MNI US MARKETS ANALYSIS - Risk Holds Rally Despite WH Appeal

Highlights:

- Risk rallies, tech outperforms on double tailwind of tariff ruling and solid NVIDIA earnings

- White House lodges immediate appeal against court ruling, but Trump's personal response yet to come

- GDP second reading, litany of Fedspeak mark the calendar highlights

US TSYS: Off Lows, Awaiting Trump Response To Court Ruling And 0830ET Data

- Treasuries are pulling back off lows, in more uniform moves now having at first mostly reversed a sizeable bear flattening seen with the Asia open in reaction to the U.S. Court of International Trade ruling that Trump's April 2 tariffs superseded his executive authority.

- US desks filtering in appeared to help push the long end to new latest lows although moves were at a steady pace and have also been pared quickly in recent trading.

- Cash yields are 2.3-4.5p higher, with increases led by 5s and 7s whilst 2s lag the day’s sell-off. Today’s 7Y supply could be helping this underperformance at the margin, although follows yesterday’s strong 5Y which traded through by 0.4bp and saw a record high for indirect take-up.

- 2s10s at 50.6bp (+1.3bp) has lifted off overnight lows of 47.5bp whilst 5s30s at 91.1bp (-0.7bp) has lifted off 87bps.

- TYU5 trades at 109-30+ (-09+) on solid volumes of 490k considering the roll is nearly complete.

- It’s off an earlier low of 109-26 that came close to tentative support at 109-25+ (Friday’s low) but still a little off troubling firmer support at 109-12+ (May 22 low). In case a corrective bounce resumes, resistance is seen at 110-21 (50-day EMA) for close to a key 110-23 (May 16 high).

- Today sees markets awaiting Trump’s response to the court ruling before data attention on GDP revisions and jobless claims including a payrolls reference period for continuing claims.

- Data: 2nd Q1 GDP/PCE revisions (0830ET), Jobless claims (0830ET), Pending home sales Apr (1000ET)

- Fedspeak: Barkin (0830ET), Goolsbee (1040ET), Kugler (1400ET), Daly (1600ET), Logan (1825ET)

- Coupon issuance: US to sell $44bn 7Y notes - 91282CNF4 (1300ET)

- Bill issuance: US to sell $75bn 4W bills, $65bn 8W bills (1130ET)

