data today will go ahead as usual and could be a more market-moving event as a result. Our full guide to data releases during shutdown here: https://media.marketnews.com/Shutdown_Guide_Oct120252_ee7acddcc9.pdf

OPTIONS: Expiries for Oct03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700(E1.3bln), $1.1845-55(E2.2bln), $1.1875(E1.2bln)

- USD/JPY: Y146.00($1.3bln), Y147.00($845mln), Y148.00($1.0bln)

- EUR/GBP: Gbp0.8785-05(E1.1bln)

- AUD/USD: $0.6600(A$1.9bln)

- NZD/USD: $0.6450(N$1.2bln)

EQUITIES: Eurostoxx 50 Remain Bullish After Recent Break of Key Resistance

- Eurostoxx 50 futures maintain a bullish theme. This week’s gains have resulted in a breach of key resistance at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend. The impulsive climb opens the 5700.00 handle next, with potential for a test of 5727.18 further out, a Fibonacci projection. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. Initial firm support is 5525.00, the Aug 22 high.

- A bull cycle in S&P E-Minis remains intact. The contract has traded to a fresh cycle high this week to confirm a resumption of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6787.63, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6675.82. It has recently been pierced, a clear break of it would signal scope for a deeper pullback, potentially towards the 50-day EMA, at 6558.72.

COMMODITIES: WTI Futures Breach Bear Trigger and Key Support

- WTI futures have pulled back from their recent highs. Yesterday's sell-off resulted in a move through key support and the bear trigger at $60.85, the Aug 13 low. Clearance of this level strengthens a bearish theme and paves the way for an extension towards $57.50, the May 30 low. Initial firm resistance has been defined at $66.42, the Sep 29 high. A break of this level would highlight a reversal.

- A bull cycle in Gold remains in play. The yellow metal has traded to a fresh cycle high this week, confirming a resumption of the primary uptrend. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on $3909.4, a Fibonacci projection. On the downside, support to watch lies at $3715.0, the 20-day EMA. A pullback would be considered corrective.

| Date | GMT/Local | Impact | Country | Event |

| 03/10/2025 | 1320/1420 | BOE Bailey Keynote At Knot Farewell Symposium | ||

| 03/10/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 03/10/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 03/10/2025 | 1350/1550 | ECB Schnabel In Panel At Knot Farewell Symposium | ||

| 03/10/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 03/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 03/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 03/10/2025 | 1740/1340 | Fed Vice Chair Philip Jefferson |