STIR: Holding Most Of Trimming In Fed Cut Expectations On Trade Court Ruling

May-29 10:38

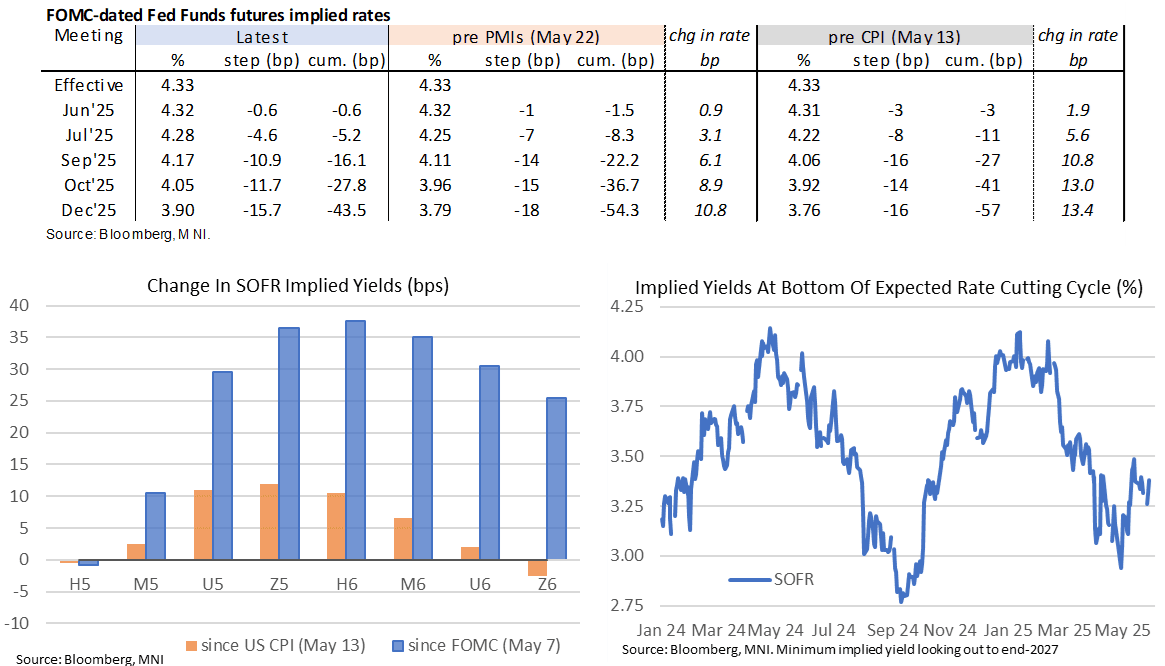

- Fed Funds implied rates are off overnight hawkish extremes following the U.S. Court of International Trade ruling that Trump's April 2 tariffs superseded his executive authority but still sees the Dec’25 rate 2bp higher on the day.

- Cumulative cuts from 4.33% effective: 0.5bp Jun, 5bp Jul, 16bp Sep, 28bp Oct and 43.5bp Dec.

- The SOFR terminal implied yield of 3.38% (SFRZ6, +6.5bp) is up solidly overnight but roughly keeps to the circa 100bp +/-5bp range of cuts from current effective rates seen over the past two and a half weeks.

- Yesterday’s FOMC minutes suggested there wasn’t any participant who argued any way forcefully for the potentially "transitory" inflation outcome of tariffs. The vast majority were focused on multiple upside risks, with a small nod to factors that might mitigate inflation - including weaker growth. It's not even clear Gov Waller made the case for a one-off shock to inflation from tariffs, which he has repeated multiple times in public appearances. See a more in-depth review of the minutes here.

- Trump reaction and data is likely more important but today also sees Fedspeak from five separate FOMC members.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROZONE DATA: Few Bright Spots In The EC's April Survey

Apr-29 10:30

The EC’s sentiment index slipped to 93.6 in April, below the 94.5 consensus and 95.0 prior for the lowest since October 2023. The results underscore ECB Governing Council concerns around the growth outlook, with few positive signals across the business and consumer sides of the survey.

- Both industry (-11.2 vs 10.4 cons, -10.7 prior) and services (1.4 vs 2.2 cons, 2.2 prior) were weaker than expected.

- Within the industry survey, the expected production component was 0.0, its weakest level YTD. There were no obvious signs of tariff front-running in the export orders component.

- The retail confidence reading also softened to -8.9 (vs -7.0 prior). The future business activity component fell for a fourth consecutive month.

- The expected employment indicator was steady at 96.5, the weakest since February 2021. Meanwhile, expected price metrics ticked up modestly across industries.

- Consumer confidence was confirmed at -16.7 (vs -14.5 prior). All of the forward-looking components (financial situation, economic situation, unemployment expectations, capacity to save and major purchase intentions) weakened in April.

LOOK AHEAD: Tuesday Data Calendar: Inventories, House Prices, JOLTS Job Openings

Apr-29 10:27

- US Data/Speaker Calendar (prior, estimate)

- 29-Apr 0830 Advance Goods Trade Balance (-$147.8B rev, -$145.0B)

- 29-Apr 0830 Wholesale Inventories MoM (0.3%, 0.6%), Retail MoM (0.1%, 0.3%)

- 29-Apr 0900 FHFA House Price Index MoM (0.2%, 0.3%)

- 29-Apr 0900 S&P CoreLogic CS 20-City MoM SA (0.46%, 0.40%)

- 29-Apr 1000 JOLTS Job Openings (7.568M, 7.5M), Rate (4.5%, 4.5%)

- 29-Apr 1000 Conf. Board Consumer Confidence (92.9, 88.0)

- 29-Apr 1030 Dallas Fed Services Activity (-11.3, --)

- 29-Apr 1130 US Tsy $70B 6W bill auction

EGB SYNDICATION: 3.00% Jun-49 Green OAT: Final terms

Apr-29 10:26

- Spread set earlier at 3.00% Jul-49 OAT + 13bps (guidance was +15bp area)

- Size: E5bln (MNI expects E4-8bln)

- Books in excess of E74bln (inc JLM interest)

- Settlement: May 7, 2025 (T+5)

- Bookrunners: Barclays, BNPP (B&D), BofA, CA-CIB, HSBC, Natixis

- Timing: MNI expects to price today

Source: Bloomberg and MNI colour