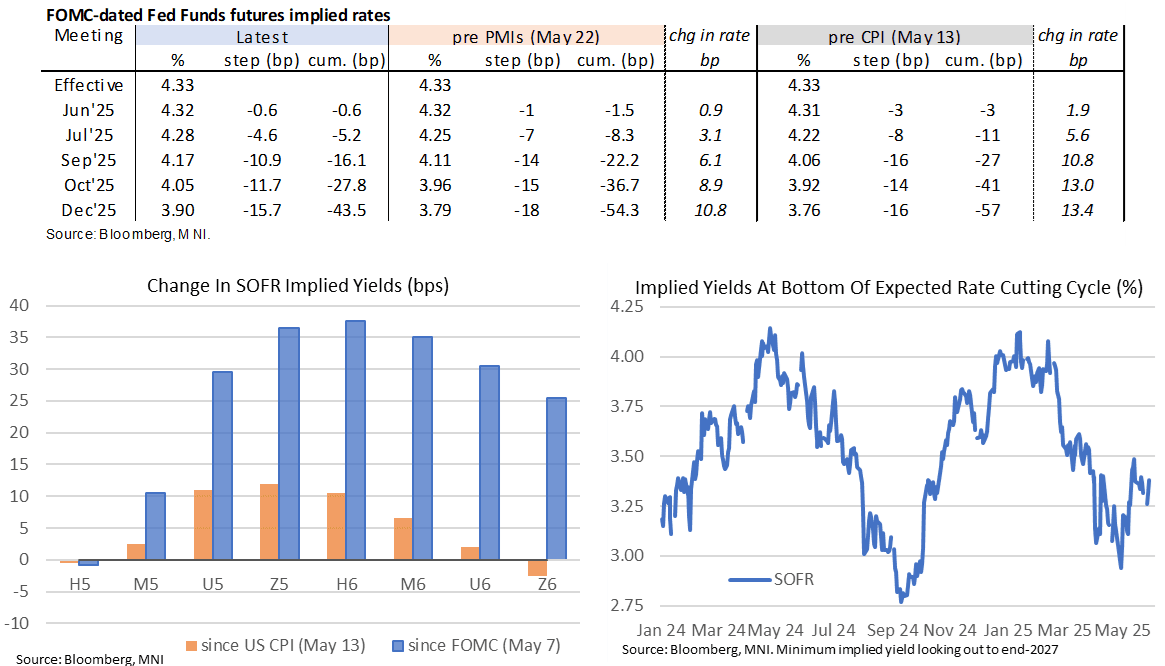

STIR: Holding Most Of Trimming In Fed Cut Expectations On Trade Court Ruling

- Fed Funds implied rates are off overnight hawkish extremes following the U.S. Court of International Trade ruling that Trump's April 2 tariffs superseded his executive authority but still sees the Dec’25 rate 2bp higher on the day.

- Cumulative cuts from 4.33% effective: 0.5bp Jun, 5bp Jul, 16bp Sep, 28bp Oct and 43.5bp Dec.

- The SOFR terminal implied yield of 3.38% (SFRZ6, +6.5bp) is up solidly overnight but roughly keeps to the circa 100bp +/-5bp range of cuts from current effective rates seen over the past two and a half weeks.

- Yesterday’s FOMC minutes suggested there wasn’t any participant who argued any way forcefully for the potentially "transitory" inflation outcome of tariffs. The vast majority were focused on multiple upside risks, with a small nod to factors that might mitigate inflation - including weaker growth. It's not even clear Gov Waller made the case for a one-off shock to inflation from tariffs, which he has repeated multiple times in public appearances. See a more in-depth review of the minutes here.

- Trump reaction and data is likely more important but today also sees Fedspeak from five separate FOMC members.

FED: Context For Today's Five Fed Speakers

The majority of today's Fed speakers have spoken recently, although of course these will be the first comments post the court ruling. We would ordinarily have put most focus on Kugler and Logan but the former only gives opening remarks and the latter is comfortably after the close.

- 0830ET – Barkin (non-voter) in a fireside chat (just Q&A). He said May 27 that people are being patient on investment decisions and waiting out policy uncertainty whilst there is no evidence that the drop in sentiment is affecting spending.

- 1040ET – Goolsbee (’25 voter, dove) in moderated Q&A (text tbd + Q&A). On May 23 he reiterated that the bar to move rates in any direction is higher but that rate cuts were still possible over a 10-16 month horizon.

- 1400ET – Kugler (permanent voter) opening remarks (just text). She said May 12 that it’s critical to keep long-term inflation expectations anchored but also that short-term expectations matter as they affect wage demand. Talking specifically on the tariff pause announced between the US-China on that day, it changes the magnitude that the Fed might use its tools but not the direction.

- 1600ET – Daly (non-voter) fireside chat (just Q&A). She noted in limited remarks on May 21 that policy is in a good place and that she’s highly sensitive to the risk of inflation. She’d previously said May 14 that the uncertainty shock from US government policy is not yet causing a demand shock.

- 1825ET – Logan (’26 voter) opening remarks and discussion (text + Q&A). She has recently focused on focused on market functioning, saying on May 19 that treasury and money markets are strong but not invulnerable. She previously talked on mon pol back on Apr 10.

US OUTLOOK/OPINION: Consensus Doesn’t Share Powell View On Upward GDP Revisions

- Bloomberg consensus sees real GDP growth remaining at -0.3% annualized in Q1 in the second release, with a small downtick in personal consumption (from 1.8% to 1.7%) the only revision expected from median estimates.

