OPTIONS: Expiries for Oct03 NY cut 1000ET (Source DTCC)

Oct-03 10:35

- EUR/USD: $1.1700(E1.3bln), $1.1845-55(E2.2bln), $1.1875(E1.2bln)

- USD/JPY: Y146.00($1.3bln), Y147.00($845mln), Y148.00($1.0bln)

- EUR/GBP: Gbp0.8785-05(E1.1bln)

- AUD/USD: $0.6600(A$1.9bln)

- NZD/USD: $0.6450(N$1.2bln)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

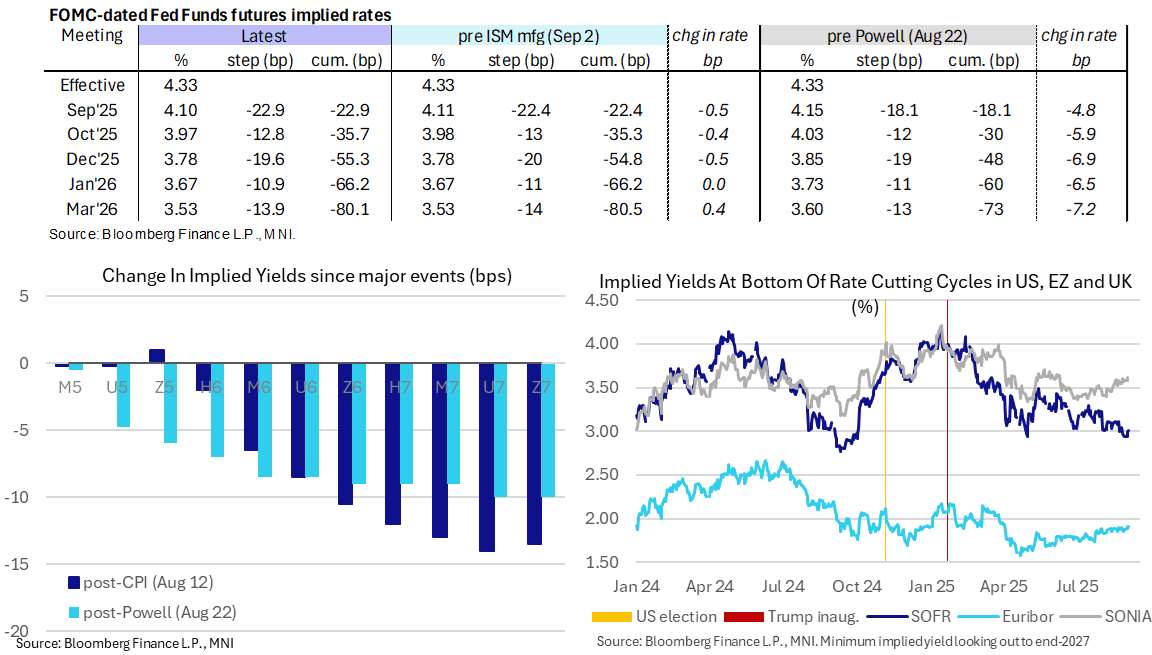

STIR: 55bp Of Fed Cuts To Year-End Ahead Of Musalem, JOLTS and Then Beige Book

Sep-03 10:30

- Fed Funds implied rates are up to 1bp higher on the day for meetings out to Mar 2026 but hold within recent ranges ahead, with little sign of net impact from crude oil futures sliding on Reuters suggesting OPEC is considering further supply hikes.

- Today’s JOLTS report sees the start of the week’s labor data build up to payrolls on Friday, with ADP coming tomorrow owing to a Labor Day delay.

- Cumulative cuts from 4.33% effective: 23bp Sep, 35.5bp Oct, 55.5bp Dec, 66bp Jan and 80bp Mar.

- SOFR futures are up to 1.5 ticks lower on the day out through 2027 contracts.

- The SOFR implied terminal yield of 3.01% (still SFRH7) is 1bp higher, off last week’s multi-month lows of ~2.95% but still pointing to more than 130bp of cuts from current levels.

- St Louis Fed’s Musalem (’25 voter, hawk) speaks on the economy and policy at the Peterson Institute at 0900ET (text tbd, Q&A). We imagine risks are skewed to the dovish side considering his usually hawkish stance. He said Aug 14 that inflation seems to be running close to 3%, he expects the tariff inflation impact to fade in 2-3 quarters but that there was a reasonable possibility it could be more persistent. He saw the labor market at full employment but with risks to the downside.

- Fed Beige Book (1400ET). With a focus on labor developments ahead of Friday’s payrolls report, recall that July’s Beige Book characterized the labor market in fairly mixed fashion, though generally stable to slightly-positive across most Fed Districts compared with the June beige book. It was arguably the most solid Beige Book on the employment front since the start of the year.

LOOK AHEAD: Wednesday Data Calendar: StL Fed Musalem, JOLTS, Factory Orders

Sep-03 10:30

- US Data/Speaker Calendar (prior, estimate)

- 09/03 0700 MBA Mortgage Applications (-.5%, --)

- 09/03 0900 StL Fed Musalem on economy/policy, moderated Q&A

- 09/03 1000 JOLTS Job Openings (7.437M, 7.382M), Rate (4.4%, --)

- 09/03 1000 JOLTS Quits Level (3.412M, 3.136M), Rate (2.0%, --)

- 09/03 1000 JOLTS Layoffs Level (1.604M, 1.675M) Rate (1.0%, --)

- 09/03 1000 Factory Orders (-4.8%, -1.3%), ex-trans (0.4%, 0.6%)

- 09/03 1000 Durable Goods Orders (-2.8%, -2.8%), ex-trans (1.1%, 1.1%)

- 09/03 1000 Cap Goods Orders Nondef Ex Air (1.1%, 1.1%), ship (0.7%, --)

- 09/03 1130 US Tsy $65B 17W bill auction

- 09/03 1400 Fed Beige Book

- Source: Bloomberg Finance L.P. / MNI

EU-BILL AUCTION RESULTS: 3/6/12-Month EU-Bills

Sep-03 10:17

| Type | 3-month EU-bill | 6-month EU-bill | 12-month EU-bill |

| Maturity | Dec 5, 2025 | Mar 6, 2026 | Sep 4, 2026 |

| Amount | E817mln | E894mln | E997mln |

| Target | E1.0bln | E1.0bln | E1.0bln |

| Previous | E907mln | E917mln | E1.303bln |

| Avg yield | 1.946% | 1.968% | 1.982% |

| Previous | 1.946% | 1.945% | 1.937% |

| Bid-to-cover | 1.85x | 1.83x | 1.67x |

| Previous | 2.51x | 2.68x | 2.01x |

| Previous date | Aug 06, 2025 | Aug 06, 2025 | Aug 06, 2025 |