- Recall that last month’s advance release saw real GDP growth ‘surprise’ with -0.3% annualized for Q1. Whilst it appeared close to the -0.2% consensus, it was better than the -0.8% median from 26 analysts who had updated forecasts following March advance trade data just a day beforehand plus the Atlanta Fed’s GDPNow of -1.5%.

- Large swings in trade (-4.8pps) and inventories (+2.25pps) in Q1 on tariff front-running has made it harder to get a sense of underlying momentum in the economy. However, one notable finding in the advance release was that final private domestic purchases was robust at 3.0% annualized in Q1 after 2.95% in Q4 and an average 3.0% in 2024 – a point that was unsurprisingly made in the May FOMC press conference.

- It was helped by a surge in non-residential investment (9.8%, adding 1.3pp to GDP growth) plus consumption growth at a softer but still relatively healthy 1.8% vs an expected 1.2%. Both of course were likely boosted by tariff front-running as well.

- Powell talked on the nature of the large trade drag as well as his expectations for upward revisions: “So that could, in the second quarter, be reversed so that we have, you know, an unusually large [negative] contribution to—unusually positive. That’s very likely as imports drop sharply. You could also have—you know, very likely you’ll have restatements of the—of the first quarter. It’ll turn out that consumer spending was higher. It will turn out that inventories were higher. And so you’ll see —you’ll see those data revised up. It may actually go into the third quarter, too. And so I think it’s going—this whole process is going to, a little bit, make it harder to make a clean assessment of U.S. demand.”

STIR: Apparent Net Long Setting In SFRM5 Bucks Wider Wednesday Theme

OI data generally points to a mix of net short setting and long cover as most SOFR futures settled lower on Wednesday.

- An exception to the wider theme seemingly came via SFRM5, which saw the largest net positioning swing on the day (OI in that contract continues to swell, rising by ~248K lots since last Tuesday).

- That contract finished unchanged on the day after seeing two sizeable rounds of screen buying, which suggests that net long setting dominated there.

| 28-May-25 | 27-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,064,876 | 1,069,272 | -4,396 | Whites | +88,818 |

SFRM5 | 1,467,973 | 1,393,653 | +74,320 | Reds | -7,514 |

SFRU5 | 1,109,932 | 1,102,147 | +7,785 | Greens | -24,627 |

SFRZ5 | 1,075,375 | 1,064,266 | +11,109 | Blues | +5,547 |

SFRH6 | 764,540 | 763,368 | +1,172 |

|

|

SFRM6 | 730,600 | 722,043 | +8,557 |

|

|

SFRU6 | 705,185 | 723,256 | -18,071 |

|

|

SFRZ6 | 837,702 | 836,874 | +828 |

|

|

SFRH7 | 671,330 | 689,028 | -17,698 |

|

|

SFRM7 | 592,371 | 592,963 | -592 |

|

|

SFRU7 | 425,954 | 421,415 | +4,539 |

|

|

SFRZ7 | 407,739 | 418,615 | -10,876 |

|

|

SFRH8 | 284,609 | 279,927 | +4,682 |

|

|

SFRM8 | 203,764 | 197,659 | +6,105 |

|

|

SFRU8 | 162,256 | 161,649 | +607 |

|

|

SFRZ8 | 187,746 | 193,593 | -5,847 |

|

|

EUROPE ISSUANCE UPDATE:

UK tender results

- 0.125% Aug-31 I/L supply was smoothly digested.

- GBP1.25bln of the 0.125% Aug-31 Linker. Avg yield 0.827% (bid-to-cover 2.57x).

Italy auction results

- E3.25bln of the 2.95% Jul-30 BTP. Avg yield 2.73% (bid-to-cover 1.52x).

- E3.25bln of the 3.60% Oct-35 BTP. Avg yield 3.57% (bid-to-cover 1.52x).

- E3.5bln of the 0.85% Apr-34 CCTeu. Avg yield 3.28% (bid-to-cover 1.52x).

GERMANY: Coalition Measures Include Doubling Down on Infra & Streamlining Taxes

The German government overnight announced a timeline for measures of an "immediate program" to underpin the struggling economy. Most measures flagged appear to have been touted by media reports and/or the coalition agreement before, meaning there are few surprises. Key excerpts below:

Economic Measures

- Degressive depreciation of tax obligations ("Investitions-Booster")

- 30% in year 1, then 30% of remaining value each following year

- Applies for 2025, 2026, and 2027

- Extra-fast depreciation of tax obligations for enterprise-held electric vehicles

- 75% in year 1, followed by 10%, then 5%, 5%, 3%, and 2%

- Timeframe seemingly not explicitly stated, but likely aligns with the 2025–2027 investment period

- Reduction of corporation tax (Körperschaftsteuer)

- Gradual decrease from 15% to 10% in five annual steps starting 2028

- Parallel tax relief for partnerships (Personengesellschaften)

- Final tax burden to also reach 25%, aligned with corporations

- No specific timeframe, but parallel to corporate tax reform

- Simplification of permit procedures & reduction of bureaucracy

- Planning, building, environmental, procurement, and administrative law reforms

- First decisions expected before summer 2025

- Digitalization of public procurement law

- Target: Summer 2025

- Creation of the 500-billion-euro special fund for infrastructure and climate neutrality

- To be passed by summer 2025

- Runs over the next 12 years (through 2037)

- Climate & energy infrastructure acceleration

- Faster permits for wind power, hydrogen, geothermal, etc.

- Reforms to start by summer 2025

Social and Labour Market Measures

- Tariff loyalty law (Bundestariftreuegesetz)

- To enforce collective wage agreements in public contracts

- No timeframe specified

- Extension of rent control (Mietpreisbremse)

- Already initiated, duration or end date not mentioned

- Comprehensive pension reform ("Rentenpaket")

- Includes 48% pension level guarantee (Haltelinie) until 2031

- Expansion of "Mütterrente" (+€20/month per child for mothers)

- New “Active Pension” (Aktivrente): tax-free income up to €2000/month for seniors

- No implementation date stated, but included in first-term priorities

Tax and Subsidy Reliefs

- Reduced VAT for gastronomy (from 19% to 7%)

- Planned from January 1, 2026

- Increased commuter allowance (Pendlerpauschale)

- Planned from January 1, 2026

- Revival of diesel tax rebate for agriculture (Agrardiesel)

- Planned from January 1, 2026

- Lowering electricity tax, grid fees, and gas storage levy

- No specific date, but part of overall economic relief package

Institutional and Governance

- Commission on debt brake reform

- To be convened soon, as agreed in coalition deal

TAIWAN: CB Sees Financial System Stable Despite Broad FX Losses in April

Taiwan's 2025 financial stability report certainly eyed more carefully after recent currency volatility. The report states the insurance sector suffered a TWD 118bln FX loss in April (USD/TWD dropped 3.6% over the month), but losses would have been well over double that on a pre-hedging basis (TWD 322bln), and as such the financial system remains generally stable. Full report for download is here (only available in Mandarin so far): https://www.cbc.gov.tw/tw/cp-899-182554-5fef0-1.html

- Worth noting that the USD/TWD fell further, and more sharply, in early days of May: as much as 7.7% over the course of two sessions - meaning FX losses for insurers were likely of a much higher magnitude as both the spot move and the sharp increase in hedging costs will have eaten into positioning.

- The report acknowledges the life insurance sector, with large domestic & foreign investment positions, faces higher market risks ahead. Implied vols are likely one of these risks - feeding directly into hedging costs and forcing firms to seek more cost effective hedges via the likes of HKD, IDR and KRW - a key driver of the APAC FX vol earlier this month.

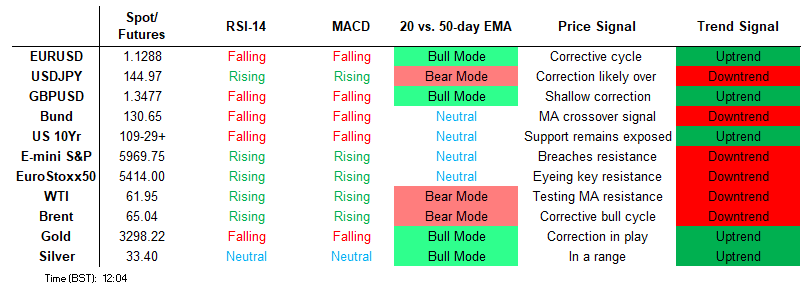

EGBS: Curves Bear Flatten On US Court Ruling, But Policy Uncertainty Still High

The German curve has lightly bear flattened, with yields 1-2bps higher on the session. The Court of International Trade’s judgement blocking a significant portion of US tariffs has pushed European yields higher, as it reduces the tariff-implied downside growth/inflation risks facing the Eurozone economy.

- Hawkish impetus is limited by the fact the judgement does not cover sectoral tariffs (e.g. on autos and steel/aluminium). The court ruling should also not be considered set in stone. The US administration has already appealed the judgement, and there are avenues available for tariffs to be ratcheted higher in the meantime - uncertainty remains high.

- Bund futures gapped 23 ticks lower at open, and currently trade -18 ticks versus yesterday’s settlement at 130.65. The contract has moved away from session lows of 130.39. A bullish theme in Bund futures remains intact and the pullback from Tuesday’s lows is considered corrective.

- Liquidity has been thinned out by the Ascension Day public holiday in Germany and France.

- 10-year EGB spreads to Bunds are biased tighter, with the Court judgement supporting risk sentiment (even with European equity futures off overnight highs).

- Italy sold 5/10-year BTPs and a new CCTeu this morning, with the supply digested smoothly. Italian business and consumer confidence improved in May, but it is still too early to determine whether sentiment has entered a more pronounced uptrend.

- Global focus turns to this afternoon’s US GDP, PCE and jobless claims data.

FOREX: USD Slips Off Tariff Ruling Overnight High, AUD Benefits

- European desks have been happy to fade the overnight bid in the USD so far this morning, with markets reassessing the implications of the Court of International Trade’s tariff block. Although the ban implies a smaller tariff-related hit to US growth and upside inflation risk than a day ago, it further increases US policy – and political – uncertainty.

- EURUSD had traded lower by as much as 0.7% overnight, but has pared losses to trade in only minor negative territory headed into the Ny crossover. The pair briefly pierced initial support at the 20-day EMA, bringing attention to the more important support at 1.1156, the 50-day EMA. Meanwhile, GBPUSD has also essentially fully unwound the overnight selloff.

- AUD outperforms against broader G10 FX, the primary beneficiary from the slip off overnight highs for the greenback. AUD/USD pressed toward 0.6450 this morning to challenge yesterday's highs, and while the moves may be inconsequential on the week, (AUD/USD is still hugging the 200-dma at 0.6444) the currency is looking more constructive against the likes of JPY, CHF and EUR on the daily charts - against which the underlying positivity and re-correlation with global equities is aiding prices higher.

- Having bounced off pullback lows of 1.7248, EUR/AUD looks to have concluded the corrective bounce, with spot now through 38.2% retracement of the strength. A further stabilisation of global trade themes or persistence of legal challenges against Trump's tariffs would affirm the AUD profile, particularly if the E-mini S&P holds a sustainable break above the 6,000 handle.

- Weekly US jobless claims and the secondary reading for the core PCE price indices are the calendar highlights Thursday. Fed's Barkin, Goolsbee, Kugler & Daly are all set to speak as well as BoE's Bailey. The Ascension day public holiday will thin out liquidity in the European session, even with most domestic markets still open.

OPTIONS: Expiries for May29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1200(E784mln), $1.1300-15(E540mln)

- USD/JPY: Y144.80-00($2.1bln)

- USD/CAD: C$1.4355-75($1.5bln)

EQUITIES: E-Mini S&P Rallies Above Bull Trigger and $6000 Handle

- The trend cycle in Eurostoxx 50 futures remains bullish and the recent pullback appears corrective. Moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. A break of this level would strengthen a bull theme. Key support to watch lies at 5244.11, the 50-day EMA. Clearance of this average would signal a possible reversal.

- A bullish trend condition in S&P E-Minis remains intact. Today’s gains have delivered a print above 5993.50, the May 20 high and a bull trigger. The break confirms a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. 6000.00 has been pierced, an extension would open 6057.00 next, the Mar 3 high. Key support lies at 5734.85, the 50-day EMA. A clear break of this average is required to highlight a reversal.

COMMODITIES: WTI Futures Trading Above Key Resistance at the 50-Day EMA

- WTI futures traded to a fresh S/T cycle high on May 21 before finding resistance. The recovery since Apr 9, appears corrective. Key resistance to watch is $62.60, the 50-day EMA. It has been pierced, a clear break of it would highlight a stronger reversal and open $65.82, Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger. The price pattern on May 21 is a shooting star - a bearish signal.

- Recent gains in Gold signal the end of the corrective phase between Apr 22 - May 15. Medium-term trend signals are unchanged, they remain bullish and the latest pullback is considered corrective. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. A resumption of gains would open $3435.6 next, the May 7 high. Key support and the bear trigger has been defined at $3121.0, the May 15 low.

| Date | GMT/Local | Impact | Country | Event |

| 29/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 29/05/2025 | 1230/0830 | * | Current account | |

| 29/05/2025 | 1230/0830 | * | Payroll employment | |

| 29/05/2025 | 1230/0830 | *** | GDP | |

| 29/05/2025 | 1230/0830 | Richmond Fed's Tom Barkin | ||

| 29/05/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 29/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 29/05/2025 | 1445/1545 | BOE's Saporta panellist on hedge funds' role in recent crises | ||

| 29/05/2025 | 1500/1100 | ** | DOE Weekly Crude Oil Stocks | |

| 29/05/2025 | 1500/1600 | BOE's Bailey speech and fireside chat at Irish IAIM Dinner | ||

| 29/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 29/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 29/05/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 29/05/2025 | 1800/1400 | Fed Governor Adriana Kugler | ||

| 29/05/2025 | 2000/1600 | San Francisco Fed's Mary Daly | ||

| 30/05/2025 | 2330/0830 | ** | Tokyo CPI | |

| 30/05/2025 | 2330/0830 | * | Labor Force Survey | |

| 30/05/2025 | 2350/0850 | ** | Industrial Production | |

| 30/05/2025 | 2350/0850 | * | Retail Sales (p) | |

| 29/05/2025 | 0025/2025 | Dallas Fed's Lorie Logan | ||

| 30/05/2025 | 0130/1130 | * | Building Approvals | |

| 30/05/2025 | 0130/1130 | ** | Retail Trade | |

| 30/05/2025 | 0600/0800 | *** | GDP | |

| 30/05/2025 | 0600/0800 | ** | Import/Export Prices | |

| 30/05/2025 | 0600/0800 | ** | Retail Sales | |

| 30/05/2025 | 0630/0730 | DMO to release FQ2 (Jul-Sep) issuance ops calendar | ||

| 30/05/2025 | 0700/0900 | *** | HICP (p) | |

| 30/05/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/05/2025 | 0800/1000 | ** | M3 | |

| 30/05/2025 | 0800/1000 | *** | GDP (f) | |

| 30/05/2025 | 0800/1000 | *** | Bavaria CPI | |

| 30/05/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 30/05/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 30/05/2025 | 0900/1100 | *** | HICP (p) | |

| 30/05/2025 | 1000/1200 | ** | PPI | |

| 30/05/2025 | 1200/1400 | *** | HICP (p) | |

| 30/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 30/05/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 30/05/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 30/05/2025 | 1230/0830 | *** | GDP - Canadian Economic Accounts | |

| 30/05/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 30/05/2025 | 1230/0830 | *** | CA GDP by Industry and GDP Canadian Economic Accounts Combined | |

| 30/05/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 30/05/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 30/05/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 30/05/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 30/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 30/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 30/05/2025 | 2045/1645 | San Francisco Fed's Mary Daly |